Main Points:

- Market dominance of USD‑pegged stablecoins (USDT, USDC) and their liquidity advantages

- Structural obstacles for EUR‑pegged and other fiat‑pegged stablecoins

- Regulatory clarity (e.g., Europe’s MiCA): catalyst or insufficient alone?

- Proposed liquidity solutions: cross‑peg liquidity pools, refined AMM algorithms

- Incentive alignment: reshaping liquidity‑provider economics

- Future use cases: cross‑border remittances, on‑chain FX, multi‑currency corporate treasury

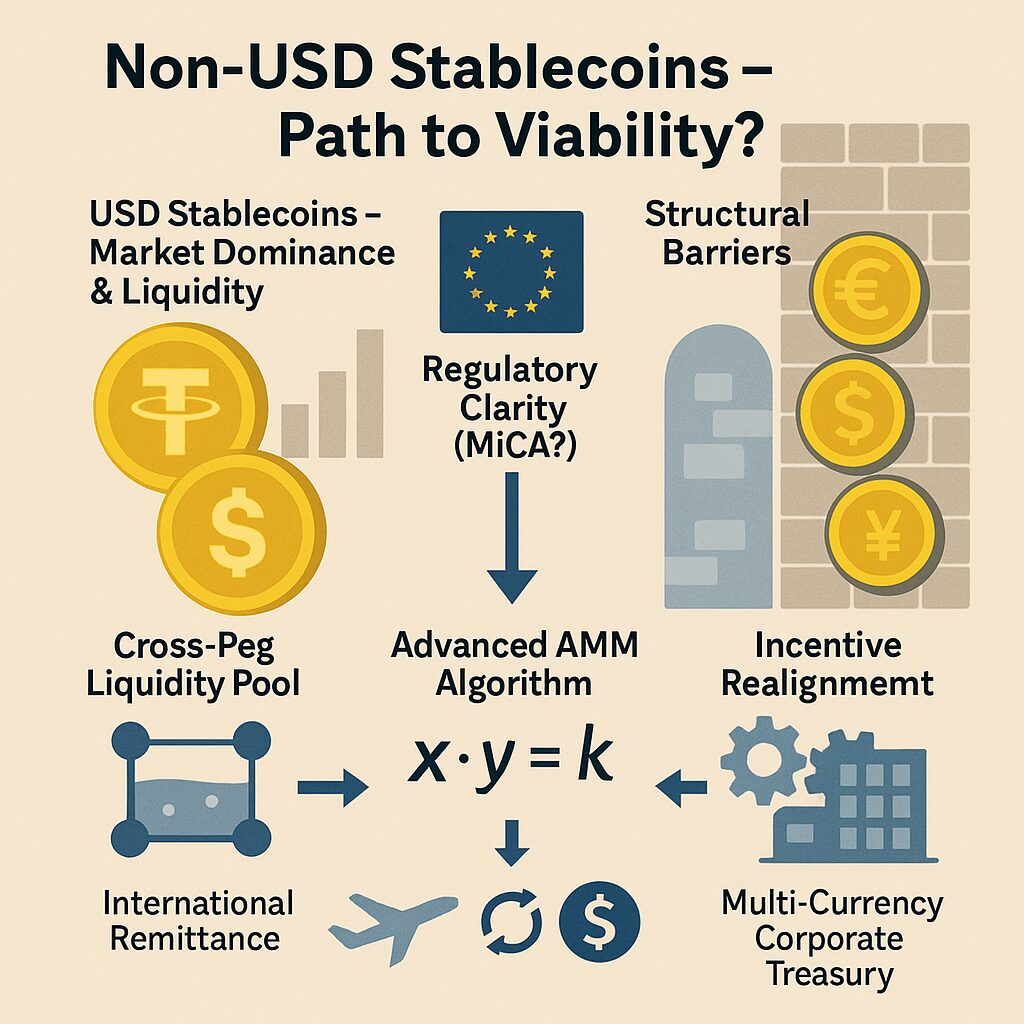

Market Leadership: The USD‑Pegged Hegemony

Stablecoins currently bridge crypto and TradFi: as of May 2025, total market cap exceeds $240 billion, reflecting broad trust in their utility. USDT and USDC alone account for roughly 90% of that market, with market caps of $149 billion and $62 billion, respectively (CoinGecko, May 2025). By contrast, EUR‑pegged coins like EURC and EURS each linger at around $200 million—less than 0.1% of the overall stablecoin market. Deep liquidity, trading volume, and CeFi/DeFi integrations undergird this USD‑peg dominance.

The Liquidity Challenge for Non‑USD Coins

Liquidity is the ultimate arbiter of adoption. EUR‑pegged stablecoins have existed for years but lack the trading pairs, on‑ramps, and AMM pools that make USD‑pegged coins “sticky” in both centralized exchanges and DeFi protocols. Market‑making firms allocate capital where returns are highest; with insufficient volume and fees in EUR pairs, there is little economic incentive to supply liquidity. This is not a matter of preference but of straightforward risk‑return calculus.

Regulation: Necessary but Not Sufficient

There is optimism that clear frameworks—such as the EU’s MiCA (Markets in Crypto‑Assets) regulation—will spur EUR‑pegged adoption by mandating transparency, reserve audits, and consumer protections. MiCA‑compliant coins like EURC could gain institutional trust, and TradFi on‑ramps in Europe may begin to support them more robustly. Yet, regulation alone cannot manufacture liquidity where market demand and profitability are lacking. Pre‑MiCA EUR coins languished; whether MiCA will meaningfully shift market‑maker behavior remains uncertain.

Emerging Non‑USD Examples

Notable non‑USD stablecoins have launched recently:

- XSGD (Singapore Dollar) on Ethereum, backed 1:1 and approved by the Monetary Authority of Singapore in late 2024

- XCHF (Swiss Franc) by Sygnum, with on‑chain reserves audited monthly

- HKDS (Hong Kong Dollar) issued December 2024 under Hong Kong’s regulatory sandbox

These nascent projects demonstrate regulatory leadership, yet their on‑chain liquidity remains orders of magnitude below USD counterparts.

Designing Liquidity Solutions

To bridge the gap, new mechanisms are required:

- Cross‑Peg Liquidity Pools: Establish AMM pools pairing USD‑pegged and non‑USD‑pegged coins (e.g., USDC/EURC pools) to allow direct swaps and facilitate arbitrage.

- Dynamic Fee Structures: Incentivize LPs through variable fees that increase during periods of high volatility or low depth.

- Synthetic Aggregators: Use derivatives and composability to route trades via synthetic USD exposures, thus deepening non‑USD pools indirectly.

Refining AMM algorithms—optimizing slippage curves and incorporating oracle‑based dynamic reserves—can attract LPs by offering better risk‑adjusted returns.

Aligning Economic Incentives

Ultimately, liquidity providers need sustainable yields. Protocols must offer a share of trading fees, emissions, or dedicated incentive programs for non‑USD pools. Governance tokens and ve‑model staking could allocate rewards specifically to EUR, SGD, or HKD pools. Partnerships with TradFi institutions—allowing them to stake real‑world assets or cash equivalents—could further deepen liquidity.

Potential Use Cases for Non‑USD Coins

While mass retail adoption may lag, specific niches could drive growth:

- Cross‑Border Remittances: SMEs in Europe or Asia sending EUR or SGD on‑chain to avoid FX fees.

- On‑Chain FX Trading: Decentralized exchanges offering native EUR/SGD pairs for arbitrage and hedging.

- Corporate Treasury: Multi‑national firms managing cash flows in multiple currencies on‑chain, borrowing non‑USD stablecoins to offset FX exposure.

In these contexts, non‑USD stablecoins deliver clear value, bypassing the need for USD on‑ramps and reducing currency conversion layers.

Conclusion

Although USD‑pegged stablecoins dominate due to unmatched liquidity, the door is open for non‑USD stablecoins to carve out niches—provided that liquidity provisioning is reengineered. Cross‑peg pools, dynamic AMMs, and targeted LP incentives can create sustainable depth. Regulation like MiCA may lend credibility, but only cohesive market design and aligned economics will enable widespread adoption. As global commerce demands multi‑currency on‑chain solutions, non‑USD stablecoins could emerge as vital infrastructure—ultimately fostering a more diversified and resilient digital‑asset ecosystem.