Main Points :

- The total debt of publicly listed Bitcoin miners has soared from approximately US$2.1 billion to US$12.7 billion over the past 12 months.

- The drivers include intensified competition for hash-rate after the April 2024 halving (reward per block down to 3.125 BTC), compelling miners to upgrade hardware and broaden into AI and HPC hosting.

- Debt financing has replaced equity as the prime capital‐raising route for many miners, thanks to lower cost and more predictable cash‐flow frameworks tied to AI/HPC contracts.

- The pivot to AI/HPC hosting is viewed as a way to stabilise earnings, yet introduces execution risk, rising interest costs and heavy CapEx burdens.

- Despite the transition, analysts believe these shifts do not threaten the underlying security of the Bitcoin network; rather they may reinforce it via surplus power monetisation.

1. Debt Explosion in the Bitcoin Mining Sector

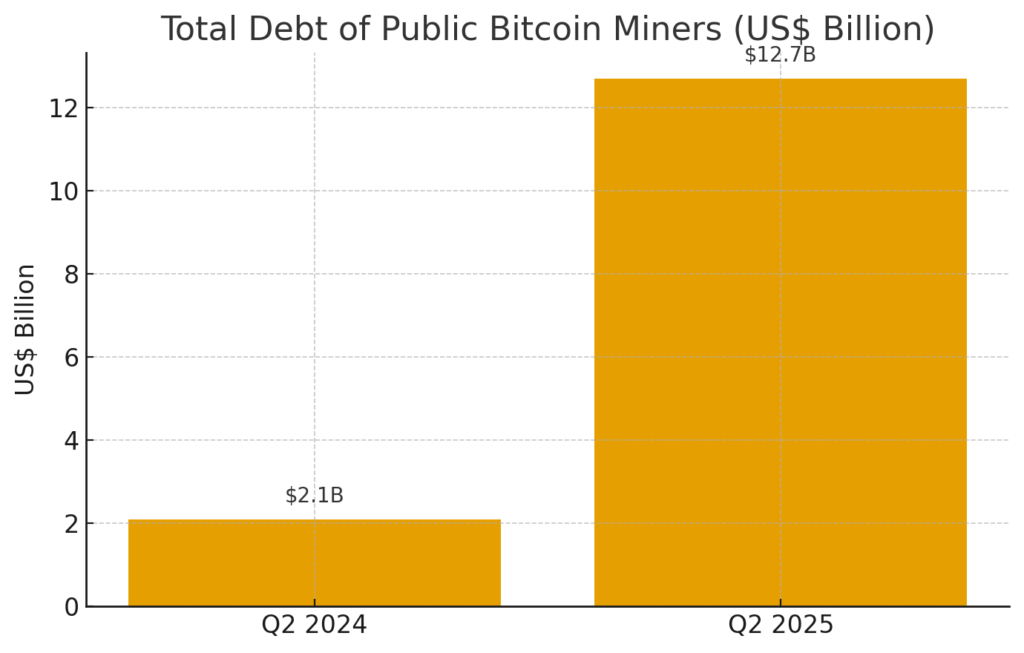

Over the past year, the debt burden carried by publicly traded Bitcoin mining companies has ballooned. According to the most recent analysis by VanEck, the aggregate debt of these operators rose from around US $2.1 billion in Q2 2024 to approximately US $12.7 billion in Q2 2025.

This roughly 500 % increase underscores the mounting financial pressure miners face. As noted, the problem is described as the “melting ice cube” phenomenon: if miners do not continuously upgrade to the latest ASIC hardware or diversify their business models, their share of the global hash-rate will shrink, reducing their daily Bitcoin reward allotments.

Historically, miners raised capital via equity markets, but the current landscape—where revenue streams are highly volatile and tied closely to the price of Bitcoin (BTC)—makes underwriting debt backed purely by mining income more challenging. Consequently, many miners are shifting to debt financing because it can be structured around more predictable revenue streams (such as multi-year contracts) and may offer lower cost of capital.

For investors and the broader crypto ecosystem, this evolution has significant implications. A rapidly leveraged mining industry raises questions around refinancing risk, energy cost exposure, and the sustainability of mining business models in a post-halving era.

2. Post-Halving Reality and the Hash-Rate Arms Race

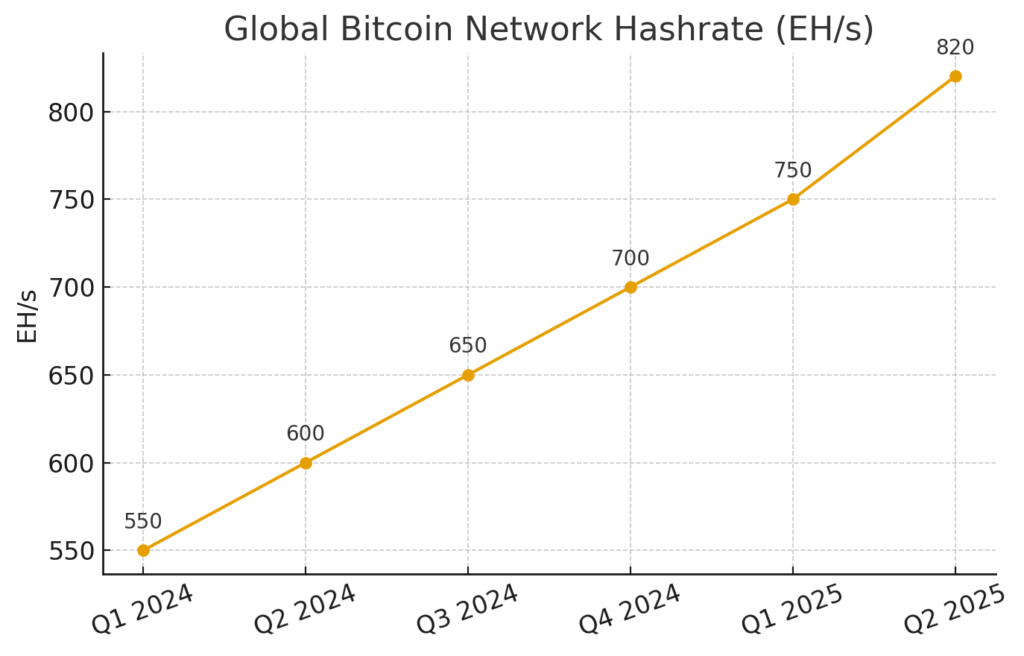

In April 2024, Bitcoin underwent its scheduled block-reward halving, reducing the reward to 3.125 BTC per block for miners. This cut in revenue per unit of work intensified pressure on mining operators to scale, improve efficiency, and capture larger slices of the network’s hash-rate.

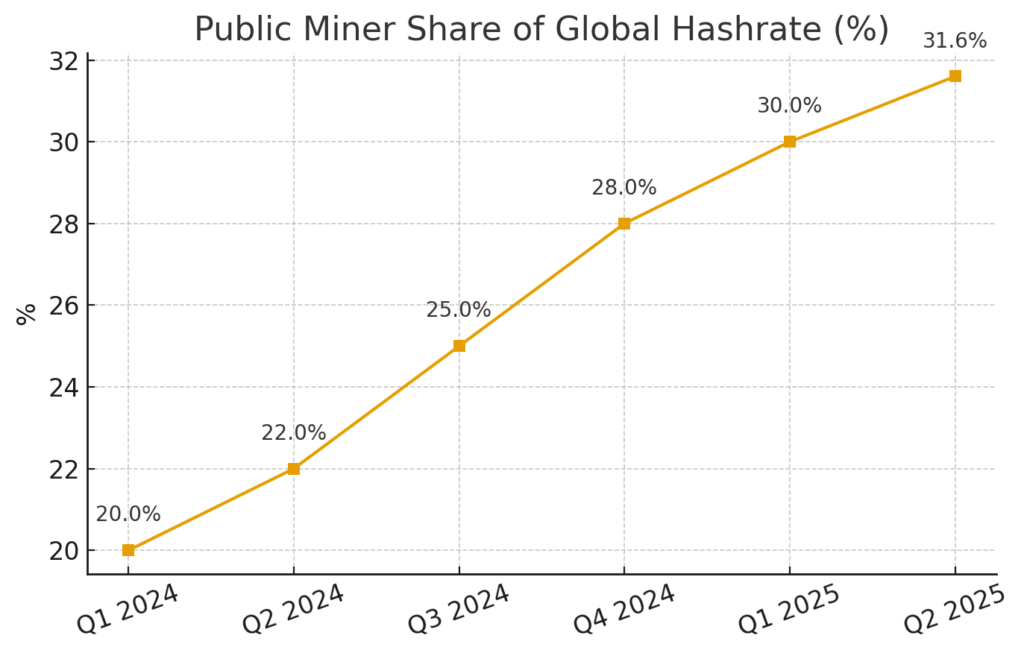

As the largest public miners together recorded realised hash-rates of 150 EH/s a year earlier and reached approximately 326 EH/s in September 2025, representing ~31.6 % of the global network, the competitive landscape has clearly intensified.

To remain competitive, miners are investing in next-generation ASICs, expanding infrastructure, and seeking lower-cost energy sources. But those investments require large capital outlays at a time when margins from pure mining are under strain. Hence the surge in capital-raising and debt accumulation.

From an asset-seeker’s standpoint, this trend suggests that integration points between mining, energy markets and computation (AI/HPC) are increasingly relevant. A pure bet on mining hardware alone may face headwinds; the structural upgrade of the mining model is in full motion.

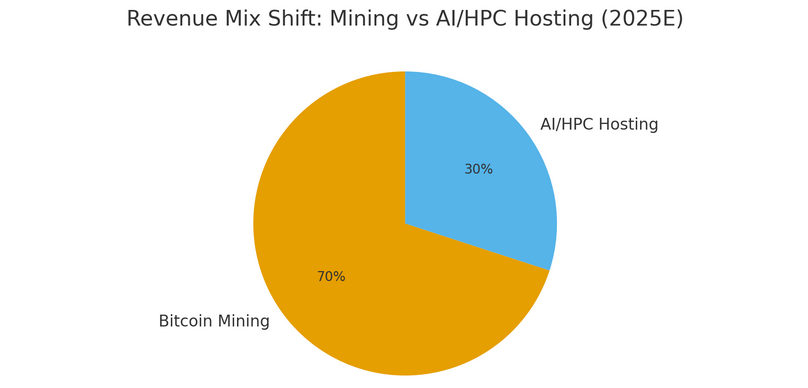

3. The AI/HPC Hosting Pivot: A New Business Model

One of the most significant developments in recent months is the pivot by mining firms into hosting high-performance computing (HPC) and artificial intelligence (AI) workloads. Given that mining data centers already require substantial power, cooling and network infrastructure, some miners view themselves as a natural fit for HPC/AI colocation services.

Such deals allow miners to lock in more predictable multi-year contracts with large customers, thereby reducing reliance on volatile daily Bitcoin rewards. For example:

- Some firms issued convertible notes and senior secured bonds explicitly to fund AI/HPC infrastructure.

- The shift is not primarily driven by an ideological commitment to AI, but by pragmatic financial engineering: miners are monetising idle capacity or excess power during non-peak mining periods.

From the perspective of someone exploring crypto or blockchain infrastructure opportunities, this pivot raises interesting possibilities:

- Infrastructure-as-a-Service (IaaS) tied to blockchain/AI convergence may present new tokenisation or B2B models.

- Collaboration potential exists between miners and Web3 ecosystems (e.g., decentralised AI training, computation tokens, energy-based revenue sharing).

- For altcoin investors, the broader ecosystem shift may boost demand for networks or tokens that enable mining/hosting hybrid models (e.g., decentralised compute markets, energy-tokenised assets).

That said, execution risk is non-trivial: success hinges on securing large customers, managing power infrastructure effectively, and navigating regulatory and energy-market risks.

4. Risks, Hidden Costs and the Silent Threats

While the mining industry’s shift makes strategic sense, it is not without substantial risk. Key risk vectors include:

- Rising interest and refinancing costs: Debt has replaced equity financing, but if interest rates remain elevated or capital markets sour, the debt burden may impose stress.

- Execution risk in AI/HPC hosting: Landing long-term contracts is one thing; delivering infrastructure, managing power, satisfying customers is another. Many miners pivoting to AI are facing the test.

- Energy and regulatory exposure: Mining and hosting operations are heavily dependent on energy availability and cost, and regulatory regimes (especially in jurisdictions like New York) are already scrutinising miners with higher power taxes or environmental limitations.

- Dependency on Bitcoin network and coin price: While the hosting pivot mitigates some of the dependence, most miners remain anchored to the economics of Bitcoin itself. A major down-cycle in BTC price or a rise in hash-rate making mining unprofitable still looms as a threat.

For new asset seekers or blockchain practitioners, these risks imply that any involvement in mining infrastructure or mining-adjacent tokens should factor in debt exposure, power contracts, and hosting business viability — not just hashrate growth or mining rewards.

5. Implications for Investors, Blockchain Practitioners and New Asset Seekers

Given the above developments, several key implications emerge for those looking to identify new crypto-assets, infrastructure plays or practical blockchain use-cases:

- Infrastructure tokens and compute-utility tokens gain relevance: As mining firms turn into hosting/compute providers, tokens or projects that provide verifiable access to compute resources, or tie mining and AI services on-chain, may emerge as interesting targets.

- Energy-tokenisation and monetisation becomes more relevant: The concept of converting excess energy (especially in mining facilities) into monetisable compute or tokenized revenue streams is gaining traction. For example, miners may monetise otherwise idle power by switching to AI workloads when mining demand falls.

- Due diligence should include host-contract and power-cost metrics: For any investment in mining or compute-adjacent projects, assessing the quality of hosting contracts, duration, customer type, energy cost and regulatory exposure may reveal the real earnings sustainability (rather than just hash-rate growth).

- Altcoins focused on compute, staking, or decentralised AI might benefit: As the mining sector retools around AI/HPC, crypto networks that provide decentralised compute markets, staking of compute resources, or incentivise on-chain AI workloads may gain indirect benefit.

- Mining stocks or tokens carry new risk profiles: For those familiar with mining equities or tokens, the debt explosion means that balance‐sheet risk is now higher. The assumption that mining ops simply scale linearly with hashrate is outdated; the business model is in transition.

6. What this Means for the Bitcoin Network and Crypto Ecosystem

Despite concerns that miners shifting to AI/HPC might undermine the Bitcoin network’s security, analysts at VanEck and others believe the opposite could hold true:

- Mining facilities converting excess power into AI/HPC workloads may make better use of capacity, thereby improving overall utilisation and economics.

- The term “melting ice cube problem” emphasises that without continual investment, miners will fall behind, so the pivot can be viewed as an evolution of the mining ecosystem rather than its destruction.

From a network view, miners who remain viable and profitable are more likely to continue supporting network security. If many weaker miners exit due to high debt burdens or energy cost pressures, network consolidation might increase—but this also carries centralisation risk. For the broader crypto ecosystem, the convergence of mining, energy, AI and compute infrastructure signals that the lines between “mining” and “cloud/data‐centre” are blurring.

7. Charts & Visuals (Insert at this point)

Suggested chart captions:

- “Figure 1: Total debt of publicly listed Bitcoin miners (US$ billion) – 2024 vs 2025”

- “Figure 2: Global Bitcoin network hash-rate progression (EH/s) and public miner share”

- “Figure 3: Mining-to-AI/HPC pivot: Infrastructure revenue mix infographic”

8. Conclusion

The past 12 months have brought a dramatic transformation in the Bitcoin mining sector. A six-fold surge in debt—from roughly US$2.1 billion to US$12.7 billion—reflects the urgency for mining firms to upgrade hardware, compete in hash-rate, and diversify into AI and HPC hosting. The “melting ice cube problem” succinctly summarises the dynamic: miners must either constantly invest or see their share of rewards erode.

For practitioners, investors, and those seeking new crypto-assets, the significance is clear: mining is no longer a simple function of deploying ASICs and earning BTC. It has evolved into a complex interplay of energy, infrastructure, debt financing, compute hosting and contract streams. Opportunities may lie in tokens or platforms that support decentralised compute, energy efficiency, or mining-adjacent services. But higher leverage, rising power costs and execution risk mean this is a terrain for the informed and the strategic—not the passive.

From a systems perspective, the shift does not pose an imminent threat to the Bitcoin network’s security; in fact, by enabling miners to monetise excess capacity and stay profitable, it may reinforce network resilience. Nevertheless, the ecosystem is changing. For anyone exploring blockchain applications, new crypto investments or infrastructure plays, understanding this mining-hosting pivot is essential.