Main Points:

- Japan’s Financial Services Agency (FSA) has formally criticized crypto exchanges for steering users toward high-spread brokerage services (“sales offices”) rather than low-cost order-book exchanges.

- Regulatory authority is expected to shift from the Payment Services Act to the Financial Instruments and Exchange Act (FIEA), bringing stricter obligations: disclosures, insider-trading rules, best-execution rules, and reserve requirements.

- These new rules will significantly increase operational costs, placing smaller exchanges at risk of exit or consolidation.

- Investors must adapt by reducing spread losses, diversifying exchange risk, and monitoring regulatory changes closely.

- The changes could narrow available tokens in Japan but strengthen long-term consumer protection and institutional credibility.

1. Introduction: A Market Under Intensifying Scrutiny

Japan’s cryptocurrency ecosystem—once celebrated as one of the safest regulatory environments globally—is entering a period of profound transition. On November 25, 2025, the Financial Services Agency (FSA) released a draft report outlining concerns that crypto exchanges have been intentionally guiding users toward brokerage-style services (販売所) instead of market-based exchanges (取引所).

The critique centers around one fact: brokerage spreads are drastically higher and function as hidden fees, often burdening inexperienced users who choose simplified interfaces.

This report signals a major regulatory realignment—one that shifts crypto asset regulation from the Payment Services Act to the Financial Instruments and Exchange Act (FIEA), placing crypto assets under a framework similar to securities.

To understand the implications for exchanges, investors, and builders, this article synthesizes the FSA’s findings, analyzes industry shifts, compares global regulatory posture, and forecasts where Japan’s crypto landscape is heading.

2. Brokerage Steering and the Real Cost of Crypto Purchases

2.1 What the FSA Identified

The FSA’s Working Group on Crypto Asset Systems highlighted a growing industry practice:

Exchanges prominently display “simple buy/sell” screens (brokerage) while hiding order-book trading behind several layers of UI.

The agency notes this creates a misleading perception:

- Brokerage looks simpler

- “No fee” claims disguise wide spreads

- New users unknowingly pay multiple percentage points per trade

In effect, many beginners end up paying 5–10× more than necessary.

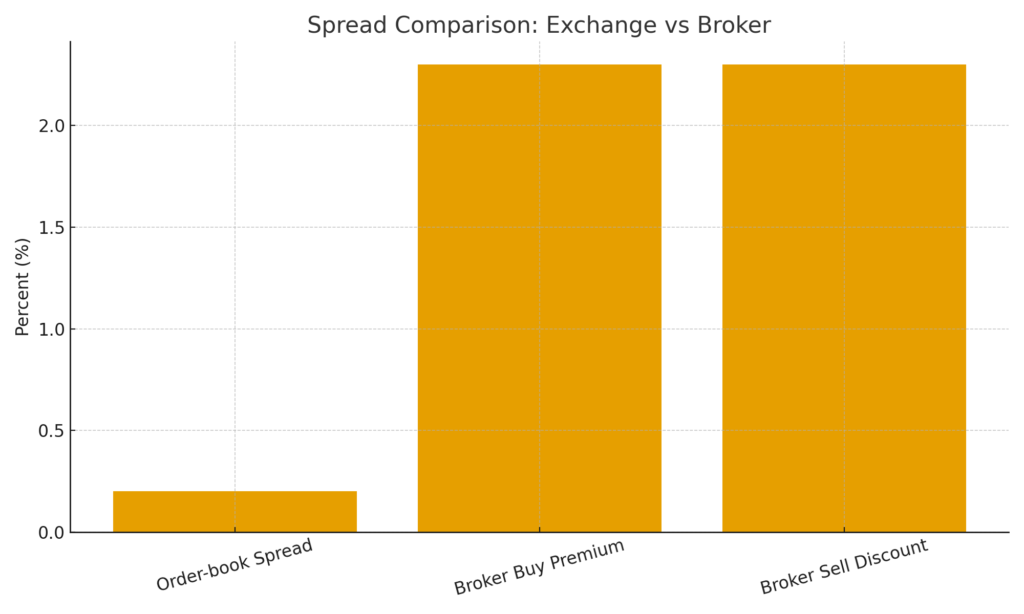

2.2 How Large Are These Spreads?

In Japan, brokerage spreads typically fall between 0.1% and 5%, but can exceed this during periods of volatility.

Below is a sample snapshot comparing spreads:

The chart shows:

- Exchange (order-book) typical spread: 0.01–0.2%

- Broker (buy price): +2.3%

- Broker (sell price): –2.3%

- Effective spread: ~4.6%

Thus, a user buying and immediately selling $1,000 of BTC at a brokerage could lose around $46 instantly.

This cost structure explains why brokers have strong financial incentives to route users to brokerage screens—and why regulators are alarmed.

3. Why Exchanges Push Brokerage: Understanding the Revenue Model

3.1 The Profit Engine Behind Brokerage

Brokerage revenue sources include:

- High spreads (hidden fees)

- Example: 3% spread on $1,000 buys → $30 revenue per trade

- Round-trip trading: $60 revenue

- Market-making profits

Exchanges hold inventory, adjusting prices to capture volatility spreads. - Complete pricing control

Brokerage allows exchanges to set prices rather than relying solely on open markets.

In contrast:

- Order-book exchanges rely primarily on 0–0.15% fees.

- Some even offer negative maker fees.

Therefore, order-books are less profitable unless volumes are extremely high.

3.2 How Users Are Steered

The FSA cited patterns across major exchanges:

- “Simple Buy” icons placed on the home screen

- Buy/sell buttons redirecting to brokerage by default

- Order-book access hidden in submenus

- Marketing messages like “zero fees!” that obscure spreads

Media investigations confirm that most beginners unknowingly use brokerage instead of exchanges—even though order-books are cheaper.

4. Japan’s Regulatory Shift to the Financial Instruments and Exchange Act (FIEA)

The FSA now plans to move crypto regulation under the FIEA, essentially treating crypto assets similarly to securities.

4.1 Key Regulatory Upgrades Under Consideration

(1) Mandatory Disclosure Requirements

For all professionally handled tokens:

- Token supply information

- Centralization risks

- Technical documentation

- Audits

- Governance and insider risks

This will force issuers and exchanges to meet standards similar to IPO disclosures.

(2) Insider Trading Rules

Crypto will be treated like stocks for insider rules:

- Large transactions (20%+ supply)

- Listing/delisting events

- Project failures or major changes

These must be disclosed through official channels, not social media.

(3) Best Execution Obligation

Under FIEA, brokers must prove they are executing trades at the best available price.

This directly challenges wide brokerage spreads.

(4) Suitability Requirements

Users may be restricted from buying certain high-risk assets based on:

- Income

- Experience

- Net worth

- Risk tolerance

(5) Full Market Surveillance

The FSA intends to implement:

- Anti-manipulation rules

- Enforcement of fair pricing

- Real-time monitoring infrastructure

This is likely to change how exchanges operate fundamentally.

5. Reserve Requirements: Protecting User Assets After Repeated Hacks

Japan plans mandatory reserve funds for all exchanges—covering both:

- Hot wallets

- Cold wallets (new requirement)

This follows several major global and domestic hacks:

| Incident | Loss |

|---|---|

| Bybit Hack (2025) | $1.5B |

| DMM Bitcoin Hack (2024) | $3.1B |

| Coincheck NEM Hack (2018) | $3.7B |

Because cold-wallet losses have historically been unprotected, the new rules will require exchanges to maintain tens or hundreds of millions in reserves—either in cash or insurance.

Small exchanges may be unable to survive this shift.

6. Impact on the Industry: A Possible Wave of Exchange Closures

6.1 Five Critical Impacts

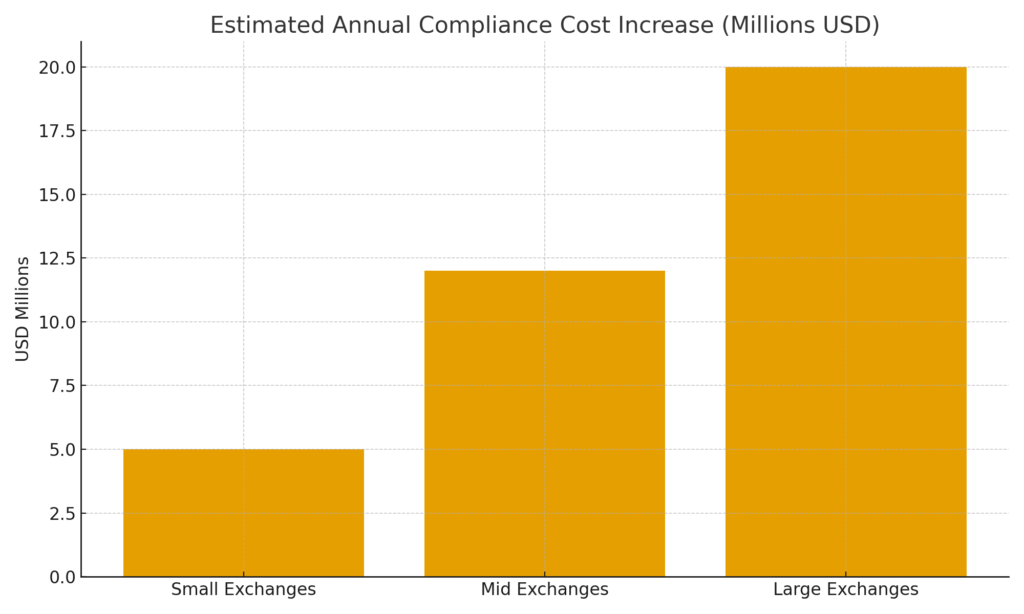

- Massive Compliance Cost Increase

Annual costs may increase by $5M–$20M, depending on exchange size. - Sharp Reduction in Supported Tokens

Only 105 major tokens may survive initial listing eligibility under FIEA standards. - Decline in Brokerage Profitability

Best-execution rules will restrict wide spreads. - Small Exchanges May Exit

Many may sell, shut down, or merge. - Competitive Loss to Overseas Exchanges

Over-regulation risks pushing users toward:

- Binance

- Bybit

- Coinbase International

- Global DEXs

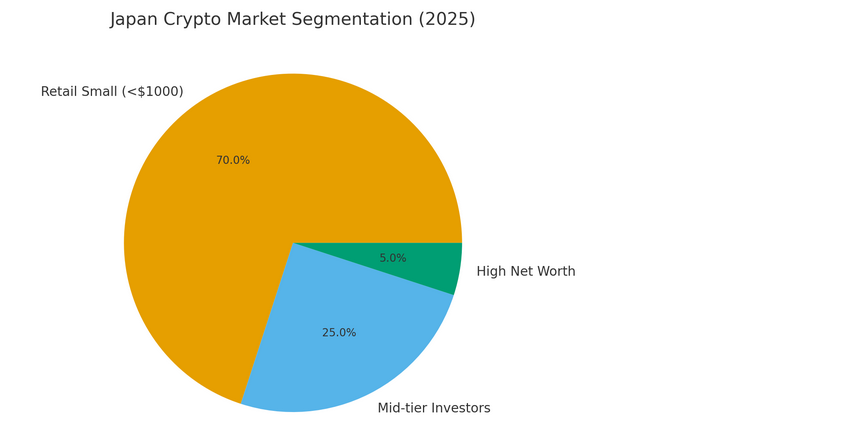

7. Japan’s Crypto Market Structure (as of January 2025)

Data submitted to the FSA indicates:

- 12.13 million accounts

- Customer assets exceeding $33B (approx ¥5T)

- 70% of holders earn under $47,000/year

- 86% buy crypto expecting long-term appreciation

A large majority are small retail investors—not high-risk day traders.

Below is an easy segmentation chart:

8. What Investors Should Do Now

8.1 Five Essential Actions

- Use order-book exchanges—not brokerage—to avoid spread losses.

- Open accounts on multiple exchanges.

- Self-custody long-term holdings.

- Monitor regulatory changes.

- Invest only what you can afford to lose.

8.2 Checklist for Selecting an Exchange

- Registered with FSA

- Offers order-book trading

- Transparent security practices

- Clear financials

- Reliable customer support

9. Conclusion: A More Mature but Narrower Market Ahead

Japan’s regulatory tightening will likely:

- Improve consumer protection

- Reduce fraudulent or low-quality tokens

- Increase institutional confidence

- Create high operational barriers for new exchanges

However, the market may also shrink as:

- Many tokens disappear from availability

- Smaller exchanges exit

- Brokerage models decline in profitability

For investors and builders, the era of “easy crypto trading in Japan” is ending.

A more mature, regulated, institutional-grade market is emerging—one that rewards informed investors and compliant operators.