Main Points :

- Circle partners with Mastercard to enable merchants and acquirers in the EEMEA region to settle in USDC and Euro Coin (EURC) via traditional card rails.

- Circle collaborates with Finastra to integrate USDC into its Global PAYplus (GPP) payments hub, covering over US $5 trillion in daily cross-border flows, enabling banks in 50+ countries to settle with USDC while retaining fiat payment instructions.

- These moves follow U.S. regulatory clarity such as the GENIUS Act and Circle’s expansion via OKX zero-fee conversions, dialogues with Korean banks, and ventures in Japan for USDC and tokenized real-world assets (RWA).

- This marks an institutional-level shift, embedding stablecoins into legacy systems, reducing reliance on correspondent banking, lowering costs, and accelerating settlement—positioning blockchain as a practical backend for payments.

1. Mastercard Integration in EEMEA – A Retail and Merchant On-Ramp

Circle’s newly announced partnership with Mastercard opens a major gateway for stablecoins in retail contexts across the EEMEA (Eastern Europe, Middle East, and Africa) region. Now, acquirers and merchants served by Mastercard there can settle transactions in USDC and Euro Coin (EURC). The first adopters include Arab Financial Services and Eazy Financial Services—marking the first deployment of stablecoin settlement through Mastercard’s network in these regions.

This integration effectively bridges blockchain-native currency with traditional merchant processing, reducing settlement friction and offering merchants faster, more efficient payment clearing. Mastercard’s move into stablecoin settlement underscores mainstream financial players’ recognition of tokenized money’s potential to complement existing payment rails.

2. Finastra’s Global PAYplus – Embedding USDC in Bank Settlement Infrastructure

Simultaneously, Circle announced a strategic collaboration with Finastra, a global financial software leader, to enable USDC settlement through its flagship payments hub, Global PAYplus (GPP). GPP processes over US $5 trillion in daily cross-border payments, serving thousands of banks across more than 130 countries.

Through this integration, banks using GPP can settle cross-border transfers with USDC even when payment instructions remain in fiat. This provides institutions an optional approach to reduce exposure to legacy correspondent systems, accelerate settlement times, maintain compliance and FX operations, and lower transaction costs.

Finastra’s CEO Chris Walters emphasized that this collaboration allows banks to access innovative settlement without building standalone infrastructure. Similarly, Circle’s CEO Jeremy Allaire noted that Finastra’s vast reach makes it a natural channel to scale USDC adoption in global banking flows.

3. Regulatory Momentum and Broader Expansion Strategy

These partnerships build on Circle’s broader global expansion, supported by emerging regulatory clarity and strategic alliances:

- The GENIUS Act, passed in the U.S. recently, established the first federal framework for stablecoins—facilitating institutional confidence in USDC deployments.

- In July, Circle teamed up with major crypto exchange OKX to allow zero-fee conversions from USDC to USD across Asia, Europe, and the Middle East, improving global liquidity access.

- Circle engaged with CEOs of South Korea’s top four banks—KB Kookmin, Shinhan, Hana, Woori—to explore on‑chain integrations and the issuance of Won-pegged stablecoins.

- In Japan, Circle participates in a joint venture with SBI Group and Ripple to promote USDC adoption and build a platform for tokenized real-world assets (RWA) transactions.

4. Practical Impacts for Blockchain Adoption in Payments

Together, these developments represent a significant step toward embedding blockchain assets into practical, large-scale payments infrastructure rather than niche crypto applications. Key implications include:

- Reduced reliance on correspondent banking: Stablecoin settlement bypasses slow, costly multi-hop systems, enabling near-instant settlement 24/7.

- Lower transaction costs: Traditional SWIFT-based transfers can cost tens of dollars and take days. Stablecoins can cut this to below a dollar, with instant settlement.

- Institutional acceptance: Embedding USDC in Mastercard and Finastra infrastructure reflects growing trust by traditional financial institutions in stablecoin technology.

- Regional liquidity and accessibility: Partnerships in EEMEA, Asia, and Japan ensure broader global access, local fiat-linked deployments, and infrastructure integration.

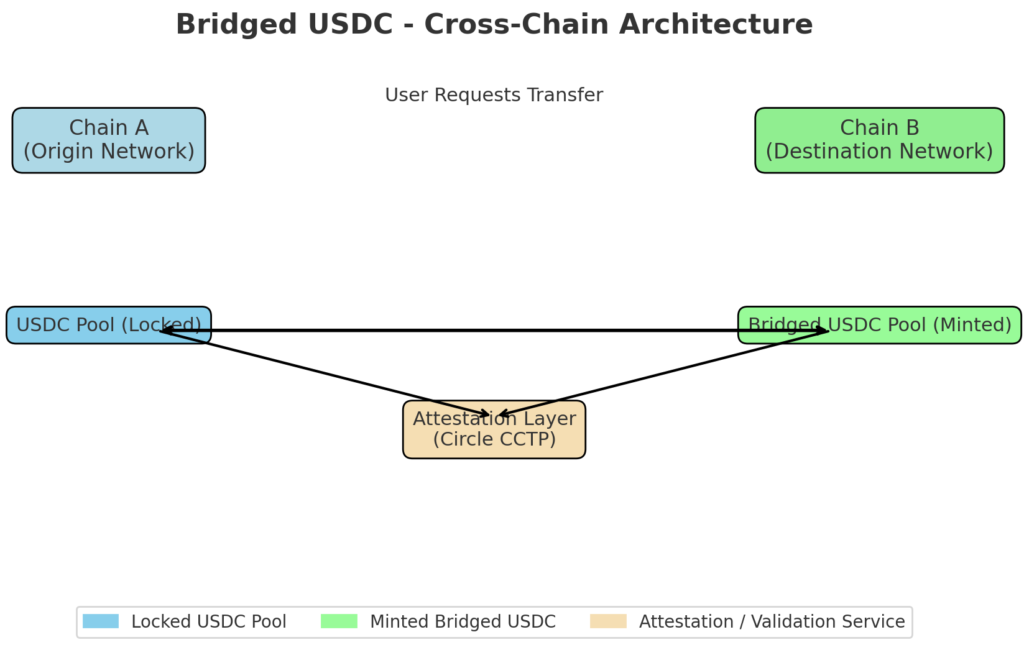

5. Bridged USDC: Technical Approach to Expansion

To support deployments across diverse blockchain ecosystems, Circle has earlier introduced the “Bridged USDC” standard and Cross‑Chain Transfer Protocol (CCTP), offering a scalable foundation for launching USDC on new networks and facilitating liquidity across chains.

(above, illustrating how Bridged USDC works across chains—on-chain/off-chain components, token pools, attestations. Supports an understanding of the technical scalability behind these partnerships.)

6. Summary and Outlook

Circle’s strategic moves with Mastercard and Finastra transform stablecoins from speculative assets into practical financial utilities embedded in mainstream banking and payments systems. By enabling merchant acceptance in emerging markets and bank-level settlement across global cross-border flows, USDC becomes a powerful bridge between the blockchain world and legacy finance.

In regions like EEMEA, emerging markets may benefit from quicker, low-cost payments. For banks, stablecoin settlement removes friction without disrupting existing compliance structures. Circle’s regulation-aligned expansion—backed by U.S. legislation, Asian bank dialogues, and Japanese tokenization initiatives—reflects a comprehensive strategy for global digital cash adoption.

Going forward, we anticipate:

- Broader rollout of USDC settlement across more merchant networks and banking systems.

- Regulatory follow-through, particularly in Europe and Asia, to support such integrations.

- Increasing issuance of local fiat-pegged stablecoins tied to USDC rails.

- Growth of tokenized real-world asset platforms using USDC as settlement medium.