Main Points :

- Bitcoin has fallen roughly 30% from its all-time high, while gold and silver continue to post record prices, signaling a rare and meaningful divergence.

- Large-holder (whale) selling pressure, declining ETF inflows, and weakening on-chain demand are key factors restraining Bitcoin’s upside.

- Capital has rotated toward traditional safe havens (gold, silver) and AI-driven equities, leaving Bitcoin without strong risk-on sponsorship.

- Correlations have shifted: Bitcoin is no longer tightly linked to tech stocks and has recently shown negative correlation with gold.

- A dovish turn by the Federal Reserve—potentially catalyzed by softer PCE data—could restore momentum, but internal demand dynamics remain a constraint.

Introduction: A Market That Moved On Without Bitcoin

In late 2025, global markets delivered a paradox that few crypto-native investors expected. While Bitcoin—the asset often branded as “digital gold”—remained roughly 30% below its peak, traditional safe havens surged to new records. Gold climbed toward $4,500 per ounce, silver briefly touched $71.49 per ounce, and major equity indices hovered near all-time highs, supported by artificial intelligence–led growth narratives.

According to on-chain analytics firm CryptoQuant, Bitcoin’s underperformance is not a coincidence nor a simple macro anomaly. Instead, it reflects a complex interaction of whale-driven selling pressure, ETF outflows, and a weakening internal demand structure that has left Bitcoin stranded between risk-on and risk-off regimes.

This article synthesizes CryptoQuant’s analysis with broader market data reported by Reuters and recent macro commentary. It aims to clarify why Bitcoin is lagging, how this divergence developed, and what conditions might reverse it—with a focus on actionable insights for investors and blockchain practitioners seeking the next opportunity.

Gold and Silver Surge While Bitcoin Stalls

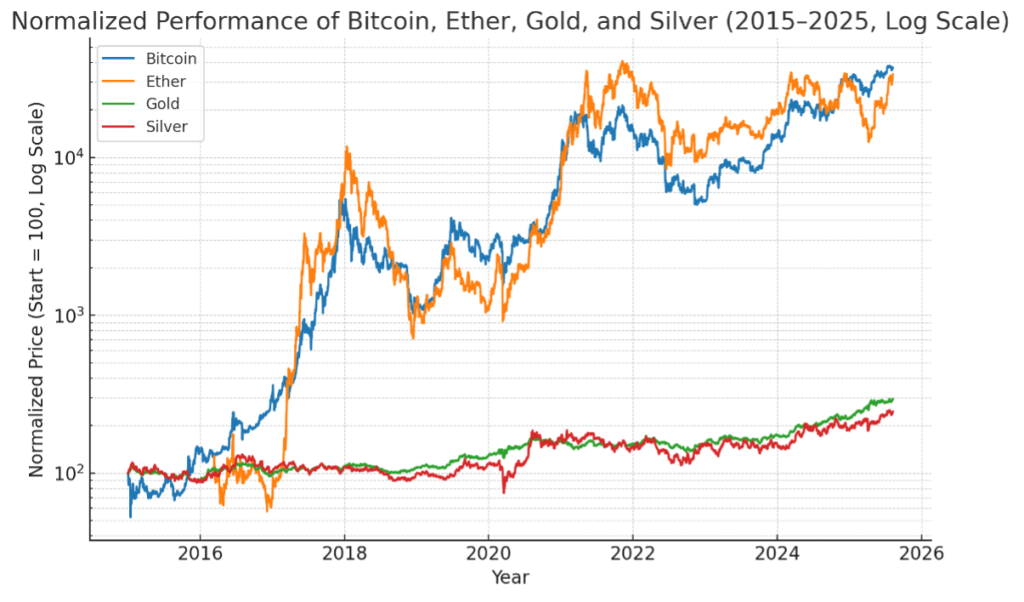

Gold and silver have delivered one of their strongest rallies in decades. Spot silver reached $71.49 per ounce, rising 147% year-to-date, while gold touched $4,497.55 per ounce, up roughly 70% since the beginning of the year. Market participants point to a confluence of forces: persistent supply deficits, rising industrial demand (especially for silver), central bank accumulation, geopolitical risk, and expectations of lower real yields amid prospective U.S. rate cuts.

By contrast, Bitcoin has failed to capitalize on the same tailwinds. Historically, Bitcoin often benefited from dollar weakness and accommodative monetary policy expectations. Yet in this cycle, capital has bypassed BTC and flowed instead into physical commodities and AI-heavy equity indices.

[Comparative performance of Bitcoin vs. Gold vs. Silver (YTD, indexed to 100)]

Whale Selling Pressure and ETF Outflows

CryptoQuant identifies persistent selling by large holders as a primary drag on Bitcoin’s price action. Since October, so-called “whales” have steadily reduced exposure, exerting continuous overhead supply. At the same time, Bitcoin ETFs have seen net outflows totaling approximately $5.1 billion from peak levels, signaling diminished institutional appetite at current prices.

This combination is particularly damaging in a market that lacks strong incremental demand. Unlike gold—where central banks act as long-term, price-insensitive buyers—Bitcoin’s marginal demand remains more tactical and positioning-driven.

The result is a market structure in which every rally encounters distribution, preventing sustained upside momentum.

A Breakdown in Correlations: Bitcoin on Its Own

One of the most striking findings in CryptoQuant’s report is the breakdown of historical correlations. Around August, Bitcoin’s correlation with the Nasdaq began to weaken. By July, its correlation with gold turned negative. In practical terms, Bitcoin is currently behaving as neither a technology proxy nor a conventional safe haven.

[Rolling correlation of Bitcoin with Nasdaq and Gold]

This “correlation vacuum” leaves Bitcoin vulnerable. In risk-off environments, capital first seeks gold and government bonds. In risk-on phases, it chases growth equities—particularly those tied to AI productivity gains. Bitcoin, positioned awkwardly between these poles, struggles to attract decisive inflows.

On-Chain Demand Weakness: The Internal Constraint

Beyond external macro forces, Bitcoin faces an internal demand problem. CryptoQuant’s data show that apparent demand has recently turned negative, even as prices remain elevated. Short-term holder SOPR (Spent Output Profit Ratio) has spent extended periods below 1.0, indicating that recent buyers are exiting at losses or near break-even.

This behavior amplifies selling pressure during rebounds, as underwater holders use price strength to exit positions. Until new demand expands meaningfully, this feedback loop remains a structural headwind.

Macro Policy as a Potential Catalyst

Despite the bleak near-term picture, CryptoQuant notes a possible inflection point. If upcoming PCE inflation data undershoot expectations, markets may price in a more dovish stance from the Federal Reserve. Historically, such shifts have benefited Bitcoin by weakening the dollar and compressing real yields.

However, unlike previous cycles, a dovish pivot alone may not be sufficient. Without renewed ETF inflows or a resurgence in on-chain demand, Bitcoin’s response could be muted relative to gold and equities.

What This Means for Crypto Investors and Builders

For investors searching for new crypto assets or yield opportunities, Bitcoin’s stagnation may redirect attention toward:

- Altcoins with clear cash-flow or utility narratives

- Tokenized real-world assets (RWA) that bridge traditional safe-haven demand with blockchain rails

- Infrastructure projects aligned with institutional adoption, compliance, and settlement efficiency

For builders, the lesson is equally clear: narratives matter, but sustainable demand structures matter more. Assets that can demonstrate persistent, non-speculative usage are more likely to attract capital in a market increasingly sensitive to macro uncertainty.

Conclusion: A Pause, Not an End

Bitcoin’s divergence from gold and silver in 2025 reflects more than temporary market noise. It exposes a structural tension between Bitcoin’s evolving identity and investors’ shifting preferences. While whale selling, ETF outflows, and weak on-chain demand have suppressed price performance, these same pressures could set the stage for a healthier reset—provided new demand emerges.

For now, Bitcoin remains in a waiting game. The next decisive move will likely depend not only on macro policy, but on whether Bitcoin can once again convince capital that it belongs in both risk-on and risk-off portfolios.