Main Points :

- Bitcoin has fallen more than 30% from its January highs, breaking below $63,000 and reaching its lowest level since November 2024.

- BTC options markets currently price less than a 6% probability of a rebound to $90,000 by late March.

- Deep out-of-the-money call options reflect fading short-term bullish conviction, while downside protection demand is rising.

- Corporate Bitcoin holders face valuation pressure, raising concerns about forced liquidations if bearish conditions persist.

- Macro risks—weakening U.S. employment data, aggressive AI capital expenditure, and broader risk-off sentiment—are weighing on crypto markets.

- For investors and builders, the current phase may be less about price recovery and more about positioning for the next structural cycle.

1. Bitcoin’s Sharp Decline: From Failed Breakout to Risk-Off Reality

Bitcoin (BTC) has entered a decisive correction phase. After failing to break above $90,500 on January 28, the asset has declined by nearly 30%, slipping below $63,000 on Thursday—its lowest level since November 2024.

This move has fundamentally altered short-term market psychology. Just weeks ago, many traders were positioning for a continuation of the post-ETF rally narrative. Today, optimism has been replaced by caution, as macroeconomic uncertainty and cross-asset weakness dominate sentiment.

While crypto-specific catalysts often drive volatility, this decline is occurring in tandem with broader risk assets, suggesting that Bitcoin is once again behaving as part of the global risk complex rather than as an isolated hedge.

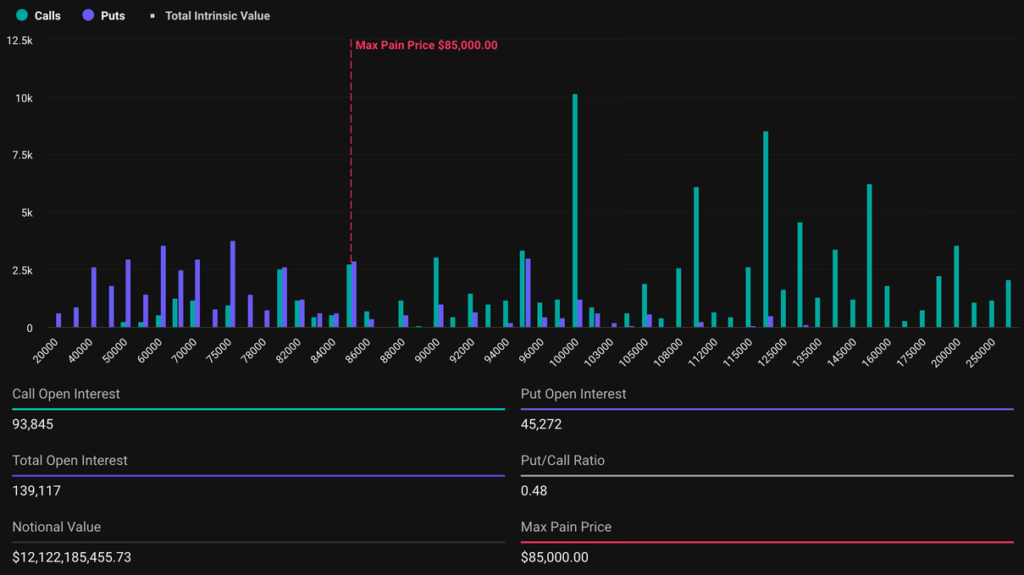

2. What the BTC Options Market Is Signaling About a $90,000 Rebound

(BTC March options implied probability and strike distribution)

The most revealing insight into market expectations comes from the derivatives market—specifically, Bitcoin options traded on Deribit.

As of Thursday, a Bitcoin call option with a $90,000 strike price expiring on March 27 was trading at approximately $522. According to the Black–Scholes pricing model, this implies less than a 6% probability that BTC reaches $90,000 by late March.

In contrast, put options granting the right to sell BTC at $50,000 on the same date were trading around $1,380, reflecting roughly a 20% implied probability of a deeper drawdown.

This asymmetry tells a clear story: traders are more concerned about downside protection than upside participation in the near term.

3. Why Probability Matters More Than Narratives Right Now

Options markets aggregate real money risk preferences. Unlike social sentiment or speculative commentary, option pricing reflects how much traders are willing to pay to insure or speculate on future outcomes.

The collapse in demand for high-strike calls suggests that—even among sophisticated participants—the probability-weighted case for a rapid recovery is weak. This does not mean Bitcoin cannot rebound; it means the market is not willing to pay for that possibility today.

For investors searching for new revenue opportunities, this environment favors volatility strategies, yield generation, and long-term accumulation, rather than directional short-term bets.

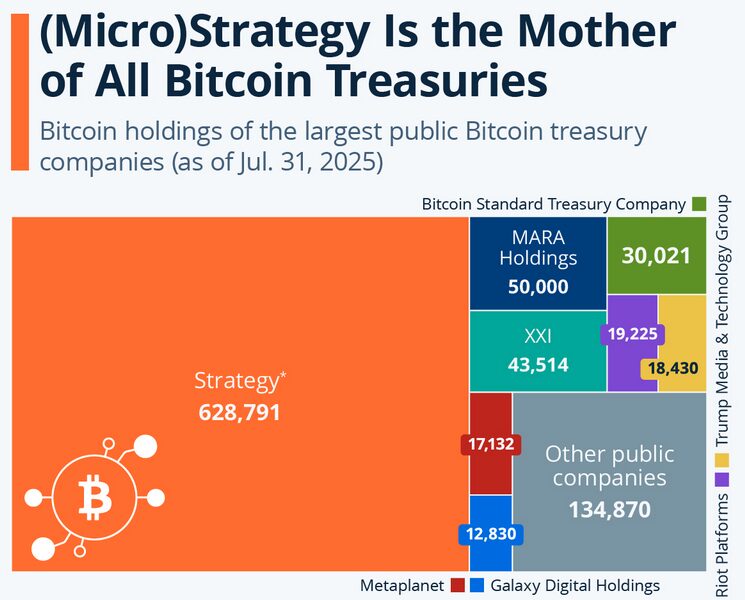

4. Corporate Bitcoin Holdings: A New Source of Systemic Risk

(Public companies’ BTC holdings vs acquisition cost)

One of the underappreciated risks in the current cycle lies in corporate Bitcoin treasuries.

The largest corporate holder, Strategy (MSTR), has seen its enterprise value decline to approximately $53.3 billion, while its Bitcoin acquisition cost remains near $54.2 billion.

Similarly, Japan-based MetaPlanet holds BTC acquired at roughly $3.78 billion, against a current valuation of about $2.95 billion.

If bearish conditions persist, investors fear that debt-servicing pressures or equity dilution could force these companies to liquidate portions of their BTC holdings—introducing additional sell-side pressure into the market.

5. Quantum Computing Fears and Long-Term Cryptographic Anxiety

Beyond price action, structural concerns are also influencing exposure decisions. In mid-January, prominent global strategists publicly cited quantum computing risks as a reason to reduce Bitcoin allocations.

The fear is not imminent key-breaking, but future cryptographic obsolescence, which introduces long-horizon uncertainty for long-duration holders. While this risk remains theoretical, it contributes to a broader reassessment of crypto exposure among institutional allocators.

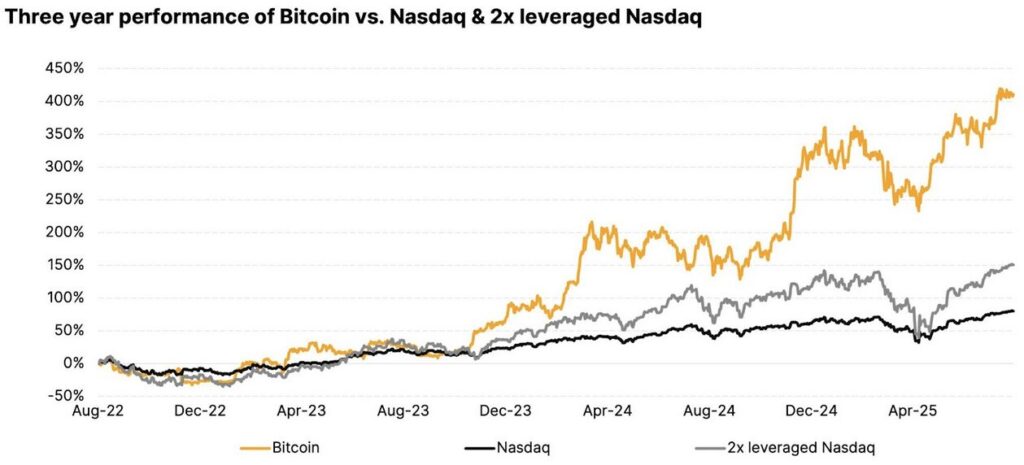

6. Macro Headwinds: Jobs, AI Spending, and the Cost of Capital

(BTC vs tech stocks and macro indicators)

Macro conditions have worsened materially. According to Challenger, Gray & Christmas, U.S. companies announced 108,435 layoffs in January, a 118% increase year-over-year, marking the worst January since 2009.

At the same time, corporate AI spending has triggered fresh concerns. Google recently projected capital expenditures of $180 billion in 2026, nearly double its 2025 spending of $91.5 billion.

Meanwhile, Qualcomm cut its growth outlook, citing memory supply constraints caused by data center demand, sending its stock down roughly 8%.

Investors increasingly fear that AI investment returns will be delayed by energy constraints, semiconductor bottlenecks, and intensifying competition—factors that weigh heavily on risk assets, including Bitcoin.

7. Cross-Asset Confirmation: Bitcoin Is Not Falling Alone

Bitcoin’s weekly decline of approximately 27% mirrors drawdowns seen in major publicly traded companies and even in commodities such as silver, which dropped 36% from its recent highs.

This cross-asset correlation reinforces the idea that the current Bitcoin sell-off is not purely crypto-driven, but part of a broader global deleveraging cycle.

8. What This Means for Investors, Builders, and Operators

For those seeking the next crypto asset, next yield opportunity, or practical blockchain applications, the message is nuanced:

- Short-term price recovery expectations should be tempered.

- Volatility, not direction, is currently the dominant tradable feature.

- Strong balance sheets and low leverage matter more than narratives.

- Infrastructure, payments, custody, compliance, and real-world settlement layers continue to attract capital even during bear phases.

Historically, periods of pessimism like this often precede structural innovation rather than speculative manias.

9. Conclusion: Probability Is Low—but Cycles Never End

The probability of Bitcoin reclaiming $90,000 by March is currently priced at around 6%, according to options markets. This reflects caution, not collapse.

Bitcoin remains a long-duration asset shaped by liquidity cycles, technological evolution, and institutional adoption. While the short-term outlook is constrained by macro forces, the longer-term trajectory will likely be defined by who builds, who survives, and who positions intelligently during drawdowns.

For serious participants, this is less a moment of despair—and more a moment of strategic preparation.