Main Points :

- Bitcoin is increasingly debated as a potential component of retirement portfolios, particularly 401(k) plans in the United States.

- Bitwise CIO Matt Hougan argues that Bitcoin’s volatility is often overstated when compared to familiar assets such as NVIDIA stock.

- Political resistance, led by figures such as Elizabeth Warren, centers on investor protection, fees, and market stability.

- Regulatory posture has shifted toward neutrality following executive action under President Trump, reopening the debate on alternative assets in retirement plans.

- For investors seeking new income sources and practical blockchain exposure, Bitcoin’s role should be assessed through risk-adjusted returns and portfolio construction—not fear-driven narratives.

1. The Growing Controversy Around Bitcoin and Retirement Savings

The question of whether Bitcoin belongs in retirement portfolios has moved from a fringe discussion to a mainstream policy debate. In early 2026, this issue resurfaced sharply when Bitwise Asset Management’s Chief Investment Officer, Matt Hougan, publicly rejected claims that Bitcoin is inherently unsuitable for 401(k) retirement plans.

His comments came on the same day that U.S. Senator Elizabeth Warren submitted a formal letter to the U.S. Securities and Exchange Commission, urging stronger safeguards—or outright restrictions—on cryptocurrency exposure within defined-contribution retirement accounts.

At the core of this debate is a single word: volatility. Critics argue that Bitcoin’s price fluctuations make it incompatible with long-term retirement security. Proponents counter that volatility, when viewed in isolation, is a misleading metric—especially in a financial system that already allows highly volatile equities in retirement portfolios without controversy.

2. Bitcoin vs. NVIDIA: Reframing the Volatility Argument

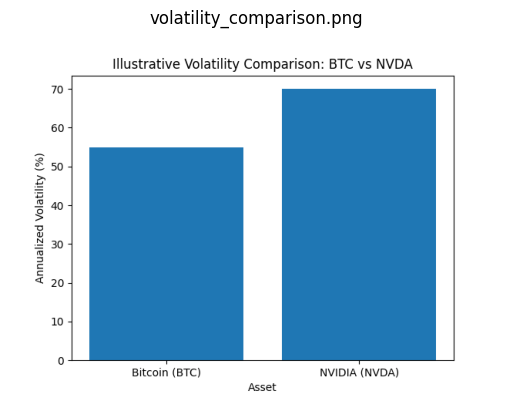

Hougan’s most striking rebuttal was a direct comparison between Bitcoin and NVIDIA, one of the most widely held and celebrated stocks in U.S. retirement plans.

According to Hougan, over the previous 12 months Bitcoin’s price volatility was lower than that of NVIDIA stock. Yet, no serious policymaker has proposed banning NVIDIA from 401(k) plans. This inconsistency, he argues, exposes a double standard rooted more in unfamiliarity than in objective risk analysis.

[Volatility Comparison Chart]

Note: This chart is illustrative and intended to demonstrate relative volatility concepts rather than precise historical data.

Volatility is not inherently negative. In finance, it is inseparable from return potential. High-growth equities, emerging market stocks, and thematic ETFs all exhibit volatility—yet they are routinely included in retirement portfolios as part of diversified allocation strategies.

Bitcoin, Hougan argues, deserves to be evaluated under the same framework.

3. Political Opposition and Investor Protection Concerns

Senator Elizabeth Warren has long positioned herself as a critic of the cryptocurrency industry. In her January 9 public letter, she warned that allowing crypto exposure in retirement accounts could expose workers to:

- Excessive and opaque fees

- Market manipulation

- Sudden and severe price collapses

Her position reflects a broader concern that retirement savings—often the primary financial safety net for American workers—should not be used for what she characterizes as speculative bets.

This framing resonates politically, particularly among regulators tasked with protecting less financially sophisticated participants. However, critics of Warren’s stance argue that it underestimates both investor agency and the existing risk already embedded in retirement systems.

4. Regulatory Shift: From Hostility to Neutrality

The regulatory environment surrounding crypto in retirement plans has evolved significantly since 2022. That year, the U.S. Department of Labor issued guidance strongly discouraging fiduciaries from offering cryptocurrency options in 401(k) plans.

In August of the previous year, President Trump signed an executive order instructing the Department of Labor to reassess restrictions on alternative assets in defined-contribution plans. As a result, the Employee Benefits Security Administration withdrew its earlier guidance and adopted a more neutral posture.

This shift does not mandate the inclusion of Bitcoin—but it removes the chilling effect that had discouraged plan providers from even exploring the option.

The change reopened the door for market-driven experimentation rather than blanket prohibition.

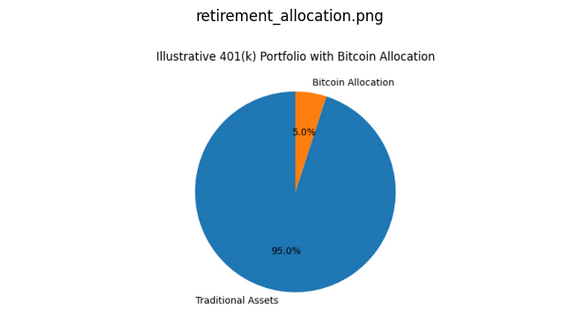

5. Current Access: Limited but Expanding

Despite the heated debate, actual access to Bitcoin within retirement accounts remains limited.

Most U.S. workers can only gain exposure through self-directed brokerage windows, where investment decisions are entirely the individual’s responsibility. Only a small number of providers currently offer Bitcoin exposure through spot Bitcoin ETFs.

Notable participants include firms like Fidelity Investments, while major incumbents such as Vanguard have chosen to stay on the sidelines.

[Illustrative 401(k) Allocation Model]

This cautious adoption reflects both regulatory uncertainty and reputational risk rather than a lack of investor interest.

6. Risk, Return, and Portfolio Construction

For investors seeking new revenue streams and practical blockchain exposure, the real question is not whether Bitcoin is risky—but whether it improves portfolio outcomes.

Multiple academic and industry studies have shown that small Bitcoin allocations (typically 1–5%) can improve a portfolio’s risk-adjusted returns due to Bitcoin’s low long-term correlation with traditional assets.

In this context, Bitcoin functions less like a speculative gamble and more like an asymmetric return instrument—limited downside at small allocations, with significant upside potential.

This is the same logic that underpins allocations to venture capital, emerging markets, and thematic growth stocks within institutional portfolios.

7. Practical Implications for Blockchain-Oriented Investors

For readers interested in the practical use of blockchain, the retirement debate has broader implications. Institutional acceptance via retirement systems accelerates:

- Market liquidity

- Regulatory clarity

- Infrastructure maturity (custody, compliance, reporting)

Each of these developments directly benefits blockchain-based business models, from custody services to on-chain analytics and tokenized financial products.

The retirement debate is therefore not only about Bitcoin—but about whether blockchain assets are recognized as a legitimate part of the global financial system.

8. Conclusion: Moving Beyond Fear-Based Policy

The argument that Bitcoin should be excluded from retirement portfolios solely due to volatility does not withstand close scrutiny. Traditional markets already tolerate—and even celebrate—volatile assets when they are familiar and profitable.

As Matt Hougan argues, the debate should focus on education, disclosure, and appropriate allocation—not outright exclusion.

For investors searching for new digital assets, alternative income sources, and real-world blockchain applications, this policy shift represents a critical inflection point. Bitcoin’s role in retirement portfolios may remain limited in the near term, but the direction of travel is clear: integration through risk management, not prohibition.