Main Points :

- Venture capitalist Chamath Palihapitiya argues that Bitcoin lacks two structural features required for central bank reserve assets: fungibility and privacy.

- Bitcoin’s traceability and transparent ledger could make it difficult for central banks to hold and circulate coins with controversial histories.

- Gold retains advantages in anonymity and fungibility, which are historically important characteristics for reserve assets.

- Crypto industry leaders such as Bitwise CIO Matt Hougan counter that gold itself has structural weaknesses, including storage, transportation, and settlement limitations.

- The debate highlights a broader transformation in global finance, where Bitcoin, stablecoins, and tokenized assets may coexist with traditional reserve systems.

The Debate Over Bitcoin as a Central Bank Reserve Asset

The question of whether Bitcoin could ever become a central bank reserve asset has become a major topic of debate in global financial circles. Venture capitalist and billionaire investor Chamath Palihapitiya, known for his early support of Bitcoin as a long-term inflation hedge, recently sparked controversy by pointing out what he considers two fundamental structural weaknesses in Bitcoin: lack of fungibility and lack of privacy.

Palihapitiya, a former Facebook executive and prominent technology investor, has long been bullish on Bitcoin. In previous interviews, he described Bitcoin as one of the best inflation hedges available and even suggested that it could become a breakout asset over the next 50 to 100 years. However, during an appearance on the “People by WTF” podcast held alongside discussions at the World Government Summit, he presented a more nuanced view.

According to Palihapitiya, Bitcoin may be an excellent investment asset for individuals, institutions, and ETFs, but it currently lacks certain characteristics required for central bank reserve assets. These structural issues could prevent it from achieving widespread adoption among national monetary authorities.

Structural Issue 1: The Fungibility Problem

One of the central issues Palihapitiya raised is fungibility, a concept that describes whether each unit of an asset is interchangeable with every other unit.

For a currency or reserve asset to function effectively, each unit must be identical and interchangeable without discrimination. In the case of gold, one ounce of pure gold is effectively indistinguishable from another ounce of pure gold. This property allows gold to function smoothly as a reserve asset.

Bitcoin, however, exists on a fully transparent public ledger. Every transaction ever conducted on the network is permanently recorded on the blockchain. This means that each coin can theoretically be traced back through its entire transaction history.

If a particular Bitcoin was previously associated with illegal activities—such as money laundering, ransomware payments, or sanctions violations—institutions may treat it differently from “clean” coins. In extreme cases, certain exchanges or compliance systems may even refuse to accept coins with controversial histories.

This introduces the concept of “tainted coins,” which undermines the idea that every Bitcoin is identical. From a central bank perspective, this lack of perfect fungibility could become a serious obstacle.

Structural Issue 2: The Privacy Problem

The second structural issue Palihapitiya highlighted is privacy.

Central banks traditionally operate with a high degree of secrecy regarding their reserve holdings. Governments rarely disclose the exact details of how their reserves are distributed, especially when it comes to gold reserves or foreign currency holdings.

Gold, for example, offers a high degree of anonymity. It is difficult for outsiders to know exactly how much gold a central bank holds or where that gold is stored.

Bitcoin, by contrast, operates on a fully transparent blockchain. If a central bank were to hold Bitcoin in publicly identifiable addresses, the entire world could theoretically monitor those holdings in real time.

For governments and monetary authorities, this transparency may create political and strategic risks. Large transfers of Bitcoin by a central bank could potentially influence markets or signal policy changes.

From Palihapitiya’s perspective, these privacy limitations make Bitcoin structurally incompatible with the traditional role of central bank reserve assets.

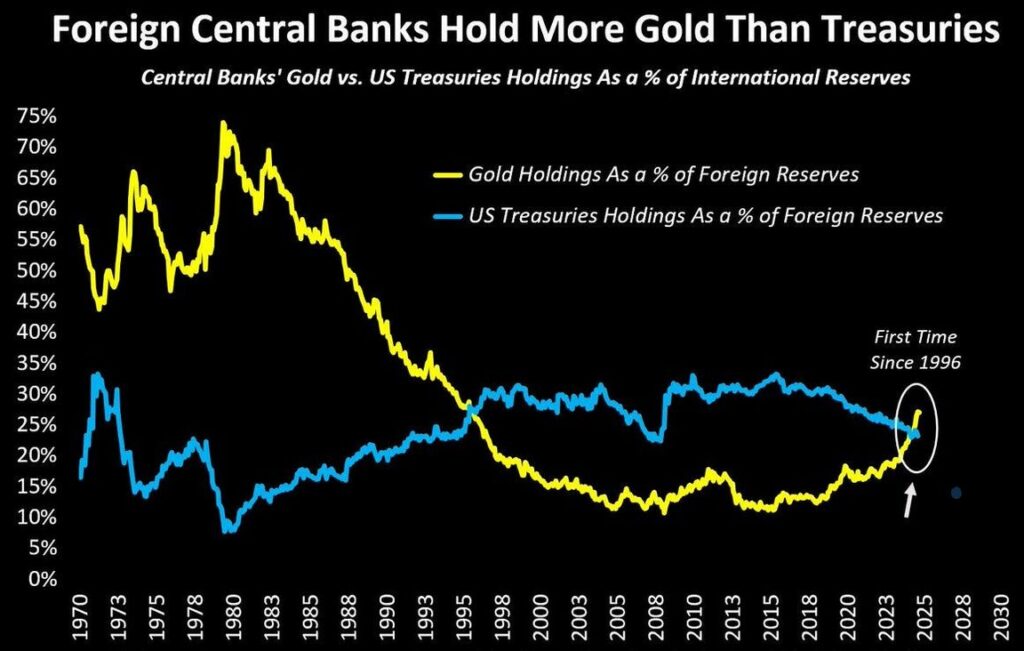

Why Gold Still Dominates Reserve Assets

Despite the rise of digital assets, gold remains one of the most important reserve assets in the world. According to data from the World Gold Council, central banks collectively hold over $2.2 trillion worth of gold reserves.

Global Central Bank Gold Reserves

The reasons for gold’s enduring dominance include:

- Long historical precedent as a store of value

- Strong fungibility characteristics

- Limited transparency in ownership

- Independence from digital infrastructure

Because gold transactions are largely opaque and physical, they offer governments flexibility in managing reserves without revealing strategic moves.

Palihapitiya argues that these characteristics make gold naturally suited for central bank reserves in ways Bitcoin currently cannot replicate.

Counterargument: Bitcoin Solves Gold’s Weaknesses

Not everyone in the crypto industry agrees with Palihapitiya’s analysis.

Matt Hougan, Chief Investment Officer at crypto asset management firm Bitwise, quickly responded on social media. Hougan argued that Palihapitiya exaggerates Bitcoin’s flaws while ignoring gold’s structural weaknesses.

According to Hougan, gold suffers from several significant limitations:

- It is difficult to use in global financial settlements due to its physical nature.

- Large amounts of gold must be stored in third-party vaults, creating counterparty risks.

- Gold is expensive and slow to transport internationally.

Bitcoin, on the other hand, can be transferred across borders instantly without requiring physical transportation or trusted custodians.

Gold vs Bitcoin Reserve Asset Characteristics

Hougan also pointed out that Bitcoin ownership can be made relatively private through operational practices such as address rotation and cold storage structures. While the blockchain is transparent, identifying the owner of an address is not always straightforward.

From this perspective, Bitcoin may still evolve into a complementary reserve asset rather than replacing gold entirely.

The Role of Stablecoins in the New Financial Architecture

Another important point raised in the discussion is the growing importance of stablecoins.

Palihapitiya described stablecoins as a structural innovation that could reduce friction in global payments and financial infrastructure.

Stablecoins—digital tokens pegged to fiat currencies such as the US dollar—are increasingly used for:

- Cross-border payments

- On-chain liquidity in decentralized finance

- International remittances

- Settlement between financial institutions

The stablecoin market has grown dramatically in recent years.

Global Stablecoin Market Growth

Major stablecoins such as USDT and USDC now collectively process trillions of dollars in annual transaction volume, rivaling traditional payment networks in certain regions.

This trend suggests that while Bitcoin may face challenges as a central bank reserve asset, other blockchain-based financial instruments could play significant roles in the global financial system.

Emerging Crypto Assets Addressing Privacy and Fungibility

Some cryptocurrency projects attempt to solve the exact issues Palihapitiya identified.

Privacy-focused cryptocurrencies such as Monero and Zcash incorporate advanced cryptographic techniques that obscure transaction histories and improve fungibility.

These technologies include:

- Zero-knowledge proofs

- Ring signatures

- Stealth addresses

Privacy vs Transparency Spectrum in Cryptocurrencies

However, these projects remain relatively small compared with Bitcoin and face regulatory challenges due to concerns about illicit finance.

As a result, they have not yet achieved the scale or institutional acceptance required to become reserve assets.

Bitcoin’s Investment Case Remains Strong

Despite his criticisms, Palihapitiya made it clear that he remains optimistic about Bitcoin as an investment asset.

Bitcoin continues to attract institutional capital through vehicles such as:

- Spot Bitcoin ETFs

- Corporate treasury allocations

- Hedge fund strategies

- Sovereign wealth experiments

Bitcoin’s limited supply of 21 million coins and its decentralized nature continue to make it attractive as a long-term hedge against monetary inflation.

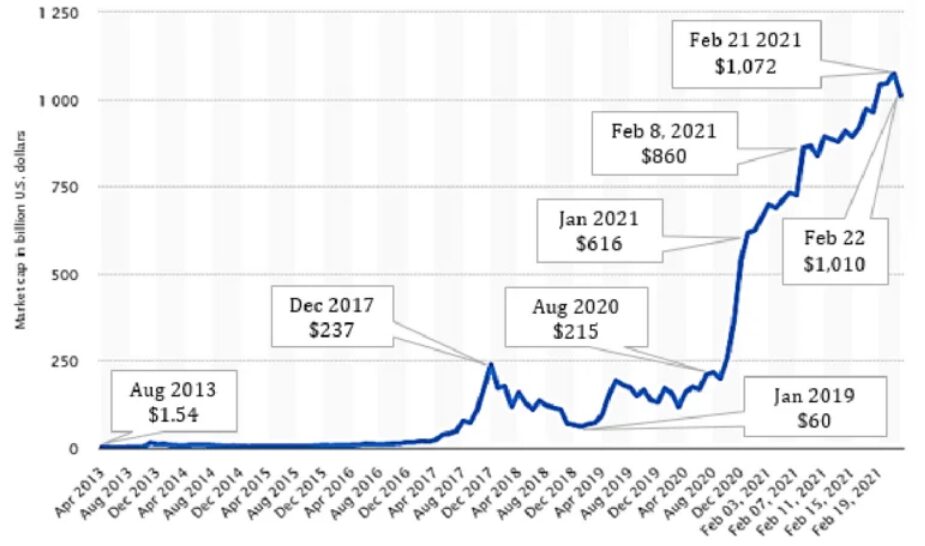

Bitcoin Market Capitalization Growth

However, Palihapitiya also suggested that Bitcoin’s era of delivering massive speculative returns may be gradually evolving into a more mature phase of market behavior.

Instead of functioning purely as a speculative asset, Bitcoin may become a foundational component of digital financial infrastructure.

The Future of Reserve Assets in a Digital World

The debate between Palihapitiya and Hougan highlights a broader transformation taking place in global finance.

For more than a century, central bank reserves have primarily consisted of:

- Gold

- U.S. dollars

- Other major reserve currencies

But the rise of digital assets is introducing new possibilities.

Some economists speculate that future reserve systems may include a diversified basket of assets, including:

- Gold

- Government bonds

- Bitcoin

- Tokenized commodities

- Central bank digital currencies (CBDCs)

In such a system, Bitcoin may not replace gold, but it could coexist alongside it as a digital reserve asset.

Conclusion

The debate over Bitcoin’s suitability as a central bank reserve asset reflects deeper questions about the evolution of global financial systems.

Chamath Palihapitiya argues that Bitcoin’s lack of fungibility and privacy creates structural barriers that prevent it from fulfilling the traditional role of reserve assets. Meanwhile, industry leaders such as Bitwise CIO Matt Hougan believe these concerns are overstated and that Bitcoin may ultimately complement gold rather than compete with it.

At the same time, stablecoins and other blockchain innovations are rapidly transforming global payment infrastructure, suggesting that the future of finance may involve a hybrid system combining digital and traditional assets.

Whether Bitcoin eventually joins gold in central bank vaults remains uncertain. What is clear, however, is that digital assets are steadily reshaping the foundations of global monetary architecture.