Key takeaways:

- Saylor’s stance: Strategy’s Michael Saylor remains “laser-focused” on Bitcoin despite a visible rise in companies adding Ether (ETH) to balance sheets. He frames broader crypto innovation as net-positive while asserting BTC will keep attracting most treasury capital.

- Corporate adoption is accelerating: Public companies holding BTC reportedly jumped from ~60 to $72–$76B depending on spot.

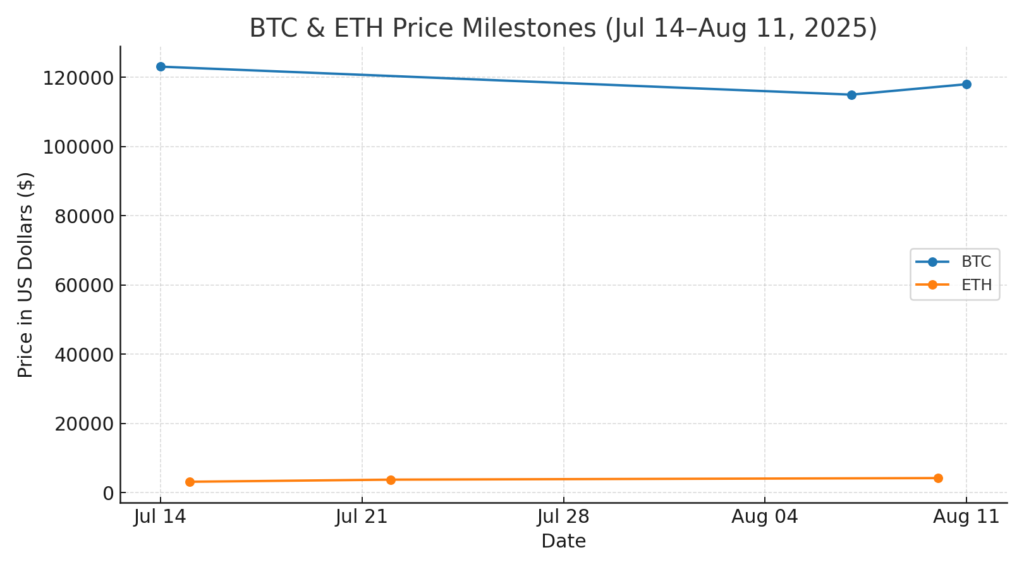

- Price backdrop: Bitcoin printed a new all-time high around $123,000 on July 14, 2025, and is trading near the $118,000 area in mid-August.

- Dominance still with BTC: Bitcoin’s market dominance hovers around 60%, underscoring its role as the primary corporate treasury asset even as ETH gains mindshare.

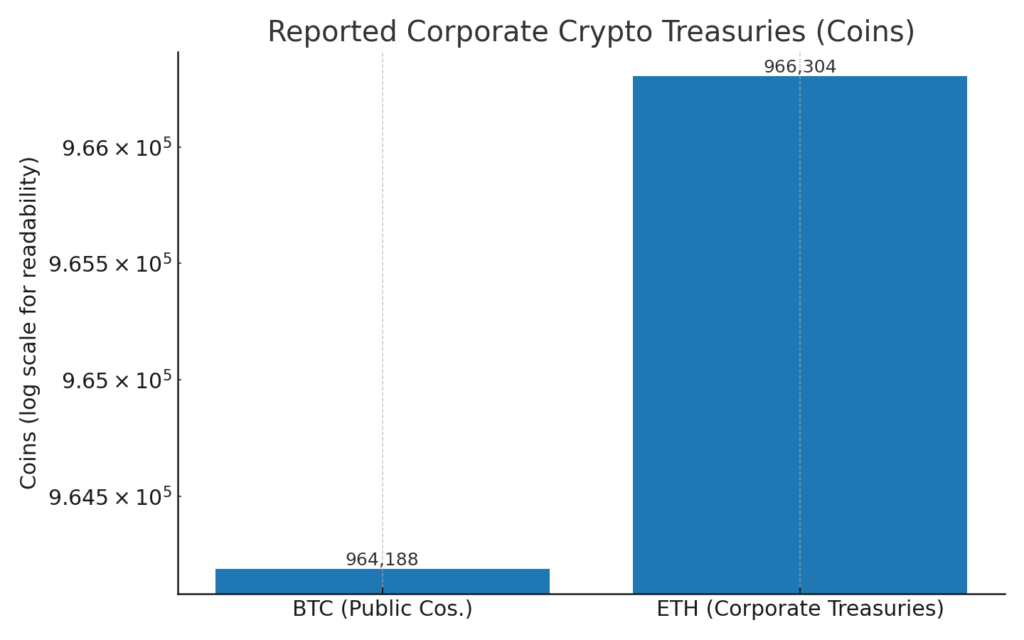

- ETH treasuries are real (and rising): Corporate ETH balances have surged to roughly 966,304 ETH (~$3.5B) as of July, aided by spot ETH ETFs and the appeal of staking yields (~3–4%).

Insert Figure 1 (after this bullet list): “Reported Corporate Crypto Treasuries (Coins)—BTC (Public Cos.) vs ETH (Corporate Treasuries)”

1) What Saylor actually said—and why it matters

In a Bloomberg interview, Strategy’s executive chairman Michael Saylor said he’s not concerned about the growing interest in ETH and other altcoins for corporate treasuries. He called the broader wave of crypto innovation “good for everybody,” but reiterated that the majority of incoming treasury capital still targets Bitcoin, the asset he describes as “digital capital.” The number of companies holding BTC, he added, has climbed dramatically in a short period.

This positioning is consistent with Strategy’s balance sheet: it is the largest corporate holder of Bitcoin, recently disclosing 628,791 BTC after additional purchases in late July and early August. The scale matters because it sets a visible benchmark for CFOs: if your treasury mandate is to preserve purchasing power and gain optionality against monetary debasement, BTC remains the most “audited” and liquid way to do so at corporate scale.

2) The price and dominance context

BTC’s all-time high near $123,000 on July 14, 2025 coincided with a pro-crypto legislative calendar in Washington and broad institutional flows. The pullback since then has been modest; prices have consolidated in the $115,000–$118,000 zone over the past week.

Crucially, Bitcoin still commands ~60% market dominance, illustrating that, even amid cyclical altcoin rallies, BTC remains the crypto market’s gravitational center—especially for corporate treasuries whose boards prize liquidity, custody depth, and regulatory clarity.

Insert Figure 2 (here): “BTC & ETH Price Milestones (Jul 14–Aug 11, 2025)”

Note: Figure 2 highlights milestone prints (ATHs and reference closes) rather than a full tick-by-tick series, to contextualize the discussion with clear dates.

3) Corporate treasuries: Bitcoin vs. Ethereum

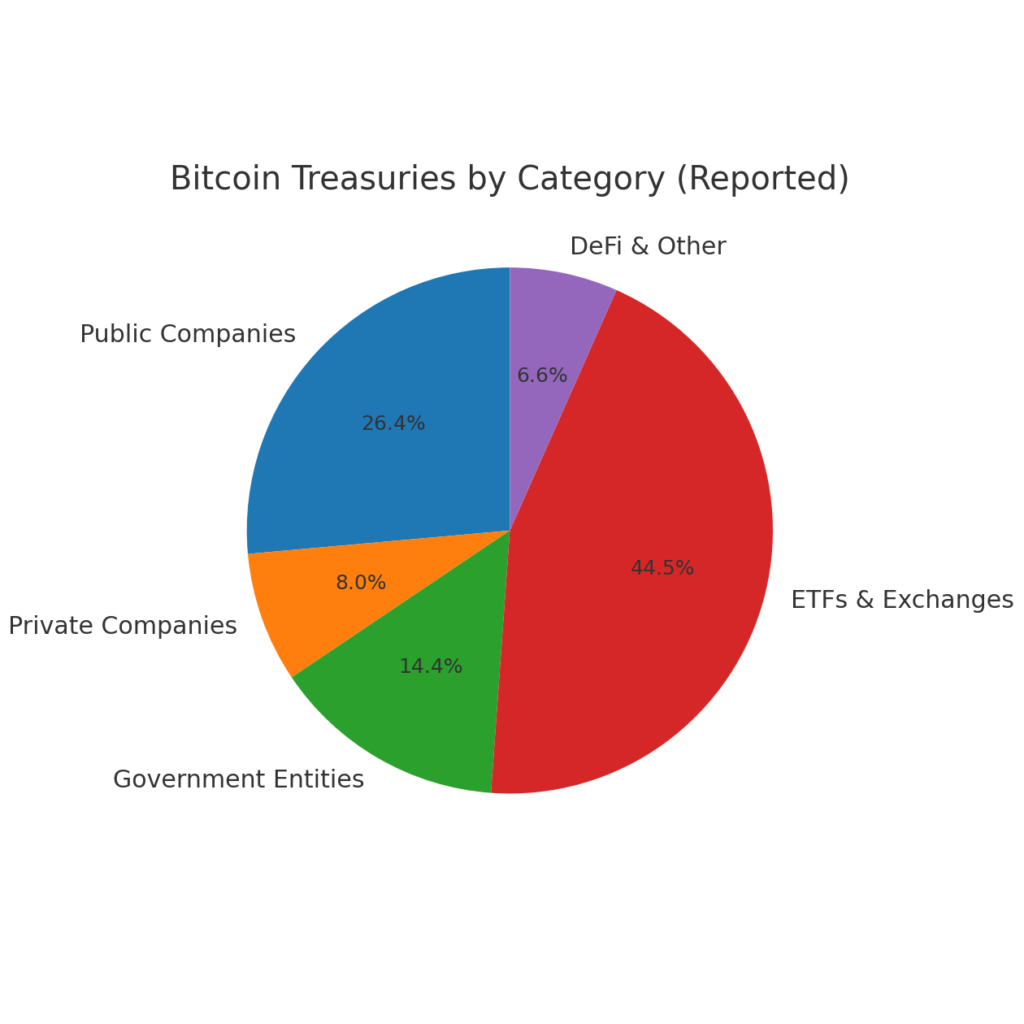

Bitcoin treasuries. Strategy’s position sits atop a broader wave of corporate BTC adoption. Aggregators tracking public and private entities, governments, and ETFs estimate millions of BTC held by institutions, with public companies alone near ~964,000 BTC. Category totals (public, private, governments, ETFs/exchanges, DeFi/other) show an increasingly institutional footprint.

Insert Figure 3 (here): “Bitcoin Treasuries by Category (Reported)”

Ethereum treasuries. On the ETH side, corporate balances are rising fast. Reuters recently tallied roughly 966,304 ETH (~$3.5B) in corporate hands as of July—up from under 116,000 ETH at the end of 2024—driven by price recovery, spot ETH ETF visibility, and staking yields that can translate idle treasury assets into programmable, yield-bearing capital.

While sourcing for ETH treasuries is more fragmented than for BTC, notable disclosures and media coverage point to SharpLink Gaming and BitMine Immersion as active acquirers (with self-reported totals in the hundreds of thousands of ETH), alongside a long tail of smaller public companies. The broad trend: ETH is emerging as the “productive” treasury complement to BTC’s “pure store-of-value” role.

4) ETF flywheel effects—and what’s different for ETH

Spot ETH ETFs have added a new demand channel. July saw multi-billion-dollar net inflows into the leading funds before early-August outflow days prompted healthy two-way trading. This ETF flywheel—primary market creations/redemptions interacting with secondary-market flows—supports deeper liquidity, clearer price discovery, and easier exposure for corporates unable (or unwilling) to self-custody.

Mechanically, the ETH ETF story differs from BTC in one respect: staking. Although U.S. funds are navigating staking constraints (and tax/custody questions), the existence of on-chain yield makes corporate ETH strategies naturally two-dimensional (price + yield), whereas BTC strategies are generally one-dimensional (price exposure), occasionally supplemented by loan-desk yields or basis trades.

5) For builders and investors: where the opportunities are

A. Treasury-adjacent yield strategies (ETH)

- Staking with robust ops hygiene: For corporates that can take ETH onto their balance sheet, carefully structured staking can add 3–4% yield without leaving the ETH beta. Risk management should cover validator slashing risk, downtime penalties, and auditor-vetted custody/signing paths (HSM/MPC).

- ETH basis trades via ETFs: If self-custody is restricted, cash-and-carry variants using spot ETH ETFs on the long leg and futures on the short leg can generate annualized carry with transparent, audited positions. (Tax and accounting treatment varies—consult advisors.)

B. Bitcoin treasury optimization (BTC)

- Capital structure engineering: Strategy’s recent purchases illustrate how corporates can sequence equity and preferred issuance to add BTC while targeting enterprise-value/holdings ratios that keep traditional investors comfortable.

- Liquidity stacking: BTC’s depth across venues allows treasury teams to blend custody providers, ETFs for short-term window dressing, and direct holdings for strategic long-term exposure.

C. Discovery of “next treasury adopters” (equity alpha)

- Screen 1: Press-release language and ATM usage. Watch for small/mid-caps raising equity under ATM programs and explicitly signaling crypto purchases (often followed by heightened trading volumes). Reuters highlighted several names that saw stock pops after ETH announcements.

- Screen 2: Board composition and advisors. Companies adding directors with crypto capital-markets experience or custody/regulatory backgrounds are often pre-positioning.

- Screen 3: Policy readiness. Firms citing internal digital-asset policies (custody, keys, risk, accounting) are more likely to move from exploration to deployment.

6) Risks and governance you cannot ignore

- Accounting/impairment & audit readiness (BTC/ETH): Fair-value treatment, impairment triggers, and auditability remain central. A robust policy stack—valuation sources, access controls, segregation of duties, key ceremonies—is non-negotiable for listed issuers.

- Regulatory and tax uncertainty (ETH staking): As Reuters noted, staking tax treatment and custodial responsibilities are still evolving; policy changes can swing after-tax yields and risk weights.

- Liquidity and volatility: ETF-driven flows can cut both ways; early-August outflow streaks showed that ETH vehicles can see sizeable redemptions, which may amplify price swings in thin hours.

- Operational risk: Whether it’s Bitcoin cold storage or Ethereum validator ops, the weakest link is often human. Use multi-party authorization, periodic tabletop incident drills, and independent SOC 2-grade service partners.

7) Data notes and caveats

- Holdings tallies vary by source and definition. For BTC, we referenced category totals (public, private, government, ETFs/exchanges) that show the breadth of institutional adoption; for ETH, corporate tallies are growing but still more fragmented. Wherever possible we use primary disclosures (company or fund PR/filings) or top-tier media (Reuters, FT, Barron’s, Bloomberg) and note when numbers are self-reported.

- Dominance figures fluctuate intraday. We cite TradingView/CoinMarketCap for methodology and context rather than a single hard print.

8) Bottom line

BTC remains the corporate cornerstone, buoyed by dominance near ~60%, deep liquidity, and a maturing ETF complex. ETH is gaining treasury appeal because it can be productive (staking) and now has ETF rails that lower the operational barrier. Saylor’s lack of concern about ETH treasuries is logical: crypto’s rising tide can lift both boats, but capital gravity—for now—still favors the original.

If your mandate is to protect purchasing power with maximal simplicity and auditability, BTC is still the first stop. If you’re also tasked with earning on idle assets and piloting on-chain finance, adding a risk-managed ETH sleeve (direct or via ETFs with policy guardrails) is increasingly defensible.

Actionable playbook for the next 90 days:

- Finalize/refresh digital-asset policy and control maps (custody, signers, incident response).

- If BTC-only today, evaluate a small ETH pilot (ETF or segregated custody) with explicit staking/tax guardrails.

- Build a monitoring screen for likely treasury adopters; review primary disclosures weekly and track flows into BTC/ETH ETFs for confirmation.