Main Points:

- China’s government, led by the People’s Bank of China (PBOC), is evaluating a yuan-pegged stablecoin to reduce dollar dependency and support the renminbi’s global role.

- Hong Kong’s new Stablecoins Bill, effective August 1, 2025, will issue a limited number of licenses for fiat-backed tokens, acting as a pilot zone.

- Only one of China’s four state-owned banks is expected to secure an initial license amid strict anti–money laundering and reserve adequacy criteria.

- Offshore yuan-denominated stablecoins are under consideration, with Hong Kong already accounting for 41% of the offshore RMB market in 2024 (Figure 1).

- Capital flight concerns and regulatory caution mean China’s stablecoin growth may lag U.S. dollar–backed counterparts.

- Market opportunities exist for crypto investors seeking yield products, trade-finance improvements, and blockchain-based payment efficiencies.

Introduction: Strategic Drivers Behind China’s Stablecoin Move

China’s central bank, the PBOC, under Governor Pan Gongsheng, is weighing the creation of a yuan-pegged stablecoin as part of a broader effort to internationalize the renminbi and challenge the U.S. dollar’s dominance in global payments. In June, Pan lauded stablecoins for their capacity to “fundamentally transform traditional payment systems”. The push follows Hong Kong’s enactment of the Stablecoins Bill in May 2025, which legalizes fiat-backed token issuance and establishes stringent regulatory requirements.

Despite a continued ban on private cryptocurrency trading on the mainland, Beijing sees state-backed stablecoins as a tool to facilitate cross-border payments, enhance trade finance, and potentially stem capital outflows by offering an on-chain alternative to USD-pegged digital assets.

Hong Kong’s Regulatory Framework: A Pilot for Stablecoin Innovation

Hong Kong’s Stablecoins Ordinance, to take effect August 1 2025, will grant “a few” licenses to issuers that meet rigorous criteria covering AML protocols, reserve transparency, and redemption processes. Applications opened in early August and will remain open for three months; approved entities can continue operations under provisional status until January 31, 2026.

The Hong Kong Monetary Authority (HKMA) has signaled a cautious rollout: only a single-digit number of licenses will be granted initially, with antipathy toward market speculation guiding its conservative approach. This regulatory sandbox aims to ensure stability before broader adoption, focusing on business-to-business use cases such as trade and institutional payments.

State-Owned Banks in Focus: Limited Initial Participation

Within China’s banking sector, only one of the “Big Four” state-owned banks is expected to receive a stablecoin license in the first phase, reflecting Beijing’s tight control over capital outflows and compliance monitoring. State-linked enterprises have shown interest, but regulators insist that “all stablecoin projects implemented in China must align with national conditions,” ensuring any issuance remains under state oversight.

This selective licensing strategy underscores the government’s dual objectives: leveraging blockchain innovation for international payments while preserving capital controls that guard against rapid outflows and speculative use.

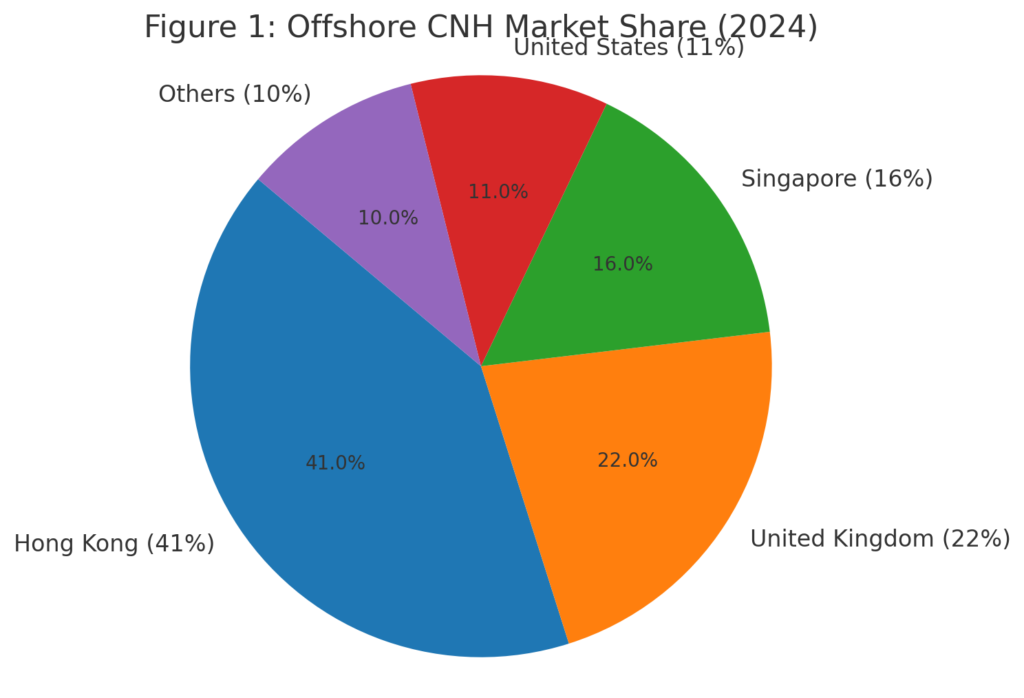

Offshore Yuan Stablecoins: Expanding the Renminbi’s Reach

In parallel, Chinese authorities are considering offshore renminbi (CNH)–backed stablecoins. Hong Kong, the primary CNH hub, accounted for 41% of the offshore RMB trading volume in 2024, followed by the U.K. (22%), Singapore (16%), the U.S. (11%), and other centers (10%).

Insert Figure 1 here

This pie chart illustrates the geographic distribution of offshore CNH transactions, highlighting Hong Kong’s central role. By enabling CNH stablecoins, China aims to streamline cross-border settlement, reducing reliance on traditional correspondent banking and SWIFT channels.

Market Dynamics and Investor Opportunities

Although China’s stablecoin ecosystem will initially trail U.S. dollar–denominated giants like Tether (USDT) and USD Coin (USDC), opportunities abound for crypto investors and institutions:

- Yield Generation: Stablecoins can earn interest on reserve holdings, a lucrative model adopted by tech firms such as Ant Group, which views reserve yields and transaction fees as recurring revenue streams.

- Trade Finance Efficiency: For exporters paying transaction fees, renminbi-pegged tokens can lower costs and settlement times compared to traditional banking channels.

- Diversification: Portfolio managers seeking reduced volatility may allocate to state-backed digital assets, balancing BTC or ETH positions with low-volatility stablecoins.

However, investors must account for regulatory risk, possible liquidity constraints, and slower adoption due to strict licensing.

Recent Developments: Global and Domestic Trends

- Hong Kong Fundraising Surge: In July 2025, Hong Kong fintech firms raised over $1.5 billion in equity for crypto and stablecoin ventures, reflecting robust investor appetite despite regulatory caution.

- International Regulatory Momentum: Jurisdictions such as Singapore and the EU are advancing stablecoin frameworks, highlighting a global shift toward regulated digital assets. Singapore’s Monetary Authority launched its stablecoin pilot program in late 2024, emphasizing sandbox testing and cross-border collaboration.

- Technology Integration: Major Chinese exchanges and tech giants (e.g., JD.com, Ant Group) are preparing license applications via Hong Kong entities, aiming to leverage blockchain rails for capital-efficient cross-border transfers.

Conclusion: Strategic Outlook for Blockchain Practitioners

China’s measured entry into the stablecoin arena represents a pivotal moment in the asset’s evolution. For practitioners seeking novel crypto assets and revenue sources, state-backed stablecoins offer a unique blend of regulatory security and blockchain efficiency. While the initial rollout in Hong Kong will be limited, its success could catalyze broader adoption across Asia and beyond, gradually challenging the dollar’s primacy in digital settlements. Market participants should monitor licensing developments, reserve management policies, and cross-border liquidity as key indicators of the ecosystem’s maturation.