Main Highlights:

- Bitcoin mining profitability edged up ~2 % in July, led by a 7 % surge in BTC price versus a 5 % rise in network hashrate.

- U.S.-listed miners increased their global hashrate share from 25 % to 26 %, mining 3,622 BTC vs. 3,379 BTC in June.

- IREN and MARA Holdings led production, with 728 BTC and 703 BTC mined respectively.

- MARA held the highest energized hashrate at 58.9 EH/s, followed by CleanSpark at 50 EH/s.

- Revenue per EH/s rose to about $57,000/day in July, from ~$56,000 in June, and ~$50,000 a year ago.

- Despite improvements, profitability remains substantially below pre-halving levels.

- Recent institutional activity and Bitcoin’s upward price momentum may further shift the mining landscape.

1. A Slight Yet Significant Profitability Uptick

In July 2025, investment bank Jefferies highlighted that Bitcoin mining profitability increased by approximately 2 %, a movement largely driven by a combination of the latest price and network dynamics. Specifically, Bitcoin’s price climbed roughly 7 % while the network hashrate rose by about 5 %. This mismatch — price outpacing hashrate — translated into improved profits for miners.

This modest increase may seem incremental, but in an industry where margins are perpetually squeezed by rising difficulty and operational costs, even a small gain can be meaningful, especially for mining operations operating at scale or seeking to push into profitability more firmly.

2. U.S.-Listed Miners Gain Further Ground

U.S.-listed mining companies expanded their footprint within the global Bitcoin mining network. In July, this cohort mined a total of 3,622 BTC, up from 3,379 BTC in June, raising their share of the total network’s mining output to 26 %, compared to 25 % in the prior month.

This indicates an ongoing consolidation in the mining industry, where capital-rich enterprises — predominantly U.S.-listed — are able to ramp operations and secure a greater share of profits. For investors exploring mining-related opportunities or infrastructure projects, this underscores the strategic advantage of backing larger, better-capitalized miners.

3. Leading Firms: IREN, MARA Holdings, and CleanSpark

Within the U.S.-listed mining cohort, two firms distinguished themselves in July: IREN, which mined 728 BTC, and MARA Holdings, which followed closely with 703 BTC. Further, MARA reported the highest energized hashrate at 58.9 EH/s, with CleanSpark trailing at 50 EH/s.

These figures illustrate not only production volume but also the scale of infrastructure investment and operational throughput, as energized hashrate reflects the computational power actively contributing to mining. Stakeholders evaluating mining firms for partnerships, investment, or competitive analysis should closely watch these metrics.

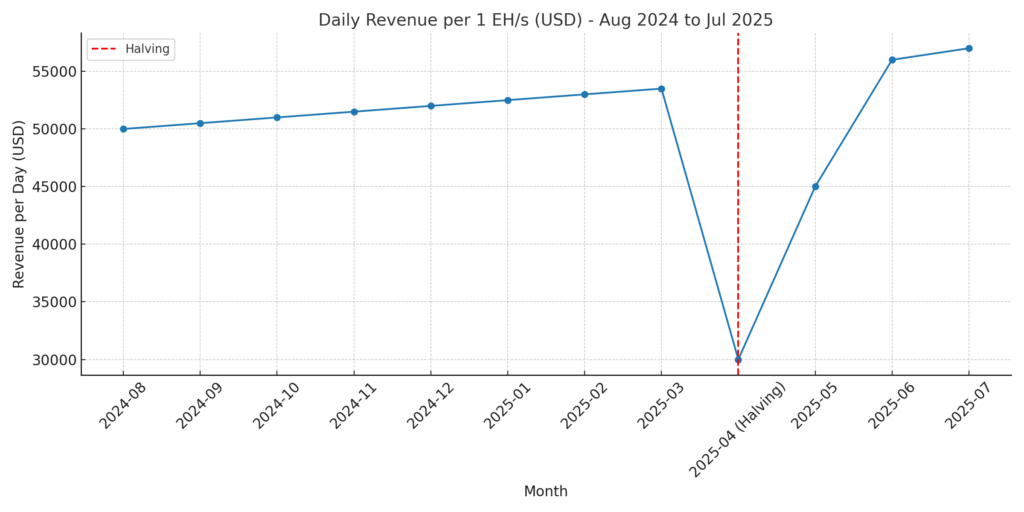

4. Revenue Per Hashpower: Improved but Below Pre-Halving Levels

The amount of revenue generated per exahash per second (EH/s) improved in July. Jefferies noted that a hypothetical 1 EH/s fleet of mining equipment would have yielded approximately $57,000 per day — up from $56,000 in June and from about $50,000 a year earlier.

However, JPMorgan’s analysis adds context: while this daily block reward revenue of $57,400 per EH/s is indeed the highest since the most recent halving, it remains roughly 43 % below pre-halving revenue levels; gross profit per EH/s is similarly about 50 % lower.

Hence, relative gains are tangible, but the shadow of the halving continues to press on long-term profitability. Firms must adopt efficiencies or innovative cost-structures to navigate this reality.

[Insert Graph Here] Figure Title: Revenue per EH/s Over Time – July 2024 to July 2025

5. Why Profitability Remains Pressured Post-Halving

Bitcoin halving events, which halve the block reward approximately every four years, fundamentally reshape mining economics. The 2024 halving reduced the block reward, immediately cutting miners’ issuance reward in half. Consequently, underlying profitability metrics — whether revenue or gross profit per EH/s — have faced structural declines. Despite resilient Bitcoin prices, these cost structures are still recovering to prior norms.

Moreover, network difficulty remains high. JPMorgan noted that network hashrate rose to roughly 899 EH/s in July, and mining difficulty increased by 9 % during the month, placing pressure on less efficient or higher-cost operations.

6. Institutional Momentum and Market Sentiment

Beyond the immediate operational details, broader macro- and institutional trends are also shaping the mining sector. As of mid‑August, Bitcoin itself is hitting new all-time highs, notably climbing to around $123,600 on expectations of U.S. Federal Reserve rate cuts, enhancing liquidity and speculative interest.

Meanwhile, corporate accumulation remains strong. For instance, Strategy (formerly MicroStrategy) added 21,021 BTC to its treasury, deploying some $2.46 billion and raising its total holdings to nearly 629,000 BTC — underscoring strong institutional conviction in Bitcoin as an alternative asset.

These signals suggest that the mining industry is buoyed not only by higher BTC prices, but also by growing institutional adoption and confidence — although the long-term trajectory depends on policy, macroeconomics, and energy cost dynamics.

7. Implications for New Crypto Projects and Practical Blockchain Applications

For innovators and practitioners exploring new crypto assets or blockchain-based revenue models:

- Mining infrastructure remains capital intensive, favoring scaled operators with energy efficiency and geographic cost advantages.

- New blockchains or protocols relying on PoW must consider competitive hashpower dynamics and interpret recent trends accordingly.

- Alternative consensus mechanisms (e.g., PoS, PoA, or hybrid models) may become more economically viable, as PoW’s barrier to entry and sensitivity to halving events persist.

- Innovation opportunities lie in mining rental, hosting services, or decentralized hashpower marketplaces — sectors where institutional miners are already gaining an edge.

- Enterprise or industrial blockchain use cases should weigh ROI over time, considering mining profitability pressure and future utility requirements.

Conclusion

In July 2025, Bitcoin mining profitability registered a modest yet meaningful 2 % uptick, buoyed by a stronger BTC price (+7 %) that outpaced a 5 % rise in network hashrate. U.S.-listed miners continue to consolidate their share of global activity, with top players like IREN and MARA Holdings setting the pace in output and computational capacity. Revenue per hashpower improved to the highest post-halving levels, yet overall profitability remains suppressed relative to pre-halving benchmarks.

For stakeholders ranging from crypto investors to blockchain practitioners and enterprise operators, these dynamics reinforce key lessons: scale matters, efficiency is indispensable, and strategic positioning in energy, capital, and institutional alignment can determine success in a competitive PoW landscape. As macro factors — including policy shifts and institutional confidence — continue to influence market traction, miners and builders alike should watch August and beyond for how these forces evolve.