Main Points :

- Circle’s Q4 2025 adjusted EBITDA surged 412% year-over-year.

- USDC circulation increased 72% to $75.3B.

- On-chain transaction volume reached $11.9T, up 247%.

- Reserve revenue hit $733M despite declining yields.

- Tether (USDT) market cap declined for two consecutive months to $1.836T.

- Circle is expanding infrastructure through Arc blockchain and Circle Payments Network.

- Multi-year USDC CAGR target: 40%.

- Transition underway from interest-based revenue to fee/subscription models.

1. Q4 2025: A Defining Quarter for Circle

Circle Internet Group (NYSE: CRCL) delivered one of the most decisive earnings reports in the modern history of stablecoins. For Q4 2025, the company reported total revenue and reserve income of $770M, a 77% year-over-year increase and well above analyst expectations of $747M.

Adjusted EPS came in at $0.43, beating consensus by 22%. More strikingly, adjusted EBITDA reached $167M — nearly five times the prior year period. This represents a 412% increase, signaling not merely operational efficiency but structural scaling.

Circle’s business model is straightforward yet powerful: USDC is backed by U.S. Treasuries and high-quality liquid assets. As circulation expands, reserve balances expand. As reserve balances expand, interest income increases.

However, this quarter revealed something more important — growth is not solely dependent on yield expansion. Even as average reserve yield declined 0.68 percentage points to 3.8%, revenue surged due to supply growth and usage expansion.

This indicates that USDC is transitioning from being a passive interest vehicle to becoming an embedded financial infrastructure layer.

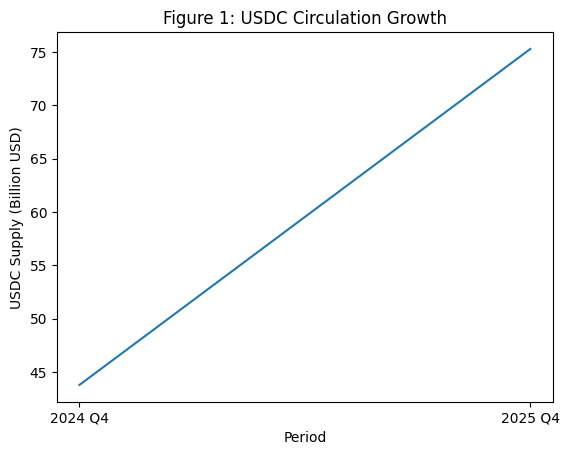

2. USDC Supply Expansion: 72% Growth to $75.3B

By year-end 2025, USDC circulation reached $75.3B, up 72% year-over-year.

USDC Circulation Growth

This level of supply growth is significant for several reasons:

- It reflects renewed institutional confidence in regulated stablecoins.

- It coincides with Circle’s 2025 IPO and increased regulatory clarity.

- It suggests capital rotation from less transparent alternatives.

USDC has increasingly positioned itself as the “compliance-first” stablecoin. As regulatory frameworks like MiCA in Europe tighten, institutional capital is likely to favor issuers with strong disclosure standards and U.S.-aligned governance structures.

While USDT remains larger in total market cap, capital quality appears to be differentiating.

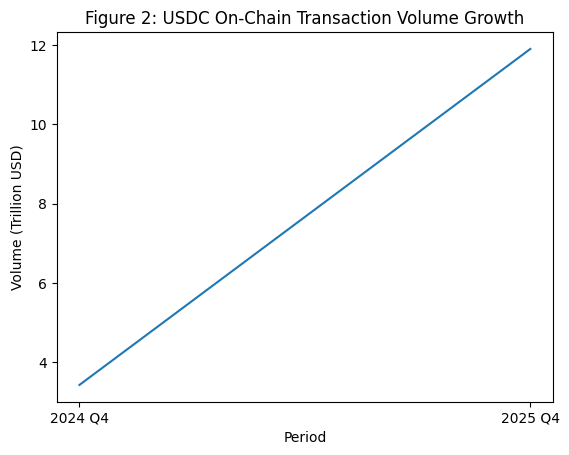

3. On-Chain Volume Explosion: $11.9T Quarterly

USDC’s on-chain transaction volume reached $11.9T in Q4 alone, a 247% year-over-year increase.

USDC On-Chain Transaction Volume Growth

This number deserves emphasis.

To contextualize:

- $11.9T quarterly volume equates to nearly $48T annualized.

- That rivals large-scale global payment networks.

- It exceeds the GDP of most countries.

What drives this surge?

- DeFi resurgence.

- Institutional settlement rails.

- Cross-border payments.

- Treasury operations by fintech and crypto exchanges.

- Machine-to-machine settlement pilots.

Stablecoins are no longer primarily trading collateral. They are becoming programmable settlement layers.

4. Reserve Revenue Model: Strength and Vulnerability

Reserve income accounted for $733M of Q4 revenue.

That is a double-edged sword.

Strength:

- Highly scalable with minimal incremental cost.

- Backed by U.S. Treasuries.

- Low operational risk compared to lending-based models.

Vulnerability:

- Yield compression directly impacts income.

- Dependence on macro interest rate cycles.

- Political risk around Treasury markets.

Circle’s management appears aware of this exposure. Their 2026 guidance projects $150M–$170M in “other revenue,” signaling a push toward diversified revenue streams.

Subscription infrastructure, payments fees, developer services, and financial API monetization are likely next-stage growth levers.

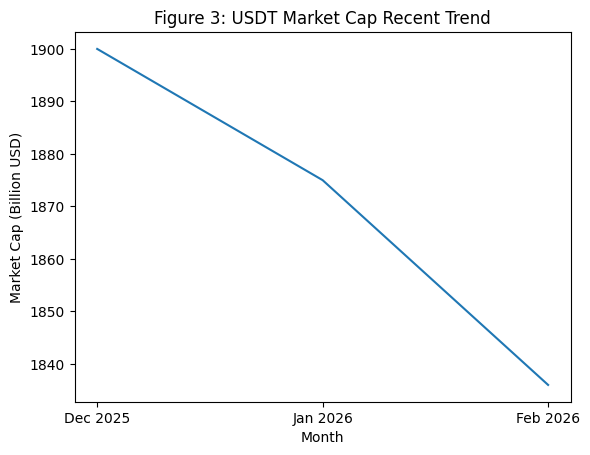

5. Tether’s Two-Month Contraction: A Warning Signal?

In contrast, Tether (USDT) has seen two consecutive months of market cap contraction, declining to approximately $1.836T as of February 2026.

USDT Market Cap Recent Trend

While USDT still dominates in absolute size, contraction in a bull-leaning environment raises questions.

Possible drivers:

- European MiCA regulatory pressure.

- Exchange delistings in stricter jurisdictions.

- Institutional preference shift toward compliant issuers.

- Liquidity rebalancing toward yield-bearing or regulated alternatives.

This does not imply structural weakness at Tether. However, momentum clearly favors Circle at this stage.

6. Arc Blockchain: Beyond Issuance

Circle is not limiting itself to token issuance.

Its proprietary blockchain initiative “Arc” has attracted over 100 institutions across banking, capital markets, and technology sectors.

Arc public testnet metrics:

- 166M+ transactions processed.

- 2.3M average daily transactions.

If Arc mainnet launches successfully in 2026, Circle could vertically integrate issuance, settlement, compliance, and smart contract infrastructure.

That would shift Circle from stablecoin issuer to financial infrastructure provider.

This transition is critical.

Infrastructure platforms command higher valuation multiples than yield-dependent issuers.

7. Circle Payments Network (CPN)

CPN now includes 55 financial institutions.

Annualized transaction volume as of Feb 20, 2026: $5.7B.

While small relative to on-chain flows, this is meaningful for regulated finance.

Strategic partnerships include:

- Visa continuous settlement integration.

- Intuit collaboration.

- Conditional national trust bank approval from the OCC.

If Circle secures full banking status, it could reduce counterparty risk, improve treasury management, and directly interface with payment networks.

That narrows the gap between crypto-native rails and traditional finance.

8. 40% Multi-Year CAGR Target: Ambitious or Realistic?

Circle targets a 40% multi-year CAGR for USDC supply.

Is this realistic?

Consider:

- Tokenized treasuries are expanding.

- Cross-border remittances remain inefficient globally.

- Stablecoins are increasingly used as dollar access in emerging markets.

- AI-driven machine commerce requires programmable settlement.

If stablecoins become the de facto digital dollar, 40% CAGR is plausible.

However, risks include:

- Central bank digital currencies.

- Interest rate normalization.

- Regulatory fragmentation.

- Competitive yield-bearing stablecoins.

9. The Emerging Stablecoin Power Balance

The stablecoin sector is entering a new phase:

Phase 1: Exchange collateral dominance.

Phase 2: DeFi integration.

Phase 3: Institutional settlement infrastructure.

Phase 4 (emerging): Embedded programmable finance.

Circle appears to be accelerating into Phase 3 and 4.

Tether remains dominant in liquidity breadth.

Circle is gaining in regulatory alignment and institutional depth.

This divergence may define the next five years.

10. Investment and Strategic Implications

For readers seeking new crypto assets, revenue opportunities, or practical blockchain use cases, this shift presents several angles:

- Infrastructure plays may outperform token speculation.

- Regulated stablecoin ecosystems may attract institutional capital.

- Payment and treasury integration tokens may gain value.

- Developers building compliance-friendly applications could benefit.

- Yield models may compress; fee models may expand.

Stablecoins are no longer “boring.”

They are becoming core financial plumbing.

Conclusion

Circle’s Q4 2025 performance marks more than a strong earnings report. It signals a structural transition in the global dollar liquidity layer.

USDC’s 72% supply growth, $11.9T quarterly transaction volume, and 412% EBITDA surge illustrate accelerating adoption. Meanwhile, Tether’s recent contraction suggests competitive rebalancing under regulatory pressure.

The critical question is no longer whether stablecoins will persist — but which issuer will dominate the programmable dollar infrastructure of the next decade.

If Circle executes on Arc, CPN expansion, and revenue diversification, it may redefine itself from stablecoin issuer to foundational financial network operator.

The stablecoin war is no longer about size alone.

It is about integration, compliance, and infrastructure control.