Main Points :

- The U.S. Senate has been working on a digital asset market structure bill since July, but progress has slowed.

- Political gridlock, a prolonged government shutdown, and partisan divisions are delaying legislative momentum.

- Debate over stablecoin yield provisions has intensified, with banking lobby concerns playing a central role.

- The upcoming U.S. midterm elections may significantly reduce the window for meaningful legislative action.

- Despite stalled progress, institutional crypto adoption and global regulatory competition are reshaping urgency.

- For crypto investors and builders, regulatory clarity could unlock new capital flows and business models.

1. Legislative Momentum Meets Political Reality

Since last summer, U.S. lawmakers have attempted to move forward with comprehensive digital asset market structure legislation. After the House of Representatives passed the CLARITY Act and forwarded it to the Senate, expectations were high that a bipartisan framework clarifying the roles of the SEC and CFTC would soon follow.

However, Washington’s political environment has proven inhospitable to rapid progress.

The Senate Agriculture Committee advanced a commodities-focused version of the bill roughly eight months before the midterm elections. Yet the Senate Banking Committee has not meaningfully progressed on securities law reform. A scheduled markup session in January was canceled, and no revised draft addressing securities oversight has emerged.

Rebecca Liao, co-founder and CEO of Web3 and AI protocol Saga and a former advisor to President Joe Biden’s 2020 campaign, recently described the bill as effectively “stalled.” Earlier optimism that the bill could pass by April has faded.

In previous bull cycles—when crypto markets were surging, traditional financial institutions were announcing digital asset strategies, and capital was flowing into Bitcoin and Ethereum—there was significant urgency for regulatory clarity. Agencies such as the SEC and CFTC were under pressure to define boundaries and provide compliance pathways.

Today, the atmosphere is different. The crypto market has cooled. Investor sentiment is more cautious. Even industry insiders question whether political alignment with crypto interests has delivered the regulatory breakthroughs many expected.

Passing any legislation in a divided Congress is difficult. Passing complex financial reform in an election year is exponentially harder.

2. Stablecoin Yield Debate: The Flashpoint Issue

One of the most contentious elements complicating Senate negotiations is the issue of stablecoin yield.

Reports indicate that senior officials within the Trump administration and representatives from the crypto and banking industries have met multiple times at the White House to discuss whether stablecoin holders should be permitted to receive yield through third-party platforms.

Banks argue that allowing yield-bearing stablecoins within a market structure framework could undermine traditional deposit models. If consumers can hold digital dollars earning competitive yields without relying on commercial banks, capital could migrate away from regulated banking institutions.

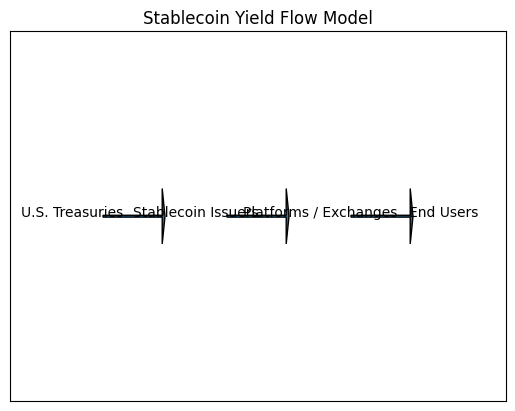

From a crypto-native perspective, yield-bearing stablecoins are a natural evolution of decentralized finance (DeFi). Stablecoins backed by Treasury securities already generate underlying returns. The question is who captures that value: issuers, platforms, or end users?

This debate reflects a broader structural tension between traditional finance (TradFi) and blockchain-based financial infrastructure.

Cody Carbone, CEO of crypto advocacy group The Digital Chamber, noted that while some participants at the World Liberty Financial Forum—including Coinbase CEO Brian Armstrong—remain optimistic about finding compromise solutions, there is little concrete clarity beyond aspirational timelines.

The political optics of stablecoin yield are significant. In an election year, lawmakers must balance financial innovation against systemic risk concerns and banking sector stability.

3. The Midterm Clock Is Ticking

The U.S. midterm elections are approaching rapidly. Primary elections are already underway in several states, including Arkansas, North Carolina, and Texas. The Senate is also expected to recess in August for approximately one month, returning only two months before the general election.

Legislative calendars shrink dramatically during election cycles. Floor time becomes scarce. Lawmakers prioritize campaign messaging and constituent engagement over complex bipartisan negotiations.

Even if a draft were finalized soon, shepherding a comprehensive crypto market structure bill through committee, floor debate, reconciliation, and final passage within such a compressed window would be ambitious.

History suggests that major financial reform typically requires sustained bipartisan momentum and economic urgency. In the current environment, both appear muted.

4. Why Market Structure Still Matters for Crypto Investors

Despite political stagnation, the strategic importance of U.S. market structure reform cannot be overstated.

A clear delineation between commodities and securities would:

- Reduce enforcement-driven uncertainty.

- Lower compliance costs for exchanges and token issuers.

- Encourage institutional capital allocation.

- Enable new product innovation, including tokenized securities and regulated DeFi protocols.

For investors seeking the “next revenue source” in crypto, regulatory clarity often precedes capital inflows.

Consider how Bitcoin ETF approvals unlocked billions of dollars in institutional capital. A comprehensive market structure framework could have a similar multiplier effect across altcoins, tokenized real-world assets (RWAs), and on-chain financial primitives.

5. Global Competition: The U.S. Is Not Alone

While Washington debates, other jurisdictions are moving decisively.

The European Union’s Markets in Crypto-Assets (MiCA) regulation has already established a unified framework across member states. Hong Kong has advanced licensing regimes. Singapore continues to refine its digital asset oversight. The United Arab Emirates is positioning itself as a global crypto hub.

Capital is mobile. Founders are mobile. Developers are mobile.

If U.S. regulatory clarity remains delayed, projects may increasingly incorporate offshore, pursue token issuance outside U.S. jurisdiction, or focus on non-U.S. markets first.

For readers interested in practical blockchain use cases, this global dynamic matters. Stablecoin payments, tokenized treasuries, decentralized identity, and cross-border remittances are scaling fastest in jurisdictions offering predictable regulatory environments.

6. Stablecoins, Treasury Yields, and the New Digital Dollar Economy

At the heart of the current debate is a profound structural shift: stablecoins are becoming digital wrappers around U.S. Treasury markets.

Major stablecoin issuers hold significant quantities of short-term Treasury securities. At $5% yields, these instruments generate substantial revenue streams. If yield were shared with holders, stablecoins could compete directly with money market funds and bank savings accounts.

This creates a new paradigm:

- On-chain dollar liquidity.

- Programmable yield.

- Instant global settlement.

- Reduced intermediary layers.

For crypto entrepreneurs, this represents a massive opportunity. Tokenized Treasury products, yield-bearing payment rails, and blockchain-native cash management systems could redefine how small businesses and global freelancers manage capital.

The policy decision around stablecoin yield will shape the competitive landscape of digital finance for the next decade.

7. The Political Paradox: Low Urgency, High Stakes

Rebecca Liao’s observation about reduced urgency captures the paradox of the moment.

In bull markets, volatility creates pressure for regulation. In bear markets, political urgency dissipates.

Yet structurally, the stakes are higher than ever:

- Institutional adoption continues incrementally.

- Asset tokenization is accelerating.

- AI and blockchain convergence is emerging.

- Digital asset payment infrastructure is expanding globally.

Legislation often lags innovation. But eventually, frameworks must align with economic reality.

Timeline of U.S. Crypto Market Structure Efforts vs. Midterm Election Calendar

Stablecoin Yield Flow Model (Treasuries → Issuers → Platforms → Users)

8. What Happens Next?

Several scenarios are possible:

- Accelerated Compromise: Lawmakers reach a limited agreement focusing on jurisdictional clarity while postponing stablecoin yield debates.

- Partial Legislation: Commodities-focused elements pass, leaving securities classification unresolved.

- Post-Election Reset: Comprehensive reform delayed until after midterms.

- Executive Action Expansion: Agencies increase enforcement and rulemaking in absence of Congressional clarity.

For investors and builders, preparation is key. Regulatory optionality—structuring projects to adapt to multiple jurisdictions—may prove essential.

Conclusion: A Window Narrowing, But Not Closing

The question of whether U.S. lawmakers can pass a crypto market structure bill before the midterm elections remains uncertain.

Political headwinds are real. Legislative calendars are tightening. Stablecoin yield debates expose deeper systemic tensions between traditional banking and decentralized finance.

Yet the long-term trajectory of digital assets continues upward.

For readers seeking new crypto assets, revenue models, and practical blockchain applications, regulatory clarity is not merely a political issue—it is a capital allocation catalyst.

Even if the bill stalls this year, the structural forces driving digital asset integration into global finance remain powerful.

Markets move in cycles. Policy often follows.

The midterms may delay reform, but they are unlikely to define the ultimate direction of blockchain’s integration into the global financial system.