Main Points :

- A Beijing court has sentenced five individuals to prison terms of two to four years for executing disguised foreign-exchange transactions worth over US$166 million, converting yuan into Tether (USDT) and transferring the proceeds abroad.

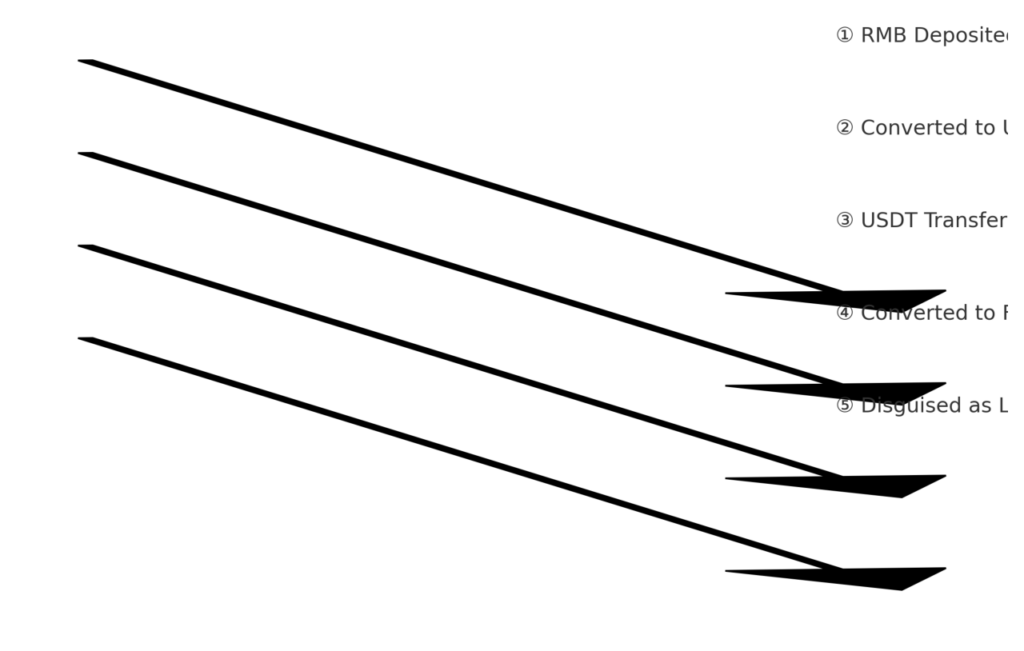

- The scheme involved domestic bank-account inflows of RMB, conversion into USDT via trading platforms, and cross-border transfers under the guise of foreign-exchange trade, thereby evading China’s capital‐control regime.

- The investigation utilised a “data-driven, tech-enabled” strategy: tracing blockchain flows, matching crypto movements with bank records, and reconstructing end-to-end chains of illicit transactions.

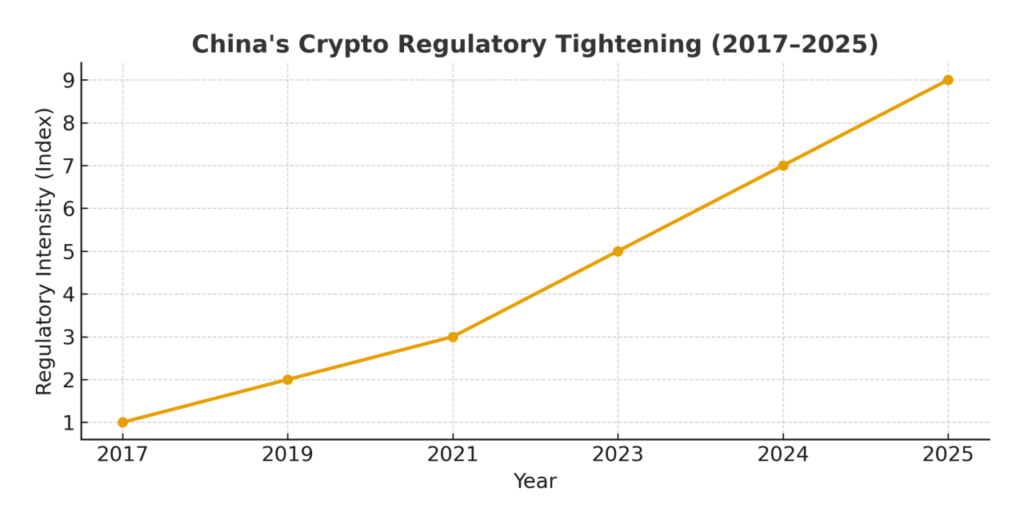

- These developments reflect a broader regulatory tightening in China: new foreign‐exchange rules effective end of 2024 require banks to monitor and report suspicious crypto-linked transfers, underpinning enhanced scrutiny of digital-asset activity.

- For crypto investors, project developers and blockchain practitioners seeking new assets or use-cases, this signals increased regulatory risk in China’s ecosystem and underscores the need for compliance, transparent flows and jurisdictional awareness.

1. Background of the Case

In a landmark enforcement action, a court in Beijing sentenced five individuals for orchestrating a complex scheme that converted Chinese RMB into USDT and transferred those funds beyond mainland China in order to bypass the country’s stringent foreign exchange controls.

Between January and August 2023 the group collected domestic‐bank-account deposits in RMB, converted them into USDT via multiple trading platforms, and then moved the currency across borders, masquerading the activity as foreign-exchange transactions.

The verdict, summarised in the “Financial Procuratorial High-Quality Case Report (2024–2025)”, imposes prison sentences of two to four years and fines.

This prosecution not only signals Beijing’s determination to police crypto-enabled flows, but also illuminates the mechanics of how stablecoins like USDT are being used in cross-border capital movement and forex arbitrage.

2. Mechanics of the Scheme: How Crypto Facilitated Illicit FX

The scheme’s structure offers instructive insight:

- Domestic actors receive large RMB deposits into bank accounts, often from clients or participants inside China.

- These funds are converted into USDT on various trading platforms. USDT, being dollar-pegged and globally tradable, serves as a bridge currency.

- The USDT is then moved across borders (either via exchanges or peer-to-peer/OTC networks), converted into foreign fiat or other assets, and thus the original funds exit the jurisdiction disguised as legitimate foreign‐exchange flows.

- The disguised foreign‐exchange nature arose because Chinese regulation prohibits domestic RMB conversion and outbound transfers except via approved channels; by using crypto the parties sidestepped those controls.

- Importantly, the prosecutors emphasised how blockchain tracing, bank-records reconciliation and platform-activity matching allowed reconstruction of the full chain, which was previously a major enforcement challenge.

For blockchain and crypto practitioners, this case underscores how ostensibly “permissionless” assets like USDT can become vectors for capital‐control arbitrage and how regulatory authorities are acquiring the tools to trace them.

3. Regulatory Shift in China: Crypto + Forex = High Surveillance

While China has long maintained a difficult relationship with cryptocurrencies—ban on trading since 2021, prohibition of mining operations, and forced closures of exchanges—recent enforcement efforts reveal a sharper focus on how crypto intersects with cross‐border capital flows and foreign‐exchange (FX) regulation.

Key regulatory developments:

- At the end of 2024 the State Administration of Foreign Exchange (SAFE) issued rules requiring banks to monitor and report transactions involving digital assets, “risky” FX trades and cross‐border transfers implicating crypto.

- Authorities emphasise that converting RMB into cryptocurrencies and then sending value abroad constitutes a disguised FX transaction, which is subject to the same prohibitions and penalties as traditional capital flight.

- Experts point out that the tools developed in this Beijing case are intended to serve as models for crime prevention in the “digital economy” and virtual-asset ecosystem.

Thus for any entity operating in or targeting Chinese market flows, the regulatory landscape is evolving: participation in digital-asset markets is no longer just about local trading bans, but about how crypto may be used for FX-related compliance triggers and cross‐border oversight.

4. Implications for Crypto Asset Investors & Use-Cases

For our readers—those seeking new crypto assets, alternative revenue streams, and practical blockchain applications—the following implications arise:

a) Heightened Regulatory Risk in China-China-adjacent Flows

Projects, tokens or platforms that rely on RMB-based in-flows or China-based investors must factor in that authorities now consider crypto conversions + outbound movements as FX violations. The cost of non-compliance (investigations, freezing of funds, reputational damage) is rising.

b) Stablecoin Utility & Jurisdictional Risk

The use of stablecoins—especially dollar-pegged ones like USDT—in facilitating cross-border “capital escape” has attracted regulatory focus. Entities leveraging stablecoin rails for movement of value must consider both blockchain-traceability and counter-party location risk.

c) Use-cases with legitimate cross-border utility

While illicit flows trigger enforcement, legitimate cross-border value transfer cases (for example payments for trade, settlement of services, tokenised assets) may still progress—but require robust compliance, transparency and audit trails. The case shows authorities are capable of reconstructing chains, so best‐practice audit logs and KYC/AML frameworks become increasingly important for any blockchain use-case.

d) Diversification of Jurisdictional Strategy

Given China’s heavy-handed stance, developers or investors might prefer jurisdictions with clearer enabler regulatory frameworks rather than opaque or high-risk ones. Projects focused solely on China may face structural headwinds.

5. Recent Trends & Outlook Beyond the Case

This enforcement action fits into wider global trends in digital-asset oversight:

- China’s crackdown on crypto for FX and capital-flight purposes is consistent with its broader emphasis on financial stability and capital-control enforcement.

- While China forbids many forms of crypto activity in the mainland, other jurisdictions (e.g., Hong Kong) are positioning themselves as digital-asset hubs, potentially offering alternative markets for blockchain innovation.

- From the investor’s vantage: this may lead to liquidity migration, projects pivoting away from China-centric models toward Southeast Asia, Europe or North America.

For those seeking new assets or blockchain application opportunities, this means: focus on regulatory clarity, on-chain transparency, and cross-border compliance architecture from day one.

6. Conclusion

The convicted case in Beijing—five individuals sentenced over US$166 million in crypto-enabled disguised foreign exchange transactions—is a sharp reminder that the intersection of digital assets and capital flows is now in regulatory spotlight. For blockchain technologists, token issuers and crypto investors, the implications are clear: jurisdiction matters, transparency counts, and the days of “crypto as untraceable capital flight” are fading. To seize the next wave of crypto opportunity, one must build with compliance in mind and craft use-cases that align with legitimate cross-border value transfer or digital-asset innovation rather than regulatory avoidance.