Main Points :

- China has formally revised the operating rules of CIPS (Cross-Border Interbank Payment System) to strengthen oversight and scalability ahead of 2026.

- The new framework clearly separates real-time gross settlement (RTGS) for single transactions and timed net settlement for batch transactions.

- This change aligns CIPS more closely with global payment infrastructure standards while preserving centralized control under the People’s Bank of China.

- The reform has important implications not only for traditional banking, but also for stablecoins, blockchain settlement layers, and cross-border crypto–fiat bridges.

- For investors and builders, the update signals how China intends to compete with SWIFT, shape RMB internationalization, and define the boundary between state-led payments and decentralized finance.

1. Introduction: A Strategic Update, Not a Minor Technical Fix

On December 26, 2025, the People’s Bank of China announced a formal revision of the operating rules governing CIPS, China’s Cross-Border Interbank Payment System. While the announcement may appear technical on the surface, it represents a significant evolution in how China manages cross-border RMB (renminbi) settlement.

CIPS, launched in 2015, was originally designed to support offshore RMB clearing and settlement. Over the past decade, however, the system has expanded dramatically in both transaction volume and the number of participating institutions. As cross-border RMB usage has grown across trade, investment, and financial transactions, the limitations of the original rules have become increasingly apparent.

The newly revised framework, aimed at full implementation toward 2026, formally introduces a hybrid settlement model. Single transactions are processed through real-time gross settlement (RTGS), while batch transactions are handled via timed net settlement. This design is intended to enhance systemic stability, reduce settlement risk, and improve liquidity efficiency—all while allowing regulators greater flexibility in managing system-wide stress.

2. How the New CIPS Settlement Model Works

2.1 Two Clearly Separated Settlement Paths

Under the revised rules, CIPS transactions now follow two explicitly defined settlement routes:

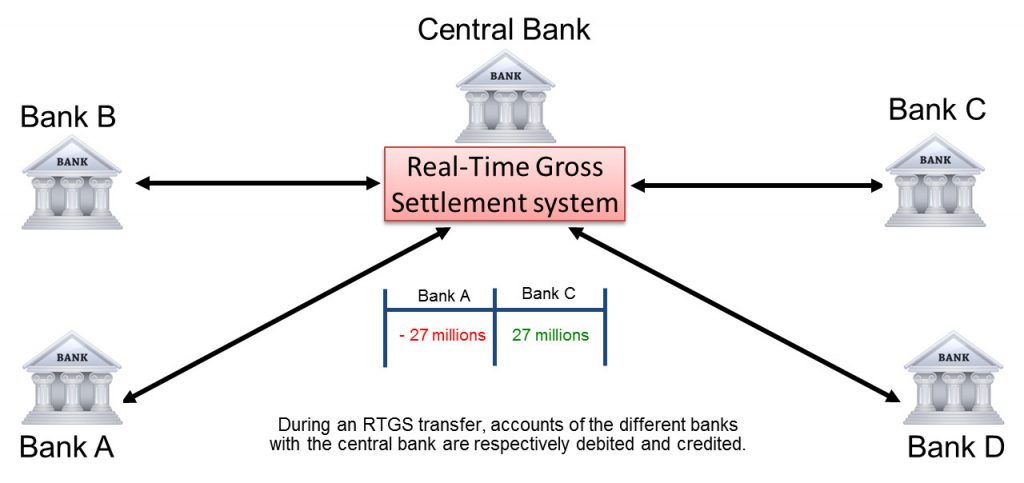

- Real-Time Gross Settlement (RTGS)

Individual cross-border RMB transactions are settled one by one, in real time, and with immediate finality. Once settled, transactions are irrevocable. - Timed Net Settlement for Batch Transactions

High-volume batch payments are aggregated and processed at scheduled intervals. Obligations are netted against each other, reducing the total liquidity required by participants.

This separation reflects best practices seen in major international payment systems, where immediacy and risk reduction for critical payments are balanced against efficiency and liquidity optimization for bulk flows.

2.2 Why This Matters for Systemic Risk

By enforcing RTGS for single transactions, CIPS reduces counterparty risk. Participants no longer face uncertainty about whether a payment will be reversed or delayed. At the same time, netting batch transactions significantly lowers liquidity pressure, especially during peak settlement periods.

The revised rules also grant CIPS operators the authority to dynamically adjust:

- Netting frequency

- Settlement windows

- Processing schedules

This flexibility allows regulators to respond to changes in transaction volume or market stress without rewriting the system’s legal foundation.

CIPS Hybrid Settlement Structure (RTGS vs Timed Net Settlement)

3. Operational Governance and Regulatory Control

3.1 Centralized Oversight Remains Intact

Despite the structural modernization, oversight of CIPS remains firmly centralized. The People’s Bank of China continues to supervise system rules, risk management standards, and settlement discipline.

Historically, Chinese authorities have demonstrated a willingness to adjust payment infrastructure rules during periods of market stress. Examples include reforms following the global financial crisis and incremental enhancements aligned with the internationalization of the RMB.

Importantly, the latest revision does not introduce a new payment system. Instead, it formalizes practices that were already being applied operationally, bringing them under a clearer and more enforceable regulatory framework.

3.2 Alignment with Global Standards—on China’s Terms

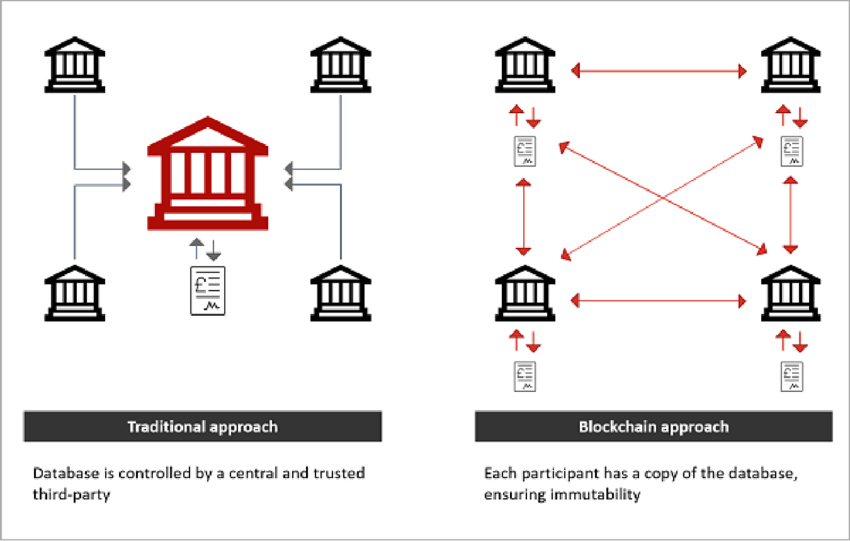

While CIPS is increasingly aligned with international settlement standards, it differs fundamentally from systems like SWIFT. SWIFT primarily functions as a messaging network, whereas CIPS directly integrates clearing and settlement.

This distinction is crucial: China is not merely improving interoperability with global finance—it is building a vertically integrated alternative where messaging, clearing, and settlement are coordinated under sovereign oversight.

4. Implications for RMB Internationalization

4.1 Strengthening Trust Through Predictability

For cross-border users—banks, corporates, and financial institutions—predictability is as important as speed. The revised rules aim to ensure that even during peak periods, settlement outcomes remain stable and foreseeable.

This is particularly relevant for trade finance and large-scale investment flows, where settlement delays can cascade into operational and financial risk.

4.2 Competitive Positioning Against Dollar-Dominated Systems

Although the U.S. dollar remains dominant in global settlement, China’s incremental improvements to CIPS reflect a long-term strategy: reduce reliance on dollar-based infrastructure while increasing the RMB’s appeal as a settlement currency.

As of recent estimates, cross-border RMB payments remain a fraction of global volumes dominated by USD and EUR, but their absolute value—measured in the trillions of dollars annually—continues to grow.

Global Cross-Border Payment Systems: SWIFT vs CIPS vs Blockchain Rails

5. What This Means for Crypto, Stablecoins, and Blockchain Settlement

5.1 A State-Led Counterpoint to Decentralized Finance

For readers interested in blockchain and digital assets, the CIPS revision offers a revealing contrast. While decentralized networks emphasize permissionless access and trust minimization, CIPS demonstrates how state-led systems evolve to absorb efficiency gains without relinquishing control.

This raises important questions:

- Where will stablecoins fit in a world of increasingly efficient sovereign payment rails?

- Can blockchain-based settlement coexist with systems like CIPS, or will they be regulated into narrow use cases?

5.2 Stablecoins as the “Neutral Layer”

In practice, many cross-border transactions today rely on USD-denominated stablecoins as a bridge asset. If RMB-backed or offshore RMB-linked stablecoins emerge under strict regulatory oversight, they could complement CIPS rather than compete with it.

However, China’s approach suggests that any such instruments would likely be tightly integrated with existing infrastructure, rather than operating as open, permissionless networks.

5.3 Opportunities for Builders and Investors

For entrepreneurs and investors, the signal is clear: infrastructure matters. Systems that can interface with multiple settlement regimes—traditional RTGS, net settlement, and blockchain rails—will be best positioned to capture future growth.

Rather than replacing banks or central systems outright, blockchain technology may increasingly serve as a middleware layer, enabling transparency, reconciliation, and programmability on top of state-controlled settlement backbones.

Future Cross-Border Settlement Stack: Banks, CIPS, Stablecoins, and Blockchain

6. Conclusion: A Quiet but Powerful Signal

China’s revision of the CIPS operating rules is not a dramatic overhaul, nor is it an attempt to disrupt global finance overnight. Instead, it is a carefully calibrated upgrade—one that prioritizes stability, scalability, and regulatory control.

For those searching for the next wave of opportunity in crypto and blockchain, the lesson is nuanced. Innovation does not occur only at the edges of decentralization. It also unfolds within—and alongside—state-led systems that quietly redefine the rules of global settlement.

As cross-border payments continue to evolve, the most successful strategies will be those that understand both worlds: the disciplined precision of systems like CIPS and the transformative potential of blockchain-based finance.