Main Points :

- Jack Dorsey’s recent statement “Bitcoin is not crypto” reignites debate about the identity and role of Bitcoin (BTC).

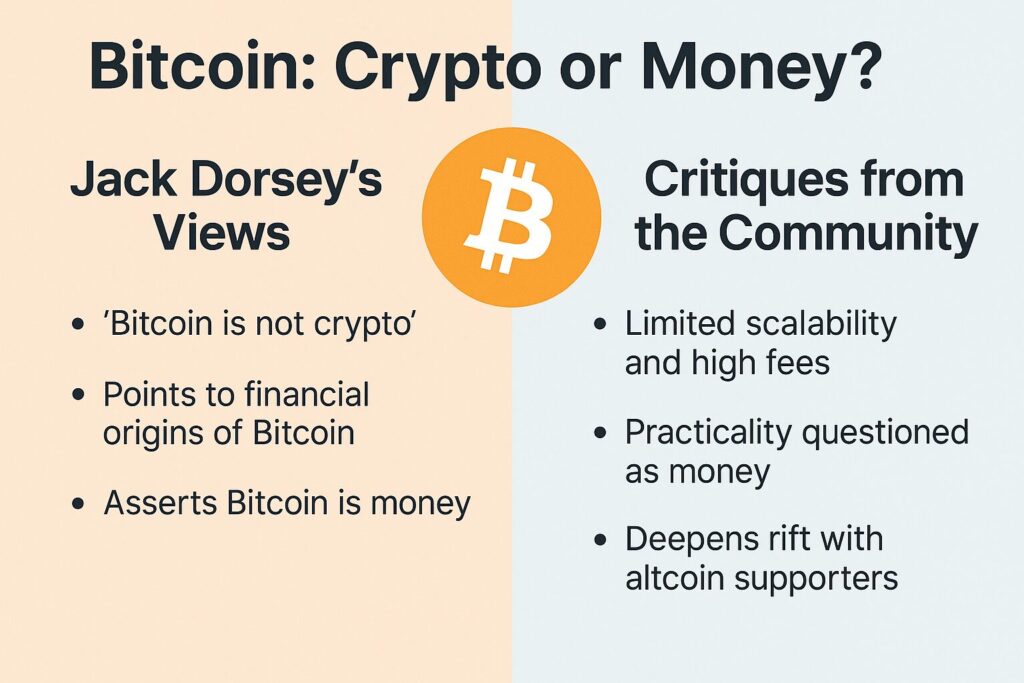

- Dorsey argues that the original white paper did not use the term “crypto” and that Bitcoin should be defined as money (or a payment system) rather than just part of the “crypto” ecosystem.

- His ecosystem (Block, Inc. / Square, Inc.) is moving to enable zero‐fee Bitcoin payments and promote everyday use of Bitcoin, as opposed to purely speculative investment.

- The crypto community pushed back: critics say Bitcoin’s scalability, fee structure and current use case limit its ability to function as “money” in the traditional sense.

- For builders and investors exploring new digital‐asset opportunities or practical blockchain uses, the Dorsey narrative invites a reassessment: differentiate between “money/settlement layer” use cases (Bitcoin) and “programmable asset / application layer” use cases (other chains, tokens).

- Recent developments (tax policy proposals, payment rails, wallet infrastructure) show acceleration in the payments narrative for Bitcoin and for digital assets more broadly.

Satoshi’s Vision and Dorsey’s Interpretation

In October 2025, Jack Dorsey — long‐time Bitcoin advocate and former co-founder of X (formerly Twitter) — penned a pithy message on X:

“bitcoin is not crypto”

Just an hour earlier he had written:

“bitcoin is money”

Dorsey’s core argument: when you read the original 2008 white-paper by Satoshi Nakamoto, the term “crypto” appears never. Instead the document describes Bitcoin as a “purely peer-to-peer version of electronic cash” and “an electronic payment system based on cryptographic proof instead of trust.”

By drawing attention to the absence of “crypto” in the foundational document, Dorsey asserts that Bitcoin’s true identity is as digital cash/money — not just one among many speculative cryptographic tokens.

Translated into practical terms: for Dorsey, Bitcoin’s value proposition lies in payments, settlement, and money-transfer, not just in being a “token” to trade. He views the conflation of Bitcoin with “crypto” (as in altcoins, DeFi tokens, utility tokens) as inaccurate and misleading.

Why This Matters for Builders and Investors

Differentiating Layers and Function

If you are exploring new digital assets or designing blockchain‐based solutions, Dorsey’s framing can serve as a useful heuristic:

- Settlement/Money Layer: Bitcoin – fixed supply, broad network effects, minimal programmability, designed as digital cash.

- Application/Utility Layer: Smart‐contract platforms, programmable tokens, DeFi, NFTs — assets and protocols built on top of or alongside settlement layers.

By separating these layers, you can evaluate where your interest lies: Are you investing in or building a money/settlement system (e.g., global payments, remittances, micropayments)? Or are you building or investing in programmable asset/application systems (e.g., tokenisation, DeFi protocols, cross-chain bridges)?

For Investors Seeking Next Income Streams

- If you believe blockchain adoption will surge via payments and consumption rather than purely speculative trading, then protocols enabling low-cost, high-frequency payments may be relevant (including Bitcoin’s Lightning Network, merchant acceptance infrastructure).

- Dorsey’s emphasis on zero-fee Bitcoin payments (via Square/Block) underscores the business model potential of payment‐rails rather than mere ‘hold and hope’ strategies.

- On the other hand, many altcoin ecosystems continue to emphasise programmability and application growth (which may yield additional revenue streams via fees, token issuance, ecosystem incentives). So the investment thesis may diverge depending on which “layer” one focuses on.

- For builders: if you lean toward real-world utility (retail payments, point-of-sale systems, micropayments) rather than speculative tokens, aligning with the “money” narrative could be a differentiator.

Infrastructure and Payments: What’s Happening Now

Zero-Fee Bitcoin Payments and Merchant Adoption

Dorsey’s company Block (via Square) has announced plans to enable merchant acceptance of Bitcoin payments with zero fees for a period, starting November 2025.

By offering no‐fee Bitcoin processing, the intent is to lower friction for businesses and boost Bitcoin’s role as a payment method, not just an investment. Dorsey projects full zero‐fee acceptance by 2026.

Tax and Regulatory Moves

In a parallel development, Dorsey has called for a de minimis tax exemption in the U.S. for “everyday” Bitcoin transactions (e.g., under $300) to foster peer-to-peer payments.

This is significant for two reasons:

- Tax friction is one major barrier to treating Bitcoin as money (if every small payment triggers capital gains, the usage model suffers).

- Should regulatory regimes ease for small payments, Bitcoin’s “money” use case becomes more practical and viable.

Community Challenges and Criticisms

Not everyone agrees with the payments‐first narrative. Some critics argue:

- Bitcoin’s scalability, high fees (in some contexts), and relatively slow block times hinder its use as a widespread payments platform.

- Others note that many users hold Bitcoin as a store of value, a “digital gold”, rather than spend it.

- Figures like David Schwartz (CTO of Ripple) have commented that Dorsey’s phrasing is more about ideology than technical change — highlighting that Bitcoin is cryptography + currency, and that simply separating “crypto” lexically may not affect real-world adoption.

Thus, if you are working on blockchain applications, it’s important to recognise that the payments narrative (Bitcoin as money) is one side; the programmability and application layer remains vibrant and may offer different growth vectors.

Implications for Blockchain Use Cases and New Assets

Real-World Utility vs Speculation

For professionals interested in practical blockchain use, Dorsey’s message invites a shift: focus less on speculative token price jumps and more on transaction flows, merchant adoption, and network usage. If Bitcoin becomes a viable payments rail (zero fees + global P2P), then infrastructure, merchant tools, wallet integrations, Lightning Network routing, micropayment gateways become areas to build or invest in.

On the flip side, smart-contract platforms and newer chains continue to explore programmable money, tokenisation of assets, DeFi, and Web3 applications — but these may imply higher risk (project viability, governance, token economics) and different thesis (not payments counts, but application usage counts).

New Asset Discovery: What to Look For

If you’re scouting new digital asset opportunities or building solutions, consider:

- Does the asset/protocol target settlement, global payments or money-transfer (a la Bitcoin) or is it an application layer token (DeFi, NFTs, gamefi, cross-chain)?

- What is the network effect and adoption pathway? For payments, merchant acceptance, regulatory clarity, low fees matter.

- How is the token economics structured? For application tokens, utility, staking, ecosystem incentives may matter more than just ‘store of value’.

- What is the infrastructure maturity (wallets, rails, user experience)? Dorsey’s emphasis on merchant tools suggests physical/retail presence is still under-explored.

- What regulatory or tax hurdles exist for everyday usage versus speculation? As we see in the Bitcoin tax exemption discussion, regulatory design can shape utility.

Summary and Outlook

Jack Dorsey’s assertion that “Bitcoin is not crypto” may seem semantic, but for builders and investors it signals a strategic framing shift: treat Bitcoin as money/payment rail, distinct from the broader “crypto token” ecosystem. For those interested in next-generation revenue streams and practical blockchain use, this means placing stronger emphasis on real payment flows, low-friction merchant adoption, and settlement infrastructure — not just speculative token gains.

At the same time, the broader digital-asset space continues to evolve with smart-contract platforms, DeFi and application layer models growing rapidly. The takeaway is not to ignore those, but to be clear: assets and protocols may belong to distinct categories (money vs application). Understanding which bucket you’re building/investing in matters.

Looking ahead, if Bitcoin’s payments narrative gains traction (zero fees, tax-exempt small payments, global merchant adoption) then infrastructure investments — wallets, payment processors, Lightning routing, point-of-sale integrations — could offer early‐mover advantages. For those looking at altcoins, smart-contract tokens, interoperability layers, the narrative remains vibrant but perhaps more crowded and speculative.

In closing: whether Bitcoin becomes the global digital money or remains primarily a store-of‐value asset, the debate stirred by Dorsey underscores the importance of use-case clarity, layer differentiation, and bridging the gap between speculation and real-world utility. For professionals keen on blockchain as a practical tool or revenue source, aligning your thesis with either the settlement layer or the application layer (or both) will help position for the coming phases of the industry’s evolution.