Main Points :

- The Bank of Canada has clarified strict requirements for stablecoins ahead of formal regulation planned for 2026.

- Only 1:1 pegged stablecoins, fully redeemable at par value and backed by high-quality, liquid government assets, are likely to be acceptable.

- Transparency, consumer protection, and operational resilience are emphasized as core design principles.

- The framework aligns Canada with global trends in stablecoin regulation, while preserving space for innovation in payments and blockchain-based finance.

- For investors, developers, and fintech operators, the message is clear: regulated stablecoins will increasingly resemble narrow banking instruments rather than experimental crypto assets.

Introduction: Why Canada’s Stablecoin Stance Matters

Stablecoins have moved from a niche crypto experiment to a core component of digital payments, decentralized finance (DeFi), and cross-border settlement. Yet, as their scale has grown, so too have concerns around financial stability, consumer protection, and systemic risk. Against this backdrop, the Bank of Canada has taken a decisive step.

In preparation for a comprehensive regulatory framework expected in 2026, the central bank has outlined what it considers acceptable stablecoins for circulation in Canada. The message, delivered publicly by Governor Tiff Macklem, is unambiguous: if stablecoins are to function like money, they must be designed and governed like money.

This clarification is not merely domestic policy. It reflects a broader global convergence toward stricter standards—one that will shape which digital assets survive, scale, and integrate into mainstream finance.

1. Stablecoins Must Behave Like Trusted Money

Speaking at the Montreal Chamber of Commerce, Governor Macklem emphasized a simple but powerful principle: stablecoins should function like reliable currency.

1.1 The Non-Negotiable 1:1 Peg

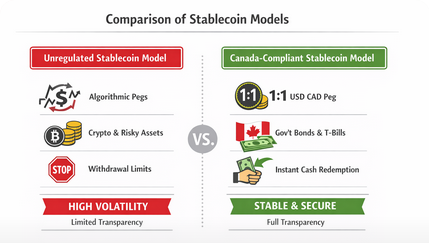

Under the proposed approach, any stablecoin permitted for use in Canada must be pegged one-to-one with a central bank currency (such as the Canadian dollar) or another major fiat currency. Algorithmic stabilization mechanisms, multi-asset pegs, or discretionary reserve management models are implicitly discouraged.

The rationale is straightforward. A unit of stablecoin must always be worth exactly $1, not approximately $1, and not $1 under “normal conditions.”

1.2 High-Quality, Liquid Reserve Assets Only

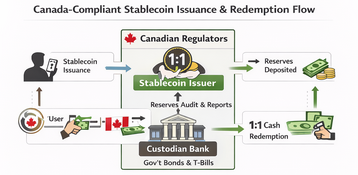

Equally critical is the nature of reserve backing. The Bank of Canada made clear that reserves must consist of high-quality, highly liquid government assets, such as:

- Short-term government bonds

- Treasury bills

- Central-bank-eligible sovereign instruments

Risky investments, leveraged strategies, or opaque structured products are unlikely to qualify. Reserves must be easily and rapidly convertible into cash, even during periods of market stress.

Implication: Stablecoin issuers will increasingly resemble narrow banks or money-market fund operators, with limited freedom to seek yield through risk.

2. Guaranteed Redemption at Par Value

Another cornerstone of the framework is unconditional redemption. Holders must be able to redeem stablecoins at face value, in cash, at any time.

2.1 Transparency Around Redemption Terms

Issuers will be required to clearly disclose:

- Redemption timing

- Fees (if any)

- Conversion processes

- Conditions under which redemption may be delayed

Without such transparency, Macklem warned, stablecoins cannot achieve trust comparable to cash or bank deposits.

2.2 Lessons from Past Crypto Failures

The central bank’s caution is informed by recent crypto-market collapses, where redemptions were halted or restricted precisely when users needed liquidity most. In those cases, lack of clarity and weak reserve management translated directly into consumer losses.

3. Consumer Protection and Operational Resilience

Beyond reserves and redemption, the Bank of Canada stressed operational robustness as a regulatory priority.

3.1 Full Reserve Coverage at All Times

Issuers must maintain sufficient reserves to cover all outstanding stablecoins, without exception. Partial backing models or reliance on future inflows will not be acceptable.

3.2 Resilience Under Market Stress

Stablecoin systems must continue functioning during:

- Market volatility

- Liquidity shocks

- Cybersecurity incidents

- Operational outages

This includes strong risk-management frameworks, internal controls, and safeguards for personal and financial data.

From a policy perspective, stablecoins are no longer viewed as experimental software—they are treated as critical payment infrastructure.

4. The Road to 2026: Canada’s Regulatory Architecture

The Bank of Canada is coordinating closely with the federal Department of Finance to integrate stablecoin oversight into existing legislation.

4.1 Integration with the Retail Payment Activities Act

The proposed framework will likely be embedded within Canada’s Retail Payment Activities Act, bringing stablecoin issuers and related payment service providers under formal supervisory oversight.

This marks a shift from the past, where many issuers operated outside traditional prudential regulation.

4.2 Budgetary and Legislative Signals

Canada’s federal government has already allocated funding in its 2025 budget to support stablecoin regulation. This signals political alignment and reduces uncertainty about whether the framework will be implemented.

5. Stablecoins as Part of Financial System Modernization

Importantly, the central bank framed stablecoin regulation not as a rejection of innovation, but as part of financial modernization.

Canada is simultaneously advancing:

- Real-time payment infrastructure

- Open banking frameworks

- Digital financial competition

Within this context, well-designed stablecoins could enhance efficiency, interoperability, and competition—provided they meet strict safety standards.

6. Global Context: Canada Is Not Alone

Canada’s position mirrors developments in other major jurisdictions:

- The European Union’s MiCA framework emphasizes full backing and redemption rights.

- U.S. policymakers increasingly favor reserve-segregation and narrow-bank-like models.

- Asian financial hubs are licensing stablecoin issuers under payment-service regimes.

For globally minded crypto entrepreneurs and investors, this convergence reduces regulatory arbitrage but increases clarity.

7. What This Means for Investors and Builders

For readers seeking new crypto assets, revenue opportunities, or practical blockchain applications, the implications are significant:

- Speculative stablecoin designs face declining regulatory viability.

- Compliance-first issuers gain strategic advantage.

- Stablecoins increasingly compete with bank deposits and money-market instruments, not volatile crypto tokens.

For blockchain builders, the opportunity shifts toward infrastructure, compliance tooling, cross-border settlement, and enterprise-grade payment solutions.

Conclusion: Innovation Within Clear Boundaries

The Bank of Canada’s message is neither anti-crypto nor laissez-faire. It reflects a mature regulatory philosophy: innovation is welcome, but only within structures that preserve trust and stability.

By insisting on 1:1 backing, high-quality reserves, guaranteed redemption, and operational resilience, Canada is signaling what the next generation of “acceptable” digital money will look like. For stablecoins, the era of creative ambiguity is ending. The era of disciplined, infrastructure-grade design has begun.

For those building and investing in the future of blockchain-based finance, this clarity—though demanding—may be the most valuable asset of all.