Main Points :

- Citibank plans to launch cryptocurrency custody services in 2026.

- Bitcoin will be treated as a “bankable” asset within traditional financial infrastructure.

- Institutional investors will access digital assets without managing private wallets.

- Regulatory clarity and stablecoin legislation accelerate adoption.

- Tokenized deposits, collateral management, and 24/7 settlement are next.

- Wall Street integration signals structural transformation of capital markets.

Part I — Bitcoin Becomes a Bank Asset

In February 2026, Citibank announced that it intends to begin offering custody services for Bitcoin (BTC) and other digital assets during 2026. This move represents more than just another bank entering crypto—it signals the transition of digital assets into what Citi describes as “commercialization mode.”

The core strategic objective is to make Bitcoin “bankable.” In other words, digital assets will be treated inside existing banking systems the same way stocks, bonds, and other financial instruments are treated today.

This changes everything.

Institutional investors—asset managers, hedge funds, pension funds, sovereign funds—will be able to gain exposure to Bitcoin and other digital assets without:

- Managing private keys

- Operating blockchain infrastructure

- Custodying assets independently

- Altering their current treasury workflows

Instead, they will interact with digital assets through familiar banking channels.

Bitcoin is no longer an alternative asset sitting outside the system. It is being absorbed into it.

Part II — The Infrastructure Bridge: TradFi Meets Crypto

Citibank’s strategy focuses heavily on infrastructure integration.

Rather than creating a standalone crypto platform, Citi is building a “bridge” between institutional-grade wallet technology and its existing custody operations. This means:

- Institutional private key management integrated into traditional custody frameworks.

- Unified reporting for both traditional and digital assets.

- Seamless balance sheet recognition of digital holdings.

- Risk management integrated across asset classes.

The importance of this cannot be overstated.

Most institutions hesitate to engage with crypto not because they doubt its potential, but because operational complexity is high. Compliance, accounting standards, capital treatment, and internal controls create friction.

Citi is abstracting that complexity.

Once a digital asset appears inside the same system as equities and bonds—with consolidated reporting, audited controls, and regulated oversight—the psychological barrier collapses.

Crypto moves from “speculative alternative” to “allocatable portfolio component.”

Part III — Regulatory Tailwinds and the GENIUS Act

This transition does not happen in isolation.

Recent regulatory developments have significantly reduced uncertainty:

- Pro-innovation regulatory shifts under the current U.S. administration.

- The 2025 GENIUS Act, establishing legal frameworks for stablecoins.

- Increased transparency requirements for digital asset issuers.

- Formalization of custody and settlement guidelines.

Stablecoin clarity is especially important.

Banks historically avoided issuing or integrating stablecoins due to regulatory ambiguity. Now, with defined legal structures, major financial institutions can:

- Issue tokenized deposits.

- Use blockchain-based settlement systems.

- Provide regulated stablecoin services.

Legal clarity transforms experimentation into deployment.

For investors seeking the next yield opportunity, this means stablecoins are no longer fringe instruments—they are becoming regulated banking tools.

Part IV — Institutional Capital Is Already Moving

The integration Citi describes is not theoretical.

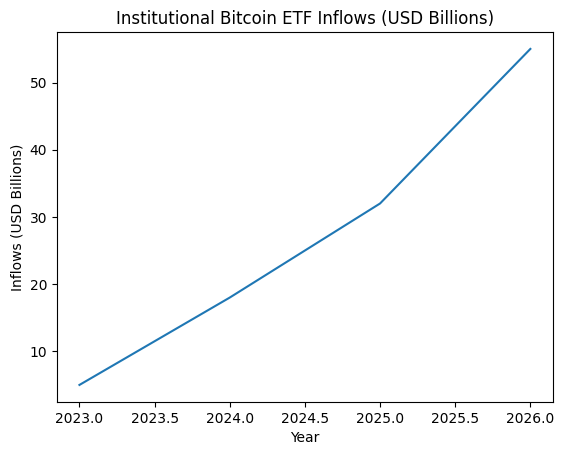

Spot Bitcoin ETFs have already demonstrated strong institutional appetite. In recent cycles, Bitcoin ETFs saw inflows exceeding $750 million during market dips, signaling that institutions are buying corrections rather than avoiding volatility.

Below is an illustrative macro trend of institutional ETF inflows:

[Institutional Bitcoin ETF Inflows]

The upward trajectory shows a structural shift rather than speculative hype.

When custody becomes bank-native, allocation friction declines further. That implies:

- Increased portfolio allocation percentages.

- Broader participation by conservative institutions.

- Expansion beyond BTC into tokenized assets.

Part V — Tokenization and Collateral Management

Citi’s roadmap extends beyond simple custody.

The bank is exploring:

- Using digital assets for collateral management.

- Tokenized deposits enabling 24/7 settlement.

- Blockchain-based settlement efficiency improvements.

- Integration into repo and treasury markets.

This aligns with broader industry trends such as tokenized government bonds and blockchain-based repo transactions.

Tokenization is not about replacing banking—it is about upgrading settlement layers.

Consider the implications:

- Collateral can move instantly.

- Margin requirements can adjust dynamically.

- Settlement risk can be reduced.

- Capital efficiency improves.

For yield-seeking investors, tokenized collateral markets may become one of the next major growth areas.

Part VI — Adoption Curve of Banking Integration

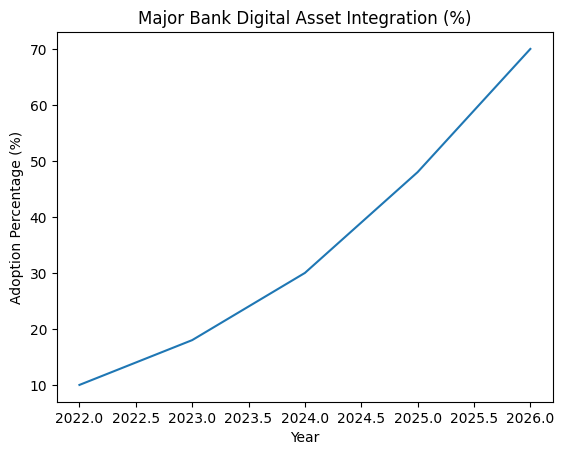

Major banks worldwide are following similar strategies—hybrid development models combining in-house infrastructure with external blockchain partners.

Below is an illustrative adoption curve of major banks integrating digital asset services:

[Major Bank Digital Asset Integration]

The acceleration from experimentation (2022–2023) to commercialization (2025–2026) is clear.

2026 appears to be the inflection point.

Part VII — Strategic Implications for Crypto Investors

For readers searching for new crypto assets and revenue opportunities, the Citi development has profound implications:

1. Infrastructure Tokens May Benefit

Projects providing:

- Institutional custody infrastructure

- Compliance middleware

- Tokenization rails

- Settlement layer scaling

are positioned structurally rather than cyclically.

2. Stablecoin Ecosystem Expansion

Regulated stablecoins may compete with bank deposits. Yield-bearing stablecoins, tokenized treasury products, and programmable liquidity could become dominant tools.

3. Bitcoin as Reserve Collateral

Bitcoin’s integration into collateral frameworks could elevate its role from “digital gold” to “digital base collateral.”

This would fundamentally change its risk profile.

4. Real-World Asset (RWA) Growth

Tokenized bonds, real estate, and structured products will likely expand rapidly once custody integration is standardized.

Part VIII — The Psychological Shift: From Alternative to Core Asset

The most important transformation is not technical—it is psychological.

When banks abstract complexity and embed digital assets into their core systems:

- Risk committees approve allocations.

- Compliance officers gain visibility.

- CFOs gain operational comfort.

- Pension funds move from pilot to deployment.

Crypto transitions from experimental allocation to strategic asset class.

This is the beginning of structural normalization.

Conclusion — 2026 as the Commercialization Threshold

Citibank’s entry into full digital asset custody represents a milestone in financial history.

The strategy is not about chasing crypto hype—it is about system integration.

By making Bitcoin “bankable,” Citi signals:

- Institutional-grade custody is maturing.

- Regulatory clarity is sufficient for deployment.

- Tokenization is entering capital markets.

- Crypto is integrating, not disrupting.

For investors seeking the next opportunity, the question is no longer whether banks will adopt digital assets.

The question is:

Which layers of the digital asset stack will benefit most from institutional absorption?

Bitcoin may anchor the transition.

Stablecoins may lubricate it.

Tokenization may scale it.

But the broader theme is clear.

Crypto is not outside the financial system anymore.

It is becoming part of it.