Main Points :

- The U.S. Securities and Exchange Commission (SEC) staff has clarified that broker-dealers may apply a 2% haircut to certain stablecoins instead of a 100% deduction for net capital purposes.

- This change significantly improves capital efficiency for Wall Street firms holding dollar-backed stablecoins.

- The clarification aligns stablecoins more closely with low-risk cash equivalents such as U.S. Treasuries and money market instruments.

- Stablecoin market capitalization remains near $295 billion, reflecting sustained structural growth since 2023.

- The passage of the GENIUS Act under President Donald Trump provided additional regulatory legitimacy to the stablecoin sector.

- Despite regulatory progress, skepticism remains among some policymakers, including Minneapolis Fed President Neel Kashkari.

- The decision could accelerate tokenized securities markets, real-world asset (RWA) adoption, and institutional blockchain integration.

1. The SEC’s 2% Haircut: A Quiet but Structural Shift

In a move that may prove more consequential than headline-grabbing enforcement actions, the U.S. Securities and Exchange Commission (SEC) staff last week clarified that broker-dealers may apply a 2% “haircut” to certain dollar-backed stablecoins when calculating net capital requirements.

Previously, industry participants struggled with the possibility that stablecoins could receive a 100% haircut under existing interpretations. Such treatment would have meant that broker-dealers could not count any portion of their stablecoin holdings toward required net capital. In practical terms, this effectively discouraged regulated financial institutions from holding stablecoins at scale.

The clarification was issued through the SEC Division of Trading and Markets in an updated FAQ concerning crypto asset activities and distributed ledger technology.

Commissioner Hester Peirce welcomed the clarification, stating that a 100% haircut was unnecessarily punitive given the reserve assets backing payment stablecoins. Her view reflects a growing recognition within parts of the regulatory community that properly structured stablecoins resemble short-duration, low-risk dollar instruments.

Under the new interpretation, if a broker-dealer holds $100 million in qualifying stablecoins, it may count $98 million toward its net capital requirement after applying a 2% haircut.

This seemingly small numerical adjustment fundamentally alters institutional incentives.

2. Why Net Capital Treatment Matters for Wall Street

To understand the significance, one must examine how U.S. broker-dealer capital rules function.

Broker-dealers must maintain minimum net capital to absorb potential losses from market volatility or operational risks. Assets deemed volatile or illiquid receive larger “haircuts,” reducing their capital value. Assets considered safe and liquid receive smaller deductions.

A 100% haircut would have categorized stablecoins as fully non-qualifying assets. A 2% haircut places them in a risk bucket more comparable to short-term Treasuries or money market instruments.

This adjustment:

- Reduces regulatory capital friction.

- Improves balance sheet flexibility.

- Enables institutional participation in tokenized asset markets.

- Makes stablecoins viable settlement instruments inside regulated entities.

From a capital efficiency standpoint, this is transformative.

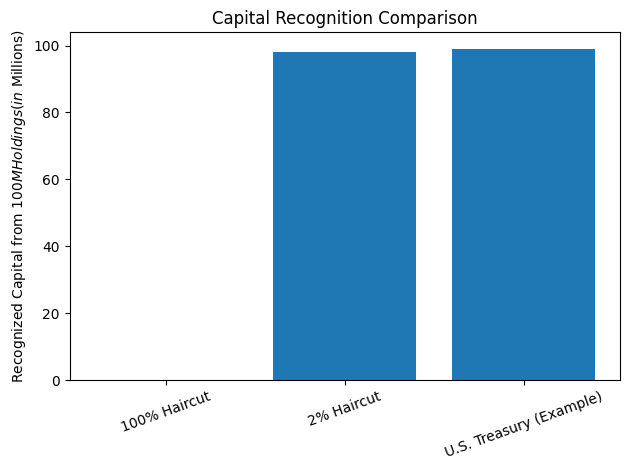

3. Visual Breakdown: Haircut Comparison

The graph should illustrate:

- Scenario A: 100% haircut → $0 counted toward capital.

- Scenario B: 2% haircut → $98 million counted from $100 million holdings.

- Scenario C: U.S. Treasury (for comparison) → ~$99 million counted.

This visual demonstrates how closely stablecoins now resemble traditional low-risk financial instruments in regulatory treatment.

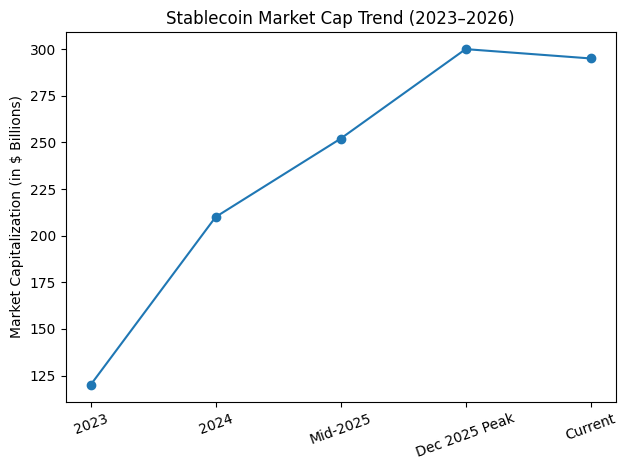

4. Stablecoin Market Growth: Structural, Not Speculative

According to industry data aggregators such as RWA.XYZ, the stablecoin market currently stands at approximately $295 billion.

While this represents a decline of roughly $6 billion from its December 2025 peak above $300 billion, the broader trend since 2023 shows steady structural growth rather than speculative mania.

The chart should show:

- 2023: ~$120 billion

- 2024: ~$210 billion

- Mid-2025: ~$252 billion

- Peak Dec 2025: ~$300 billion

- Current: ~$295 billion

The data illustrates resilience and sustained institutional adoption.

Unlike prior crypto cycles driven by leverage and retail speculation, this expansion is driven by:

- Cross-border payments.

- On-chain settlement for exchanges.

- Tokenized U.S. Treasury funds.

- Corporate treasury allocation experiments.

- Emerging market dollar access.

5. The GENIUS Act and Regulatory Legitimacy

In July 2025, President Donald Trump signed the GENIUS Act into law. While details vary across summaries, the law is widely described as a landmark stablecoin regulatory framework.

At the time of signing, stablecoin market capitalization stood just above $252 billion. Following passage, the market expanded rapidly toward $300 billion.

The legislation provided:

- Clear definitions for payment stablecoins.

- Reserve backing standards.

- Reporting requirements.

- Oversight clarity.

Regulatory certainty often acts as a catalyst for capital inflows. In this case, it provided confidence to institutions previously hesitant to engage deeply with on-chain dollars.

The SEC’s 2% haircut clarification builds upon that foundation.

6. Implications for Tokenized Securities and RWAs

Commissioner Peirce noted that stablecoins are essential for blockchain-based transactions. This statement points toward the larger structural transformation underway: tokenization.

Stablecoins serve as:

- Settlement rails for tokenized equities.

- Collateral in decentralized finance (DeFi).

- Liquidity bridges between traditional finance and on-chain assets.

- Base pairs in crypto exchanges.

With improved capital treatment, broker-dealers may now:

- Custody stablecoins directly.

- Facilitate tokenized bond issuance.

- Participate in RWA marketplaces.

- Operate hybrid on-chain/off-chain trading desks.

This opens revenue streams in:

- Digital prime brokerage.

- Tokenized fixed income markets.

- Cross-border institutional payments.

- Blockchain-native custody services.

For readers seeking new income sources, this regulatory shift signals where institutional capital is likely to flow next.

7. Skepticism Persists: The Kashkari Perspective

Despite these developments, skepticism remains.

Minneapolis Federal Reserve President Neel Kashkari recently questioned the practical utility of stablecoins, arguing that services like Venmo, PayPal, and Zelle already enable fast dollar transfers.

This critique reflects a traditional payments perspective. However, it may overlook three structural distinctions:

- Programmability: Stablecoins can integrate into smart contracts.

- Global Accessibility: They function without domestic banking rails.

- 24/7 Settlement: No reliance on banking hours.

The debate highlights a broader philosophical divide: are stablecoins merely redundant payment tools, or foundational infrastructure for programmable finance?

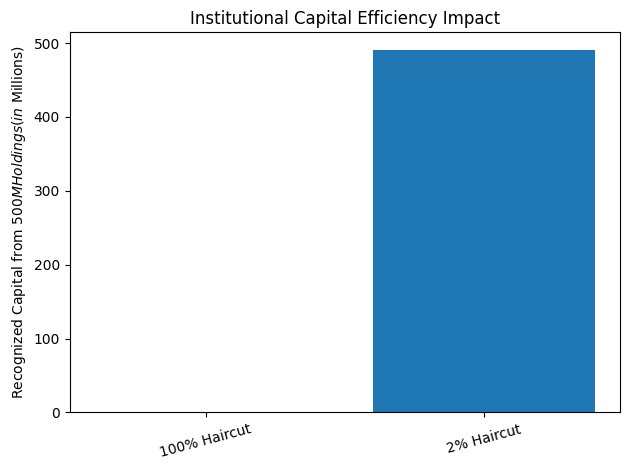

8. Capital Efficiency and Institutional Adoption

The 2% haircut rule effectively lowers the cost of participation.

For broker-dealers managing billions in balance sheet exposure, even marginal capital efficiency gains translate into significant return-on-equity improvements.

If we assume:

- A firm holds $500 million in stablecoins.

- Under 100% haircut → $0 capital recognition.

- Under 2% haircut → $490 million recognized.

The difference materially affects leverage capacity and business model viability.

This may lead to:

- Increased on-chain settlement desks.

- Stablecoin-based repo experimentation.

- Institutional DeFi integration.

- Dollar liquidity provisioning in tokenized markets.

9. Strategic Outlook for Investors and Builders

For investors and blockchain operators, the implications are layered:

Short-term:

- Positive sentiment around regulated stablecoins.

- Increased institutional custody demand.

- Potential new issuance of compliant dollar tokens.

Medium-term:

- Expansion of tokenized Treasury products.

- Broker-dealer integration of blockchain infrastructure.

- Growth in real-world asset tokenization.

Long-term:

- Stablecoins functioning as global shadow dollar system.

- Convergence between broker-dealer regulation and crypto-native markets.

- Institutional-grade on-chain capital markets.

This is not merely about a 2% accounting adjustment. It is about regulatory acknowledgment that stablecoins are becoming core infrastructure.

10. Conclusion: A Technical Adjustment with Strategic Consequences

The SEC’s clarification allowing a 2% haircut on stablecoins may appear technical, but it represents a pivotal shift in regulatory posture.

By moving stablecoins from a punitive 100% deduction to near-cash-equivalent treatment, the SEC has:

- Improved capital efficiency.

- Reduced institutional friction.

- Enabled tokenized securities markets.

- Strengthened the regulatory legitimacy of on-chain dollars.

While skepticism remains, particularly from traditional central banking voices, the direction of travel is clear.

Stablecoins are no longer peripheral experiments.

They are becoming embedded components of the global dollar system.

For readers seeking the next wave of blockchain opportunity, watch where regulated capital flows. Infrastructure plays—custody, settlement, tokenization, compliance tooling—may offer more durable upside than speculative tokens.

The 2% haircut is not just a regulatory footnote.

It is a signal.