Key Points :

- Bipartisan agreement in the U.S. may restrict yield on stablecoin passive balances

- The CLARITY Act could define market structure and unlock institutional participation

- Banks fear deposit outflows, while policymakers argue capital inflows may increase

- Yield-bearing stablecoins remain the central conflict between innovation and financial stability

- The outcome will reshape DeFi, CeFi, and global crypto capital flows

1. A Turning Point: The CLARITY Act Moves Forward

Recent developments in Washington suggest that the long-anticipated CLARITY Act—designed to establish a comprehensive regulatory framework for digital assets—is approaching a breakthrough. According to reports, bipartisan leaders have reached a “principled agreement” on one of the most contentious issues: whether stablecoins should offer yield to holders.

At the center of this agreement is a proposed restriction on providing yield to what policymakers call “passive balances.” In practical terms, this means that simply holding a stablecoin—such as USDC or USDT—would not generate interest-like returns in the same way that decentralized finance (DeFi) protocols currently allow.

This compromise reflects a broader balancing act between fostering innovation and preserving financial stability. Lawmakers appear increasingly aware that without regulatory clarity, the United States risks losing its leadership position in the global crypto economy. At the same time, they must address concerns from traditional financial institutions, particularly banks, which see yield-bearing stablecoins as a direct competitive threat.

The significance of this moment cannot be overstated. For years, regulatory uncertainty has stalled institutional participation and limited the scalability of blockchain-based financial systems. If the CLARITY Act progresses, it could provide the legal foundation necessary for large-scale adoption of digital assets in both retail and institutional contexts.

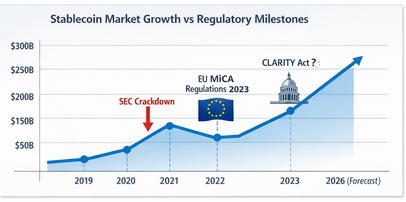

“Stablecoin Market Growth vs Regulatory Milestones”

Description: A line chart showing stablecoin market cap growth (2019–2026) alongside major regulatory events (SEC actions, EU MiCA, potential CLARITY Act).

2. The Core Conflict: Yield vs Financial Stability

The central issue in the current negotiations is whether stablecoins should be allowed to offer yield. In traditional finance, yield is typically generated through lending, staking, or investment activities. In the crypto world, however, yield can be embedded directly into token ecosystems through smart contracts.

For example, users can deposit stablecoins into DeFi protocols and earn returns ranging from 3% to over 10%, depending on market conditions. This stands in stark contrast to traditional bank deposits, which often yield less than 1% annually in many jurisdictions.

From the perspective of regulators and banks, this discrepancy raises serious concerns. If consumers can earn significantly higher returns by holding stablecoins instead of depositing funds in banks, a large-scale migration of capital could occur. This phenomenon—known as “deposit flight”—could weaken the traditional banking system, particularly during periods of financial stress.

However, proponents of yield-bearing stablecoins argue that these concerns are overstated. They contend that stablecoins, when properly regulated and backed by high-quality reserves, can actually enhance financial stability by increasing efficiency and transparency. Moreover, they argue that innovation in financial products should not be stifled simply to protect incumbent institutions.

The proposed restriction on passive yield represents a middle ground. It allows stablecoins to exist and function as digital dollars, while limiting their ability to compete directly with bank deposits in terms of interest generation.

3. Banking Sector Concerns: A Real Threat or Strategic Fear?

The banking industry has been one of the most vocal opponents of yield-bearing stablecoins. Their argument is straightforward: if stablecoins offer higher returns than traditional savings accounts, customers will move their funds out of banks and into digital wallets.

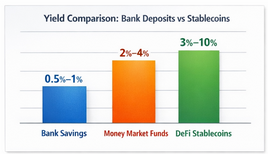

To understand the magnitude of this concern, consider the following simplified comparison:

“Yield Comparison: Bank Deposits vs Stablecoins”

Description: Bar chart comparing:

- Bank savings: ~0.5%–1.0%

- Money market funds: ~2%–4%

- DeFi stablecoin yield: ~3%–10%

This gap in yield is not merely theoretical—it has already driven significant capital flows into decentralized finance during previous market cycles. At its peak, the total value locked (TVL) in DeFi exceeded $150 billion, much of it denominated in stablecoins.

Banks fear that if such yields become widely accessible and legally sanctioned, their core business model—based on deposit-taking and lending—could be disrupted. In extreme scenarios, this could lead to liquidity shortages and systemic risk.

Yet, some policymakers argue that these fears may be exaggerated. They suggest that regulated stablecoins could actually channel new capital into the banking system, particularly if issuers are required to hold reserves in bank deposits or government securities.

This perspective reframes stablecoins not as competitors, but as extensions of the existing financial infrastructure.

4. Political Dynamics: Bipartisan Alignment and Strategic Compromise

One of the most notable aspects of the recent development is the bipartisan nature of the agreement. In an era of deep political polarization, cooperation between Republican and Democratic lawmakers on crypto regulation is significant.

The agreement reflects a shared recognition that digital assets are no longer a niche sector, but a core component of the future financial system. Both parties appear motivated to provide regulatory clarity, albeit for different reasons:

- Republicans tend to emphasize innovation, market freedom, and global competitiveness

- Democrats focus more on consumer protection, financial stability, and systemic risk

The compromise on stablecoin yield restrictions represents a convergence of these priorities. By limiting yield on passive balances, lawmakers aim to reduce systemic risk while still allowing innovation to flourish in more controlled environments.

This approach also aligns with global regulatory trends. For example, the European Union’s Markets in Crypto-Assets (MiCA) framework imposes strict requirements on stablecoin issuers, including reserve transparency and operational safeguards.

5. Implications for Crypto Markets and Investment Opportunities

For investors and builders in the crypto space, the implications of the CLARITY Act are profound.

5.1 Institutional Entry

Clear regulations are likely to accelerate institutional adoption. Large financial institutions, hedge funds, and asset managers have been hesitant to enter the market due to legal uncertainty. A well-defined framework could unlock billions of dollars in capital inflows.

5.2 Evolution of Yield Mechanisms

If passive yield is restricted, the market will likely shift toward more active and structured yield strategies. These may include:

- Tokenized treasury products

- On-chain lending platforms with explicit risk disclosures

- Hybrid CeFi-DeFi models

5.3 New Revenue Models

For entrepreneurs, the regulatory clarity could open new business models, such as:

- Regulated stablecoin issuance

- Compliance-focused DeFi platforms

- Cross-border payment systems leveraging stablecoins

5.4 Global Competitive Landscape

The United States’ approach will influence global standards. If the CLARITY Act strikes the right balance, it could position the U.S. as a leader in digital asset innovation. Conversely, overly restrictive rules could push innovation offshore to jurisdictions with more favorable regulations.

“Global Stablecoin Regulation Comparison”

Description: Table/diagram comparing:

- USA (CLARITY Act – proposed)

- EU (MiCA – active)

- Singapore (MAS framework)

- Hong Kong (Stablecoin licensing)

6. Strategic Outlook: Bridging Traditional Finance and Blockchain

The debate over stablecoin yield is ultimately a reflection of a larger transformation: the convergence of traditional finance and blockchain-based systems.

Stablecoins are not merely digital tokens—they are programmable money. They enable real-time settlement, cross-border payments, and integration with decentralized applications. As such, they represent a fundamental shift in how financial value is stored and transferred.

The challenge for regulators is to integrate these innovations into existing frameworks without undermining the stability of the financial system. The CLARITY Act, if implemented effectively, could serve as a blueprint for this integration.

Conclusion: A Defining Moment for Crypto Regulation

The reported bipartisan agreement on stablecoin yield restrictions marks a critical step forward for the CLARITY Act and the broader crypto regulatory landscape.

By addressing the most contentious issue—yield on passive balances—lawmakers have moved closer to establishing a comprehensive framework that balances innovation with stability. While many details remain to be finalized, the direction is clear: the era of regulatory ambiguity is coming to an end.

For investors, developers, and institutions, this represents both an opportunity and a challenge. The rules of the game are being defined, and those who adapt quickly will be best positioned to capitalize on the next phase of growth in the digital asset ecosystem.

In the long term, the success of the CLARITY Act will depend on its ability to foster innovation while maintaining trust in the financial system. If it succeeds, it could usher in a new era where blockchain and traditional finance coexist seamlessly—unlocking unprecedented economic potential on a global scale.