Main Takeaways :

- Bitcoin has fallen more than 20% over the past month and over 30% from its all-time high above $120,000, while U.S. equities, powered by artificial-intelligence-related mega caps, have held up relatively well.

- A $20 billion wave of derivatives liquidations in October reset positioning across the crypto market and left traders cautious, with around $500 million in positions still being flushed out on a typical day.

- Bitcoin is still trading like a high-beta risk asset rather than a pure “digital gold,” even as physical gold repeatedly hits new record highs above $4,000 per ounce amid macro uncertainty.

- Long-term “whale” investors have taken profits above $100,000, while altcoins have dropped 50% or more, pushing the market into what some strategists call a “panda market”: not a full crypto winter, but clearly a bearish phase.

- For investors hunting the next revenue source or practical blockchain use case, the most promising niches are AI-related tokens, real-yield protocols, and infrastructure that ties blockchains to real-world activity—areas where fundamentals, not just hype, are starting to matter again.

From Euphoria to “Panda Market”: Where Bitcoin Stands Now

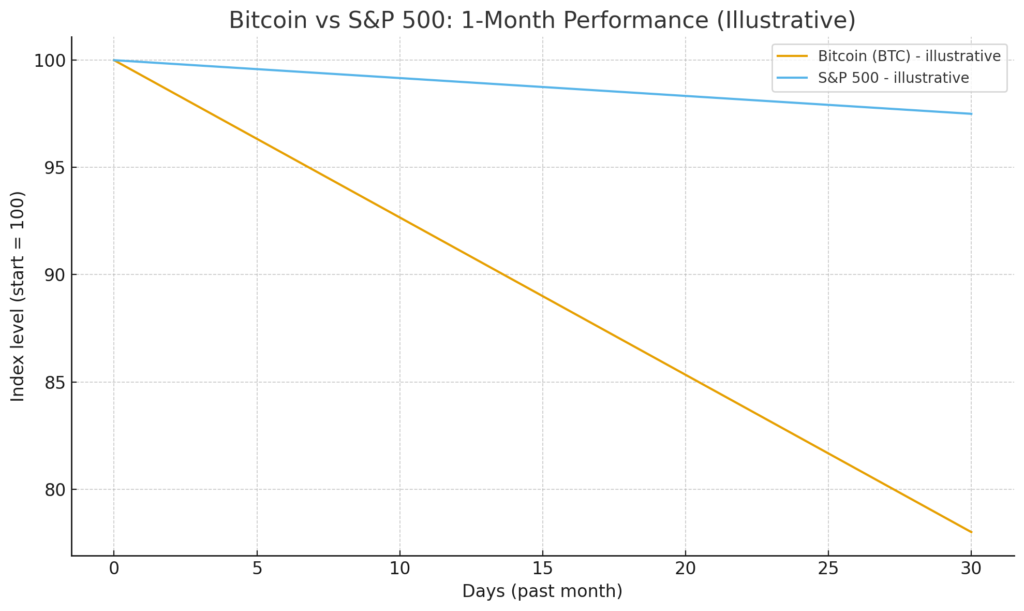

Over the last month, Bitcoin has given up a substantial part of its 2025 gains. From a peak around $126,000 in early October, the price slid below $82,000 by late November—a drop of roughly 35%. Measured over the last 30 days, Bitcoin is down a little more than 20%, while major U.S. stock indices are only mildly negative: the S&P 500 is off about 2.5% and the tech-heavy Nasdaq around 4%.

Technically, that decline has pushed BTC more than 30% below its highs and, crucially, below its 50-week moving average. Historically, losing that moving average has often signaled a broad change in market momentum from bullish to bearish. At the same time, many altcoins have fared far worse, falling 50% or more from their peaks as liquidity and risk appetite evaporated outside the very top of the market.

Some analysts describe this environment as a “panda market”: the cycle isn’t as brutal as the deep crypto winters seen after 2018 or 2022, but the bias has clearly shifted to the downside. Volumes are thinner, new capital flows are slower, and short-term sentiment is fragile—even though the long-term structural story for Bitcoin remains intact.

Figure 1 (the first chart image above) illustrates this relative underperformance. Starting from an index level of 100 one month ago, an illustrative path for Bitcoin drops to the high-70s, while the S&P 500 only drifts slightly lower. The exact numbers are simplified, but the direction matches what we see in actual markets: crypto has borne the brunt of the latest risk-off turn.

Why U.S. Equities Are Holding Up: The AI Trade

The key question is obvious: if macro conditions are challenging for all risk assets, why have U.S. stocks held up better than Bitcoin and altcoins?

The short answer is artificial intelligence.

Throughout 2025, the “Magnificent Seven” mega-cap tech stocks—companies like Nvidia, Microsoft, Alphabet, Amazon, Meta, Apple, and Tesla—have dominated U.S. equity performance. Stripping these names out of the S&P 500 leaves what some commentators call the “S&P 493,” which paints a much weaker picture of the underlying U.S. economy.

AI is the new “shiny object” on Wall Street. Corporate spending on data centers, GPUs, and AI infrastructure has exploded, and many investors treat AI-linked equities as the safest way to play long-run productivity gains. Even when the broader market wobbles, AI narratives continue to attract capital, helping to cushion any sell-offs.

This AI trade has a direct opportunity cost for crypto. Capital that might once have rotated into Bitcoin, Ethereum, or high-beta altcoins now finds its way into Nvidia shares or baskets of AI infrastructure plays. Funds with limited risk budgets often choose between “AI exposure” and “crypto exposure,” and in 2025, AI remains the stronger story for most traditional allocators.

Leverage, Liquidations, and the October Shock

Beyond relative narratives, the structure of the crypto market itself has amplified the recent downturn.

On October 10, the market suffered one of the most violent liquidation events in its short history. Triggered by a negative macro headline—new U.S. tariffs on Chinese software and tech imports—nearly $20 billion worth of leveraged crypto positions were wiped out across major exchanges in roughly 24 hours.

Estimates suggest around 1.6 million traders were liquidated, with over 1,000 losing more than $100,000 each and hundreds losing seven-figure sums. Open interest in derivatives collapsed back to levels last seen in mid-year, and liquidity in long-tail tokens temporarily vanished, leading to extreme, if brief, flash crashes.

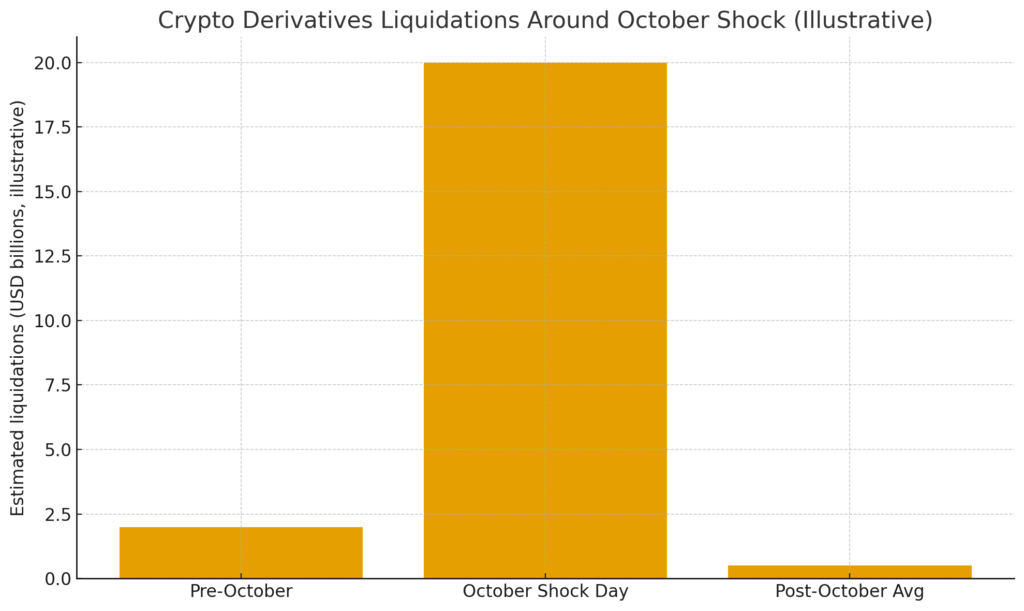

Figure 2 (the second chart image above) depicts an illustrative comparison: relatively modest average daily liquidations before October, a single spike near $20 billion on the shock day, and a much lower but still noticeable level afterward. Again, the bars are stylized, but they reflect the basic pattern seen in actual data providers’ reports.

Since that shock, the market has remained in what some analysts call a “hangover phase.” Even as spot prices try to stabilize, around $500 million of positions continue to be liquidated on a typical day as over-leveraged traders are forced out of their positions. The absence of major frauds or hacks during this drawdown suggests the core issue isn’t structural failure, but simple over-risk-taking: too much leverage on the way up, followed by a mechanical “de-risking” on the way down.

For builders and long-term investors, this matters: it implies the current downturn is largely technical and positioning-driven, not a fundamental rejection of the asset class.

Profit-Taking by Long-Term Whales

The October event also gave long-term Bitcoin holders an attractive chance to realize part of their gains.

On-chain data shows that wallets that have held BTC for many years—since the early 2010s in some cases—finally began to move coins when prices were above $100,000. At those levels, even a small sale can crystalize life-changing profits for early adopters.

From a market-structure perspective, this isn’t necessarily bearish. When a longtime whale sells to a newer holder who has done fundamental research and has a multi-year time horizon, supply becomes more distributed. However, in the short term, large sell orders from OG wallets can become self-fulfilling signals of “top-ish” conditions, especially when they coincide with elevated leverage and exuberant sentiment.

The combination of whale profit-taking, forced liquidations, and AI-driven capital rotation away from crypto helps explain why Bitcoin has underperformed even in the face of seemingly bullish catalysts such as growing regulatory clarity and the continued success of spot Bitcoin ETFs.

Bitcoin vs. Gold: Still Trading Like a Risk Asset

Another key piece of the puzzle is how Bitcoin behaves relative to gold.

In 2025, gold has repeatedly hit new record highs, briefly touching $4,000 per ounce in October and continuing to trade above $4,100 in late November. The drivers are familiar: geopolitical tension, expectations of Federal Reserve rate cuts, and concerns about equity and bond valuations.

Bitcoin, by contrast, has not yet been treated as a pure safe-haven asset. Although it has a capped supply and a predictable issuance schedule, its 24/7 trading and deep derivatives markets mean that it responds almost instantly to changes in risk appetite. When traders de-risk, BTC sells off alongside high-beta tech names.

The October liquidation shock highlighted this dynamic. While gold rallied on safe-haven flows, Bitcoin behaved more like a high-growth, high-volatility tech stock. That doesn’t invalidate the “digital gold” thesis in the long run, but it reminds investors that, for now, BTC is still primarily a risk-on macro asset.

For portfolio builders, this difference is critical. Gold may hedge geopolitical or monetary shocks; Bitcoin may amplify them. The right allocation depends on whether an investor wants convex upside with drawdown risk, or smoother defensive characteristics.

The Growing Importance of Fundamentals in Altcoins

If Bitcoin is in a “panda market,” altcoins are in something closer to a deep freeze.

Following the October crash and subsequent slide, many mid-cap tokens are down 50% or more from their highs, and liquidity in speculative micro-caps has dried up. In previous cycles, this kind of pain often preceded a new wave of meme tokens and narrative-driven rallies once the dust settled.

This time, however, there are signs the market is maturing. Investors increasingly differentiate between coins with real revenue, sustainable staking yields, or critical infrastructure roles—and those that are purely narrative-driven.

Real-yield protocols that share protocol fees or sequencer revenues with token holders are gaining traction. Infrastructure projects that connect blockchains to real-world data, payments, or compliance rails are also attracting attention, as they can tie token value to off-chain cash flows rather than pure speculation.

For readers seeking the “next income source,” this shift is important: staking APYs or emissions schedules are no longer enough. The market is asking: who pays, for what service, in which currency—and why can’t this be done without the token?

AI Tokens and the Blockchain–AI Intersection

Ironically, although AI has “stolen” some macro attention from crypto, the intersection of AI and blockchain is itself one of the most interesting areas in the market.

AI-related tokens—such as Bittensor (TAO), Fetch.ai (FET), Render (RNDR), SingularityNET (AGIX), and others—aim to decentralize either AI training, GPU compute markets, data marketplaces, or model access. Some provide marketplaces where GPU owners can rent out hardware in exchange for tokens, while others tokenize access to AI models or datasets.

After strong rallies earlier in the year, many of these tokens were also hit hard by the October sell-off. Nonetheless, they remain among the more resilient segments of the altcoin universe because they sit at the intersection of two powerful secular trends: AI and decentralized infrastructure. Recent research pieces highlight AI tokens as one of the most attractive narratives for the 2025–2026 altseason, particularly for investors who already understand the basics of crypto and want more specialized exposure.

For builders focused on practical blockchain applications, AI-blockchain hybrids also offer tangible use cases:

- Verification of AI-generated content: using blockchains to prove provenance and authenticity in a world flooded with deepfakes.

- Decentralized data markets: where data providers and labelers are paid in tokens and can prove the integrity of their contributions.

- Compute marketplaces: where idle GPUs are monetized securely via smart contracts.

These ideas are still early, and adoption is not yet mainstream. But unlike many purely speculative tokens, AI-aligned projects often have a clear business model: sell compute, data, or model access.

What Could Turn the Tide by 2026?

Despite the recent pain, many structural forces still support Bitcoin and high-quality crypto assets over a multi-year horizon.

First, regulatory clarity is slowly improving. Major jurisdictions have passed or are implementing crypto frameworks that define how exchanges, custodians, and stablecoin issuers should operate. That clarity reduces the tail risk of outright bans and makes it easier for institutions to allocate.

Second, the interest-rate backdrop is shifting. Markets increasingly expect the Federal Reserve to begin cutting rates in 2026 as inflation cools and growth slows. Lower real yields historically benefit assets like gold and Bitcoin that have no cash flows but offer scarcity and optionality.

Third, the ETF channel continues to matter. Spot Bitcoin ETFs in the U.S. have already absorbed substantial inflows this cycle. As volatility normalizes and performance stabilizes, wealth managers who missed the first wave may allocate fresh capital, particularly if clients ask for “digital gold” exposure in small, diversified doses.

For altcoins, the bar will be higher. Projects that cannot demonstrate real usage or revenue may never recover their previous valuations. But those that power core infrastructure—layer-2 rollups, cross-chain messaging, tokenized real-world assets, AI compute, compliance, and payments—could emerge from the panda market with stronger competitive positions and more disciplined tokenomics.

Where Are the Opportunities for the Next Income Source?

For readers specifically looking for the next income stream or practical blockchain implementation, three clusters deserve special attention:

- Real-Yield and Fee-Sharing Protocols

Look for protocols that share actual fees—DEX trading fees, L2 sequencer revenues, liquid-staking yields, or stablecoin interest—with token holders. The key is to distinguish between emissions (inflation) and real economic value. Sustainable yields tend to be single-digit or low double-digit in dollar terms; anything far above that likely hides hidden risk. - AI and Data-Infrastructure Tokens

As discussed, tokens such as FET, RNDR, AGIX, TAO, and similar projects are building decentralized GPU and data networks. The revenue model is often straightforward: users pay for compute or data in tokens; providers earn tokens for supplying resources. This is much closer to a traditional marketplace business than to pure speculative trading. - Real-World Asset (RWA) and Compliance-Friendly Rails

Stablecoins, tokenized treasuries, on-chain money-market funds, and compliant payment rails are gaining institutional interest. Tokens connected to these rails can benefit from predictable fee streams and the migration of traditional financial volume onto blockchains—especially in remittances, cross-border settlements, and B2B payments.

For all three clusters, due diligence is non-negotiable. Investors should review audited financials or on-chain revenue dashboards, check smart-contract audits, and understand the regulatory posture of the teams involved.

Conclusion: Surviving the Panda Market

Bitcoin’s recent underperformance relative to U.S. equities is not a mystery. A powerful AI equity narrative is capturing mainstream capital; a brutal $20 billion liquidation event reset leverage and scared away fast money; and long-term whales used triple-digit prices to take profits. Meanwhile, gold has reasserted itself as the preferred macro hedge, while Bitcoin continues to trade like a high-beta risk asset.

Yet beneath the surface, this “panda market” is not purely negative. Excess leverage is being flushed out. Weak projects are being separated from those with real revenue and durable use cases. Regulatory clarity is advancing, and the intersection of AI and blockchain is quietly building new infrastructure that could power the next cycle.

For investors searching for new crypto assets, additional income streams, or practical blockchain applications, the message is clear: focus less on the daily price action and more on fundamentals—who pays, for what service, and why the token is necessary. If Bitcoin does reclaim its role as a macro hedge during the next easing cycle and if high-quality altcoins continue to tie token value to real economic activity, today’s panda market may eventually be remembered not as the end of the crypto story, but as the consolidation phase that prepared the ground for the next wave of innovation.