Main Points :

- Strategy claims it can fully cover its debt even if Bitcoin falls to $8,000.

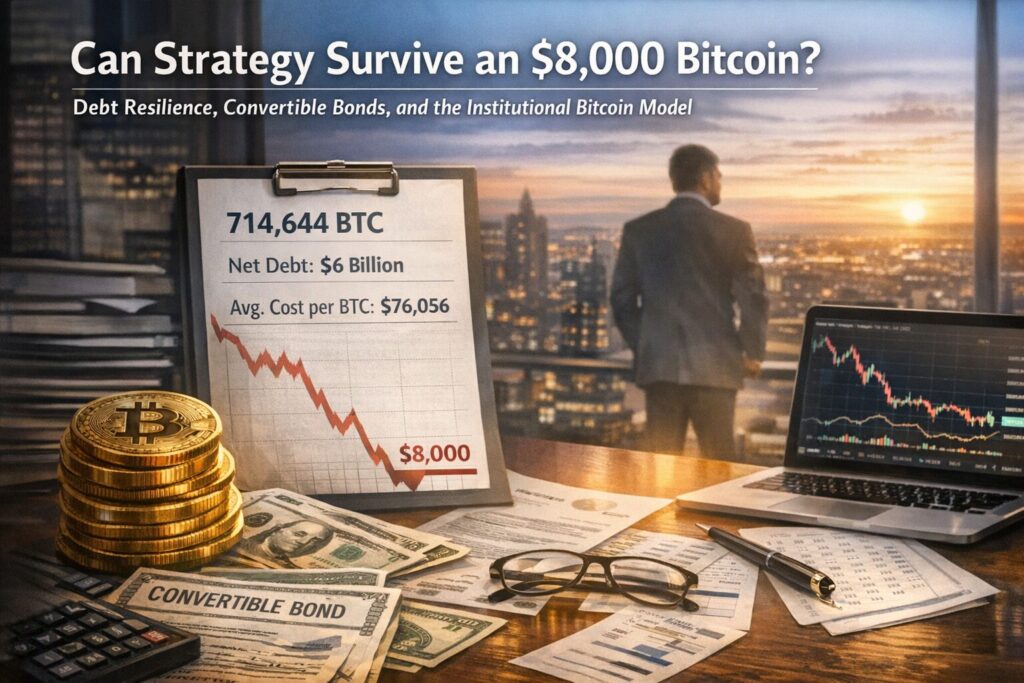

- The company holds 714,644 BTC, worth approximately $49.5 billion at current prices.

- Net debt stands at roughly $6 billion.

- Average acquisition cost per BTC is about $76,056.

- Management plans to convert convertible bonds into equity within 3–6 years.

- The model represents a new institutional Bitcoin treasury strategy.

- Extreme downside modeling may reshape corporate crypto risk frameworks.

1. Strategy’s $8,000 Bitcoin Stress Test

Strategy, widely known as the largest publicly traded corporate holder of Bitcoin, recently stated that even if Bitcoin were to collapse to $8,000, the company would still be able to fully cover its debt obligations.

At current levels near $70,000 per BTC, the firm holds 714,644 BTC, equivalent to roughly $49.5 billion in digital assets. Its net debt stands at approximately $6 billion. If Bitcoin were to fall to $8,000 — an 88% decline from present levels — the company’s Bitcoin holdings would be valued at around $5.7 billion. While that would represent a dramatic markdown relative to its total acquisition cost of approximately $54.3 billion, management argues that asset coverage would still be sufficient relative to net debt exposure.

This announcement arrives during a period of renewed volatility in the crypto market. Investors have become increasingly sensitive to leverage structures, particularly after multiple high-profile collapses in prior cycles. Strategy’s declaration appears designed to reassure shareholders and bondholders that its balance sheet remains structurally resilient even under extreme downside scenarios.

Unlike speculative overleveraged entities of past cycles, Strategy emphasizes long-dated debt maturities and structured financing rather than short-term margin-based leverage. This distinction is critical.

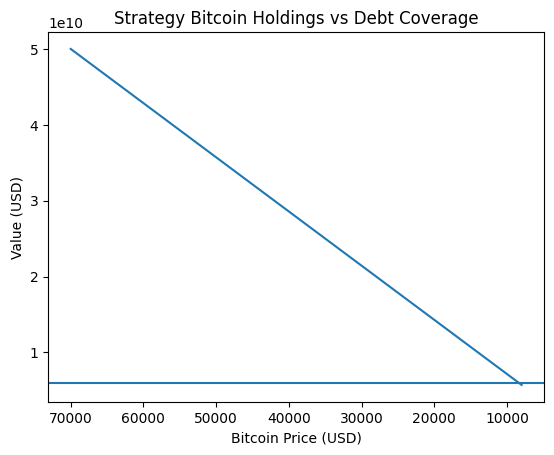

[“Strategy Bitcoin Holdings vs Debt Coverage at Various BTC Price Levels”]

Graph description:

- X-axis: Bitcoin price ($70,000 → $8,000)

- Y-axis: Asset value vs Net debt

- Line 1: BTC holdings value

- Line 2: Net debt level ($6B flat line)

This graph visually demonstrates the crossover point where asset value approaches net debt.

2. The Numbers Behind the Model

Strategy accumulated its Bitcoin at an average price of approximately $76,056 per BTC. This means that at $70,000, the company is slightly underwater on an unrealized basis. However, the core of its thesis is not mark-to-market accounting but long-term capital appreciation.

Its total acquisition cost stands at roughly $54.3 billion.

To understand the resilience model, it is important to distinguish between:

- Market value volatility

- Accounting impairment

- Debt maturity timing

- Liquidity runway

Even if Bitcoin temporarily trades below acquisition cost, debt coverage depends not on book losses but on the ability to service obligations and manage maturities. Strategy’s net debt of $6 billion is small relative to total asset exposure.

The firm has repeatedly structured debt with long maturities, reducing near-term refinancing pressure. This strategy differentiates it from short-term leveraged players in prior cycles.

3. Convertible Bonds as Strategic Leverage

Michael Saylor, co-founder and executive chairman, clarified that the company intends to convert convertible bonds into equity within the next 3–6 years.

This is a critical structural element.

Convertible bonds allow the company to:

- Raise capital at relatively low interest rates.

- Use proceeds to accumulate Bitcoin.

- Offer bondholders upside participation via equity conversion.

- Potentially reduce cash repayment burden if bonds convert.

If bondholders convert to equity instead of demanding cash redemption, net debt decreases without asset liquidation. Essentially, Strategy shifts risk from debt to equity dilution.

This is a calculated bet: if Bitcoin appreciates significantly over the next cycle, equity value rises, encouraging bond conversion.

The plan suggests high conviction in Bitcoin’s long-term appreciation trajectory.

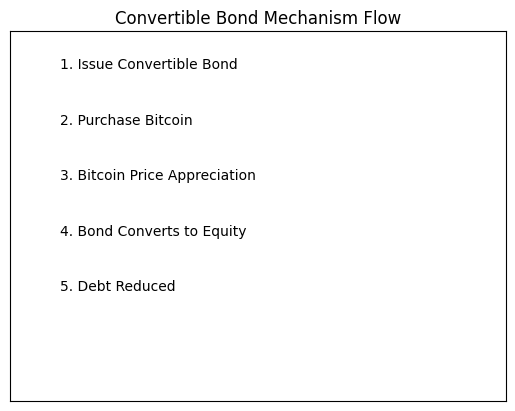

[“Convertible Bond Mechanism Flow”]

Diagram elements:

- Issue convertible bond

- Buy Bitcoin

- BTC appreciates

- Bond converts to equity

- Debt reduced

This diagram clarifies how financial engineering supports Bitcoin accumulation.

4. Institutional Bitcoin Treasury Model

Strategy represents a new corporate treasury model:

- Replace idle fiat reserves with Bitcoin.

- Finance accumulation via structured debt.

- Hedge dilution risk via long-term appreciation thesis.

Since Strategy’s initial Bitcoin purchase in 2020, numerous companies have considered similar treasury strategies, though few have matched its scale.

Institutional participation has expanded further with the launch of spot Bitcoin ETFs in the U.S., which have attracted billions in inflows. While retail participation has been uneven, institutional flows suggest accumulation phases continue beneath surface volatility.

In broader macro context, rising sovereign debt, currency debasement concerns, and structural inflation pressures reinforce Bitcoin’s positioning as a non-sovereign store of value.

5. Risk Factors: What Happens in an 88% Drawdown?

An 88% drawdown would resemble the most severe crypto bear markets historically.

At $8,000 BTC:

- Holdings ≈ $5.7B

- Net debt ≈ $6B

This implies asset coverage tightness, but management indicates additional liquidity and structured financing buffers exist.

However, risks remain:

- Equity dilution from convertible bond conversion.

- Potential credit downgrades if asset value collapses.

- Share price volatility amplifying capital cost.

- Regulatory shifts impacting accounting treatment.

Investors must recognize that while asset coverage may technically suffice, shareholder equity would experience extreme stress in such a scenario.

6. Broader Market Implications

Strategy’s stress modeling may influence how:

- Public companies evaluate crypto treasury allocations.

- Institutional lenders price crypto-backed risk.

- Regulators assess systemic exposure.

- Investors price equity proxies for Bitcoin exposure.

The key takeaway is not that Bitcoin will fall to $8,000, but that institutional players are designing frameworks to survive tail-risk scenarios.

This shift signals maturation of crypto-financial integration.

7. Lessons for Crypto Investors Seeking Opportunity

For readers searching for:

- New crypto assets

- Yield strategies

- Blockchain practical adoption models

Strategy’s model teaches several lessons:

- Long-term conviction requires structured financing discipline.

- Volatility modeling is essential for survival.

- Convertible instruments can be powerful strategic tools.

- Institutional adoption depends on risk architecture, not hype.

Investors may examine emerging companies adopting Bitcoin treasury strategies, DeFi protocols offering structured yield products, or tokenized debt instruments that mimic convertible models on-chain.

Additionally, infrastructure plays — custody solutions, treasury management software, on-chain accounting systems — may see increased demand as corporations explore digital asset balance sheets.

8. Is This Sustainable?

The sustainability of Strategy’s approach depends on:

- Bitcoin’s long-term appreciation.

- Continued access to capital markets.

- Investor appetite for equity dilution.

- Regulatory clarity.

If Bitcoin enters a multi-year structural bull market, the strategy could generate enormous equity upside.

If Bitcoin stagnates or declines for extended periods, dilution risk and debt pressure increase.

The plan to convert bonds within 3–6 years suggests management anticipates the next major cycle to unfold within that window.

Conclusion: Institutional Conviction Meets Financial Engineering

Strategy’s declaration that it can withstand an $8,000 Bitcoin scenario represents more than a bold headline.

It is a statement about institutional risk design.

The company has constructed a balance sheet architecture that blends:

- High-conviction asset accumulation

- Structured long-dated debt

- Convertible equity instruments

- Downside stress modeling

Whether one agrees with the strategy or not, it represents one of the most ambitious experiments in corporate Bitcoin adoption.

For investors seeking new crypto opportunities, the real signal is not the $8,000 number — it is the emergence of sophisticated treasury models designed to integrate Bitcoin into traditional corporate finance.

The next phase of crypto growth may not be driven solely by retail speculation, but by engineered institutional conviction.