Main Points :

- A US life insurer, Delaware Life Insurance, has introduced limited Bitcoin exposure into its annuity portfolio through a volatility-managed index.

- The exposure is indirect, delivered via iShares Bitcoin Trust ETF, avoiding direct custody of Bitcoin.

- Volatility is managed to approximately 12%, aligning Bitcoin exposure with insurance and pension risk frameworks.

- This move reflects a broader institutional shift where crypto is being embedded into regulated retirement and insurance products.

- Similar strategies are emerging globally, from Bitcoin-denominated insurance to balance-sheet Bitcoin reserves.

Introduction: From Speculative Asset to Pension Component

For more than a decade, Bitcoin has been viewed primarily as a speculative instrument—volatile, unregulated, and unsuitable for conservative financial products such as pensions and insurance. That perception is now changing. In a landmark development, Delaware Life Insurance, a US-based life insurer focused on retirement products, has integrated Bitcoin-linked exposure into its annuity offerings.

Rather than allowing direct Bitcoin ownership, the company has adopted a carefully structured, risk-managed approach that aligns with the strict capital preservation requirements of insurance products. This decision marks a significant inflection point: Bitcoin is no longer merely tolerated by institutions; it is being engineered into products designed for retirees.

Delaware Life’s Bitcoin-Linked Annuity: What Exactly Changed?

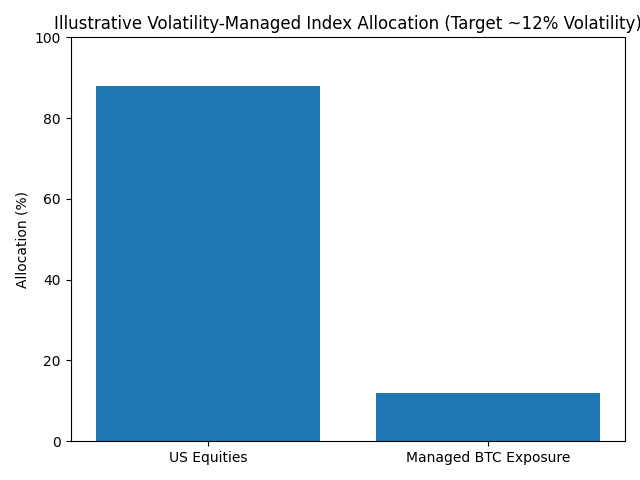

Delaware Life’s innovation lies not in offering a “Bitcoin annuity” per se, but in embedding Bitcoin exposure into a fixed indexed annuity framework. Fixed indexed annuities are insurance-based retirement products that protect principal while offering tax-deferred growth linked to a reference index.

The newly introduced index combines:

- US equities, and

- A small, tightly controlled Bitcoin allocation.

Crucially, the Bitcoin exposure is obtained through BlackRock’s spot Bitcoin ETF, iShares Bitcoin Trust ETF, ensuring:

- No direct Bitcoin custody by the insurer or policyholder

- Compliance with existing regulatory and operational standards

The insurer reports that the index is engineered to keep overall volatility around 12%, a level compatible with annuity risk profiles. This design allows policyholders to participate in Bitcoin’s upside potential while maintaining principal protection under annuity contract terms.

As of November 2025, Delaware Life reported cumulative annuity sales exceeding $40 billion, underscoring the scale at which this Bitcoin exposure could indirectly reach retail retirement savers.

How Volatility Management Makes Bitcoin “Insurable”

The core challenge in integrating Bitcoin into insurance products is volatility. Bitcoin’s historical annualized volatility often exceeds 60%, far beyond what insurance balance sheets can tolerate.

To address this, the index used by Delaware Life employs:

- Dynamic allocation between equities and Bitcoin

- Volatility targeting that automatically reduces Bitcoin exposure during high-volatility periods

- Rebalancing mechanisms designed to stabilize returns over time

This approach reframes Bitcoin not as a standalone asset, but as a return enhancer within a controlled risk envelope.

Institutional Gateways: BlackRock’s Role in Normalizing Bitcoin

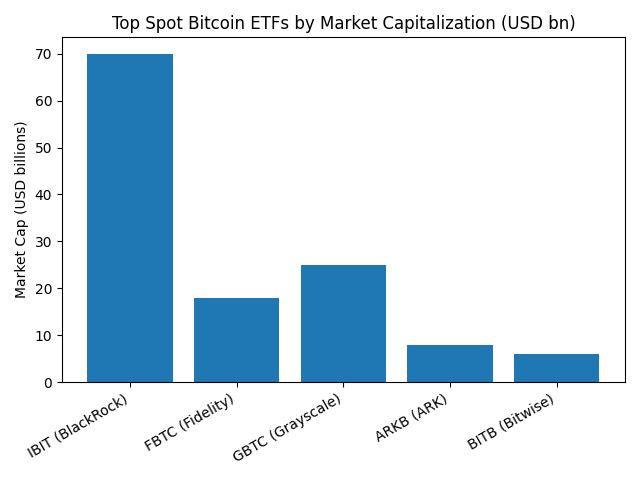

A key enabler of this development is BlackRock, the world’s largest asset manager. BlackRock’s launch of its spot Bitcoin ETF in January 2024 fundamentally altered institutional access to Bitcoin.

According to CoinMarketCap, BlackRock’s Bitcoin ETF has grown to a market capitalization exceeding $70 billion, making it the largest spot Bitcoin ETF globally.

In December 2025, BlackRock disclosed that the Bitcoin ETF ranked among its top three investment themes for the year. This endorsement carries immense signaling power for insurers, pension funds, and regulators worldwide.

For Delaware Life, BlackRock’s ETF provides:

- Institutional-grade custody and compliance

- Daily liquidity and transparent pricing

- Regulatory familiarity for insurance supervisors

Fixed Indexed Annuities: Why This Structure Matters

Fixed indexed annuities are uniquely suited to crypto integration because:

- Principal protection is embedded in the insurance contract

- Returns are linked to an index, not direct asset ownership

- Tax deferral enhances long-term compounding

From a policyholder’s perspective, Bitcoin exposure becomes:

- Indirect

- Regulated

- Bounded by predefined risk controls

This structure transforms Bitcoin from a volatile trading asset into a long-term portfolio component for retirement planning.

Beyond Delaware Life: A Broader Insurance Trend

Delaware Life is not alone. Other insurance players are exploring Bitcoin through different lenses.

Bitcoin-Denominated Insurance

The Meanwhile Group, backed by investors including Sam Altman and Gradient Ventures, launched Bitcoin-denominated life insurance products in 2023. In October 2025, the company raised $82 million to expand Bitcoin-based retirement and savings solutions.

Balance-Sheet Bitcoin Strategies

Barbados-based insurer Tabit has taken a different route, holding Bitcoin directly on its balance sheet. In March, Tabit raised $40 million worth of Bitcoin to fully back its regulatory reserves for USD-denominated insurance contracts.

These models illustrate two distinct institutional approaches:

- Bitcoin as a linked exposure (Delaware Life)

- Bitcoin as core capital (Tabit)

Policy Signals: Retirement Systems Catch Up

Regulatory and policy frameworks are also evolving. In August, US President Donald Trump signed an executive order directing regulators to expand access to cryptocurrencies within 401(k) retirement plans.

While implementation details remain under discussion, the policy signal is clear: crypto exposure is increasingly viewed as compatible with long-term retirement savings when properly structured.

Implications for Investors and Builders

For investors, Delaware Life’s move signals:

- Reduced stigma around Bitcoin in conservative portfolios

- Growing availability of “crypto-lite” products

- Potential demand for volatility-managed crypto indices

For blockchain builders and fintech operators, the implications are even broader:

- Demand for compliant crypto exposure vehicles will increase

- Infrastructure linking ETFs, indices, and insurance products will become strategic

- Volatility engineering and risk modeling will be core competencies

Conclusion: Bitcoin’s Quiet Institutional Breakthrough

Bitcoin’s inclusion in Delaware Life’s annuity portfolio may appear incremental, but its significance is profound. This is not about speculation—it is about integration. Bitcoin is being reshaped to fit the constraints of insurance, pensions, and regulation.

As volatility-managed exposure becomes standardized, Bitcoin’s role may evolve from an alternative asset into a structural component of long-term financial systems. For those seeking new digital assets, revenue opportunities, or practical blockchain applications, this development marks a critical turning point.