Main Points:

- Circle has partnered with Mastercard to enable USDC (and EURC) settlement for merchants and acquirers in EEMEA.

- Finastra integrates USDC settlement into its Global PAYplus platform, handling over $5 trillion in daily cross-border payments.

- These collaborations significantly advance stablecoin adoption, enhancing payment efficiency, cost reduction, and settlement speed for banks and merchants worldwide.

- Circle’s strategy is bolstered by regulatory clarity via the GENIUS Act and complementary partnerships (OKX, SBI–Ripple JV, Korean banks), positioning USDC as a foundational tool in blockchain-based finance.

1. Mastercard Brings Stablecoin Settlement to EEMEA

Circle’s collaboration with Mastercard marks a watershed moment in mainstream adoption of stablecoins. Under this agreement, Mastercard will enable acquirers and merchants across Eastern Europe, the Middle East, and Africa (EEMEA) to settle transactions using USDC and Euro Coin (EURC). The first adopters of this capability are Arab Financial Services and Eazy Financial Services – a symbolic and practical step, representing Mastercard’s first-ever stablecoin settlement rollout in the region.

This innovation allows merchants to accept payments in stablecoins, which are then converted into fiat as needed – combining the advantages of blockchain settlement (speed, 24/7 availability) with the familiarity of fiat rails. It also reflects Mastercard’s intent to build a regulatory-compliant infrastructure for stablecoin usage, fostering trust and broader adoption.

2. Finastra Integrates USDC into Global PAYplus Platform

Finastra, the London-based financial software leader, has integrated Circle’s USDC into its flagship cross-border payments system, Global PAYplus (GPP). This platform currently processes more than $5 trillion in cross-border transfers daily, connecting banks across approximately 130 countries.

With the USDC integration, banks can settle international payments via stablecoins—even while maintaining fiat-denominated payment instructions—thus reducing reliance on traditional correspondent banking systems. The benefits are profound: lowered cost structures, near-instant settlement, minimized friction in FX conversion, and enhanced operational efficiency.

Chris Walters, CEO of Finastra, emphasized that this integration gives banks a bridge between legacy infrastructure and innovative blockchain-enabled financial models without needing to build entirely new systems.

3. Strategic Momentum: Regulatory and Institutional Backing

Circle’s surge in partnerships is closely tied to the regulatory clarity provided by the U.S. GENIUS Act, enacted in July – the first federal stablecoin framework in the country. This legislative backdrop has emboldened Circle’s expansion strategy.

In late July, Circle announced a partnership with OKX, providing zero-fee USDC-to-USD conversions, enhancing global liquidity for USDC in Asia, Europe, and the Middle East.

In August, Circle engaged with the CEOs of South Korea’s four largest banks—KB Kookmin, Shinhan, Hana, Woori—to explore on-chain integration and the potential issuance of a won-backed stablecoin.

Furthermore, in Japan, Circle joins forces with SBI Group, Ripple, and Startale in a joint venture to promote USDC adoption and develop a tokenized real-world asset trading platform.

These multi-regional efforts showcase Circle’s holistic approach: aligning regulatory clarity, institutional partnerships, and technical integration to cement USDC’s role in global finance.

4. Why These Partnerships Matter for Blockchain Practitioners and Crypto Seekers

For blockchain developers, crypto entrepreneurs, and innovative finance professionals, these developments are transformative:

- Payment Efficiency Redefined: Traditional cross-border payments can take days and cost tens of dollars. Stablecoin settlement offers near-instant transfers at a fraction of the cost.

- 24/7 Liquidity and FX Flexibility: Settling in USDC bypasses banking hour limitations and simplifies foreign exchange logistics.

- Institutional Confidence: Tight regulatory compliance, fully reserved backing, and transparency make USDC a trustworthy tool for institutional players.

- Scalable Infrastructure Integration: Finastra’s existing network of 8,000+ clients and 130 countries means this isn’t experimental—it’s live infrastructure.

- Global Reach: Mastercard’s merchant network spans millions globally, while Finastra connects banks—together enabling blockchain-native settlement across finance’s core arteries.

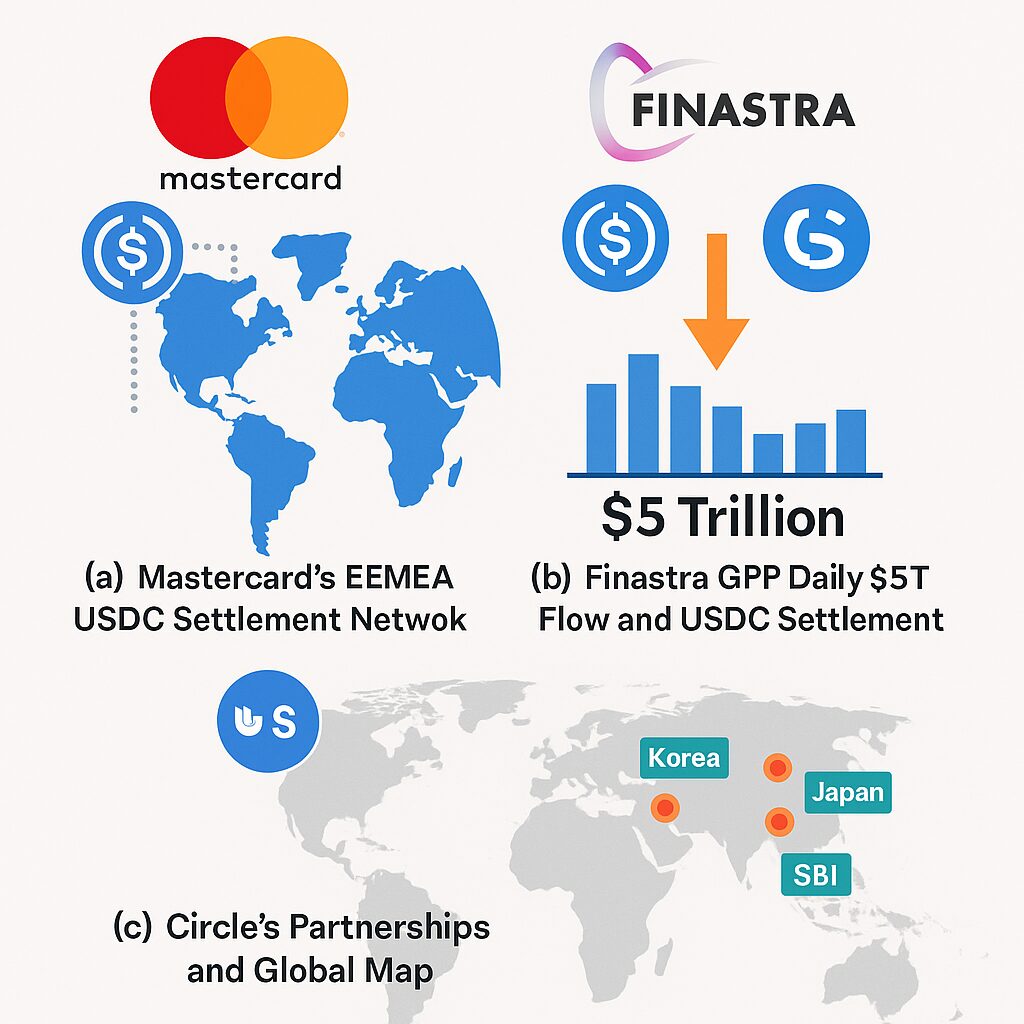

Visual Aid Placeholder

— Chart illustrating: (a) Mastercard’s EEMEA USDC settlement network; (b) Finastra GPP daily $5T flow and USDC settlement overlay; (c) global map of Circle’s partnerships (OKX, Korean banks, SBI/Japan).

5. Conclusion: A Turning Point for Stablecoins in Real-World Finance

Circle’s strategic partnerships with Mastercard and Finastra herald a pivotal shift: stablecoins like USDC are not just speculative digital assets—they are fast becoming the backbone of efficient, secure, global payment systems. By embedding USDC into established payment infrastructure—merchant networks and bank rails alike—Circle bridges traditional banking and blockchain innovation.

The combination of regulatory clarity (GENIUS Act), institutional trust (transparent backing), and infrastructural depth (Global PAYplus, Mastercard network, OKX liquidity) positions USDC as a foundational tool for the next wave of financial transformation.

For innovators exploring new revenue sources, blockchain application, or crypto-enabled services, this moment provides fertile ground. Whether designing on‑chain payment systems, tokenizing real-world assets, or building new fintech solutions, Circle’s USDC integrations offer unprecedented access to real‑time settlement across traditional finance.