Main Takeaways :

- William Blair names Circle the “most important” stablecoin player, initiating coverage with an “Outperform” rating.

- USDC is seen as a potential fiat replacement in cross-border B2B payments (a $20–24 trillion market).

- Circle’s core revenue today comes from interest on USDC reserves; true upside lies in new infrastructure: CPN (Circle Payments Network) and Arc (its own L1).

- Major risks include timing of commercial adoption, interest rate regime, and regulatory clarity.

- Recent developments: Circle IPO, partnerships (Fireblocks, Safe), competition from new stablecoins, regulatory tailwinds.

1. Introduction: A New Stablecoin Vanguard

In October 2025, investment bank William Blair initiated coverage on Circle (CRCL), assigning it an “Outperform” rating and labeling it the single most important enterprise in the stablecoin ecosystem. Blair’s thesis positions Circle—and in particular USDC, the company’s flagship stablecoin—as a pivot in the shift from fiat-driven payments toward blockchain-native settlement in global commerce. This article will summarize Blair’s reasoning, combine it with recent developments, and offer an outlook for those seeking new crypto opportunities or blockchain-based real-world use cases.

2. Blair’s Core Thesis: USDC as Fiat Replacement in Global B2B Payments

2.1 Addressable Market and Conviction

William Blair sees USDC—backed one-to-one by liquid reserves and used in blockchain transfers—as a credible alternative to fiat currencies in cross-border B2B payments, a space estimated to be worth $20 to $24 trillion annually.

The argument is that conventional banking rails are slow, costly, and fragmented, while stablecoins offer programmable, near-instant, 24/7 settlement.

2.2 Revenue Model: Yield on Reserves, But Limited Scope

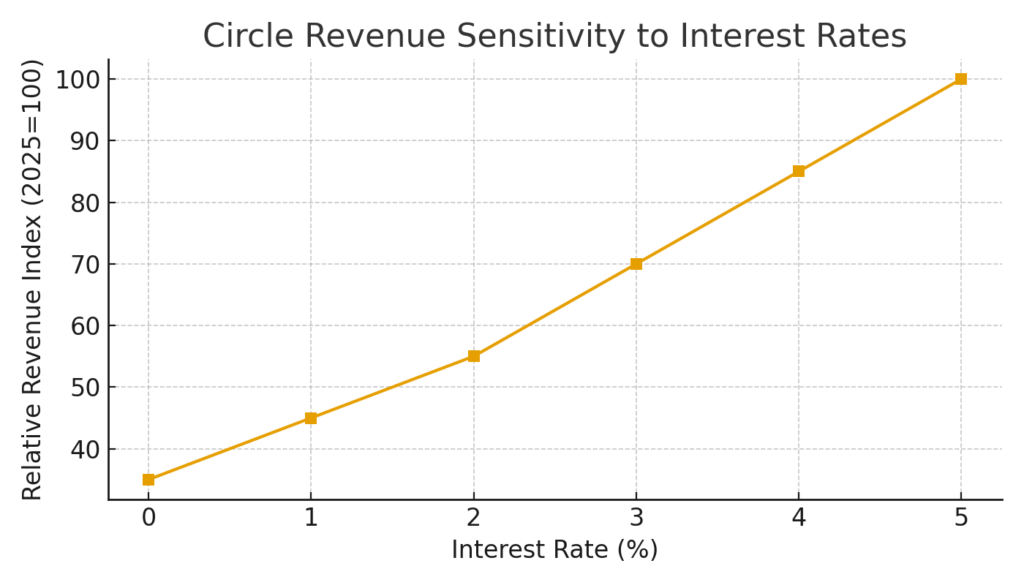

Currently, Circle derives most of its revenue by investing the reserves that collateralize USDC in short-term government securities and money-market instruments. As more institutions adopt USDC for payments, this interest income grows.

However, Blair sees that path as linear and limited. The real upside lies in transaction revenue and infrastructure monetization, especially if USDC becomes embedded in commercial workflows.

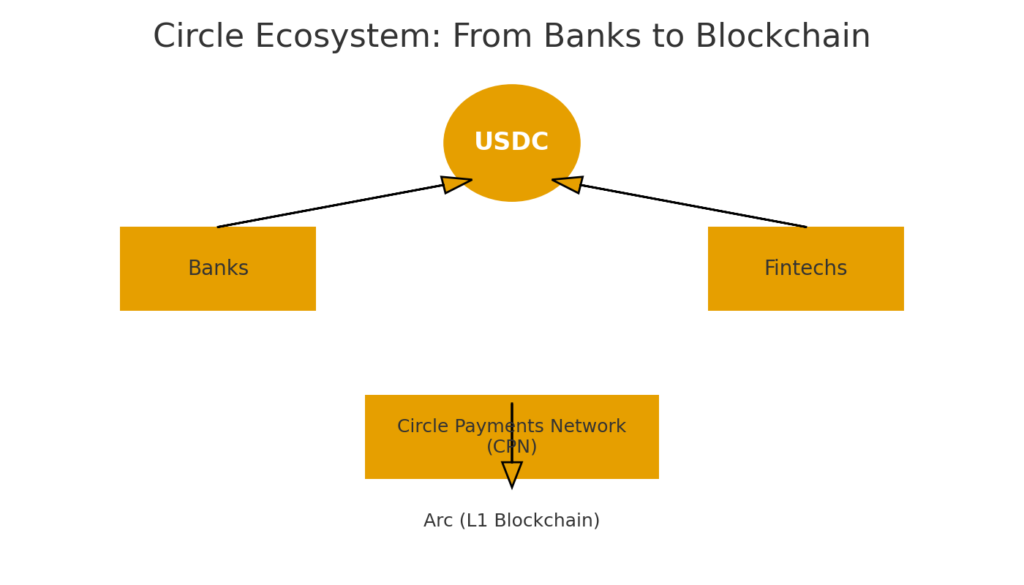

2.3 Infrastructure Bets: CPN & Arc

To bridge the gap from passive yield to active usage, Circle is building two major systems:

- Circle Payments Network (CPN): A smart-contract–based network designed to connect banks, fintechs, and blockchains, facilitating stablecoin-based cross-border payments, local fiat payout, and on-chain interoperability.

- Arc (Layer 1 blockchain): A bespoke, EVM-compatible, stablecoin-native chain intended to support low-latency settlement, built-in FX engine, composability, and interoperability for digital money and tokenized assets.

Blair sees the success of USDC’s commercial adoption as contingent on adoption of these infrastructures.

2.4 Forecasts & Valuation

Under a bullish scenario, Blair estimates:

- USDC’s market capitalization could double by 2027, reaching ~$150 billion.

- Circle’s adjusted EBITDA might exceed $1 billion, with expanding margins as the company diversifies beyond its biggest distribution partner (Coinbase).

- The current valuation—trading at ~57× projected 2026 EBITDA—is high, but Blair argues it is justified given growth potential.

3. Risks and Challenges

3.1 Timing of Commercial Adoption

Much of USDC’s current usage is still driven by crypto trading and DeFi flows, not real-world commercial payments. Transitioning to broader business use cases will take time and inertia is high.

3.2 Interest Rate Sensitivity

Because Circle’s revenue model depends heavily on interest yields, a falling interest rate environment would erode its margins. Paradoxically, though, lower rates can also reduce the opportunity cost of holding USDC vs. fiat, potentially spurring adoption. This is a double-edged sword.

3.3 Regulatory Uncertainty

While the GENIUS Act in the U.S. offers a baseline for stablecoin regulation, questions remain around how yield-bearing features will be treated, how tokens are classified, and which players can issue stablecoins.

3.4 Competitive Pressure

New entrants and incumbent platforms may issue their own stablecoins or design alternative models to capture interest revenue.

For example:

- Hyperliquid launched a native compliant stablecoin (USDH), challenging Circle’s dominance in ecosystems where yield revenue is contested.

- Circle itself responded by launching a native USDC version on HyperEVM, deepening integration into that ecosystem.

Such moves show how the competitive frontier is shifting from token issuance to embedded infra and yield capture.

4. Recent Developments: What’s New Since the Report

4.1 Going Public: IPO and Market Reception

Circle completed an IPO in June 2025, raising ~$1.05 billion and valuing the company at around $8 billion.

Upon listing as CRCL on the NYSE, shares saw strong demand, reflecting investor enthusiasm for crypto infrastructure firms.

4.2 Partnerships & Integrations

- Fireblocks formed a strategic collaboration with Circle, integrating to support Arc and enabling institutions to deploy programmable money rails with compliance.

- Safe (formerly Gnosis Safe) partnered with Circle to make USDC the default asset in institutional self-custody, combining Circle’s token infrastructure with Safe’s smart account tooling.

- CPN has seen partner growth across payments firms, banks, and remittance providers globally, leveraging network effects in cross-border rails.

4.3 Market Dynamics & Competition

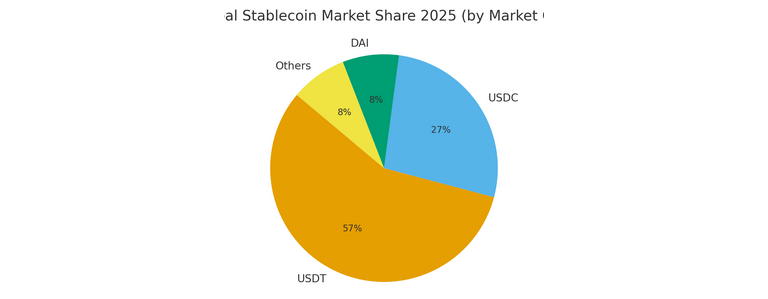

- Bernstein analysts project USDC’s market share could rise from ~27% to ~33% by 2027, and supply expanding from ~$76 billion to ~$220 billion.

- In Brazil, a local stablecoin (BRLV) backed by sovereign bonds has emerged, emphasizing yield-sharing structures that challenge traditional issuer-retained yield models.

- Tether, Circle’s main rival, also faces scrutiny and new U.S. regulatory pressures, opening room for USDC to gain ground.

4.4 Infrastructure Deployment

Arc, the stablecoin-native blockchain, is being rolled out with key design features: USDC as native gas, sub-second settlement, built-in FX engine, privacy controls, and EVM compatibility.

Fireblocks’ early support helps bring institutional adoption momentum.

5. Strategic Implications for Crypto Investors & Builders

5.1 Where to Watch for Opportunity

- Stablecoin infrastructure builders

If you are developing middleware, SDKs, compliance tools, or rails for payments and settlement, integrations with CPN or Arc may offer a strong runway. - Treasury and payments adoption plays

Companies enabling firms to adopt stablecoin-based treasury, cross-border payables, or embedded commerce could capture value downstream. - Token yield capture and monetization strategies

As platforms compete for yield flows, token models that share or route yields could emerge. Observing how yield-bearing mechanics evolve (e.g. revenue-sharing vs issuer-retained) is key. - Cross-chain and interoperability enablers

Tools bridging USDC flows across chains or enabling atomic swaps, composability, or FX hedging will become more valuable in a multi-chain stablecoin world.

5.2 What to Monitor as Risks

- Pace of enterprise adoption: will businesses move quickly or stay cautious?

- Interest rate cycles: yields may compress, affecting all margin-sensitive stablecoin issuers.

- Regulatory clarity: stablecoin classification, yield features, issuer licensing.

- Competitive disruption: new entrants issuing yield-sharing stablecoins or embedding alternative rails.

6. Outlook & Conclusion

William Blair’s initiation report frames Circle as more than a stablecoin issuer—it positions it as an ambitious pioneer building the plumbing for new financial rails. The central bet is that USDC can gradually displace fiat in cross-border B2B payments as adoption grows and the supporting infrastructure (CPN, Arc) matures.

Yet this transition is neither assured nor easy. The timing of commercial deployment, macro rate regimes, and regulatory frameworks all lie as potential headwinds. Competition is already sharpening, with new stablecoin models and ecosystems attempting to capture yield value.

For those seeking the next frontier in crypto revenue or real-world blockchain utility, Circle’s journey offers a living case study. Infrastructure-level integration, yield capture models, on-chain FX and settlement — these will be the battlegrounds of the next stablecoin era.

If USDC becomes the default money rail for commerce rather than just trading, that 57× valuation may end up looking conservative. But the path between here and there demands execution, adoption, and regulatory maturity.