Main Points :

- Traditional diversification is weakening as equities and bonds move together

- The classic 60/40 portfolio is losing its effectiveness

- Bitcoin is showing independent price behavior

- Institutional demand signals (e.g., Coinbase Premium) suggest structural adoption

- Markets are entering a phase of “redefined diversification,” not reduced risk

Market Structure Shift (VIX vs Equity-Bond Correlation vs Bitcoin Behavior)

1. The Illusion of Stability: Why Low Volatility Is Misleading

At first glance, global financial markets in early 2026 appear calm. The CBOE Volatility Index—widely regarded as a barometer of investor fear—has retreated to levels seen before recent geopolitical tensions. On the surface, this suggests that risk has subsided and stability has returned.

However, this perception is dangerously incomplete.

Beneath the declining volatility lies a structural shift that carries far greater implications: the breakdown of diversification itself. Historically, investors have relied on the inverse relationship between equities and bonds to manage risk. When stocks fall, bonds typically rise, cushioning portfolio losses. This dynamic has been foundational to modern portfolio theory.

But that relationship is now weakening—and in some cases, reversing.

2. The Return of a “Non-Diversifying Market”

Recent data shows that equities and bonds are increasingly moving in the same direction. This positive correlation mirrors conditions last seen in 2022, when both asset classes declined simultaneously, catching traditional investors off guard.

This environment creates what can be described as a “non-diversifying market”—a regime in which spreading investments across asset classes no longer reduces risk effectively.

The implications are significant:

- Portfolio volatility increases despite diversification

- Drawdowns become more severe

- Risk management models based on historical correlations fail

In other words, investors are diversified in structure—but not in outcome.

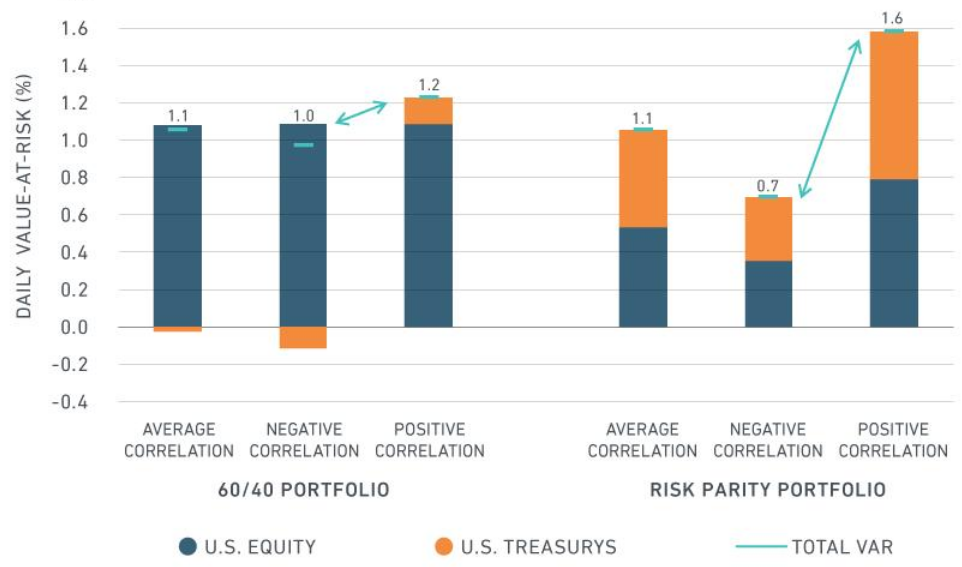

3. The Collapse of the 60/40 Portfolio Model

For decades, the 60/40 portfolio—allocating 60% to equities and 40% to bonds—has been the gold standard of asset allocation. Its success relied heavily on the negative correlation between these two asset classes.

But when that assumption breaks, so does the model.

In today’s environment:

- Rising inflation pressures both stocks and bonds

- Monetary tightening reduces liquidity across all markets

- Geopolitical fragmentation increases systemic risk

As a result, both equities and bonds can decline together, rendering the 60/40 model structurally fragile.

This is not just a temporary anomaly—it signals a deeper transition in how capital behaves across global markets.

Breakdown of 60/40 Portfolio Performance Under Positive Correlation

4. The Search for True Diversifiers

As traditional diversification fails, investors are forced to reconsider what qualifies as a “diversifying asset.”

Historically, gold and commodities have served this role. But in the modern financial system, a new contender has emerged: Bitcoin.

Bitcoin’s appeal lies not just in its returns—but in its behavior.

Unlike traditional assets, Bitcoin is not directly tied to:

- Corporate earnings

- Interest rate cycles

- Sovereign debt dynamics

Instead, its price is influenced by a combination of:

- Network adoption

- Liquidity cycles

- Regulatory developments

- Institutional flows

This independence is precisely what makes it attractive in a world where correlations are converging.

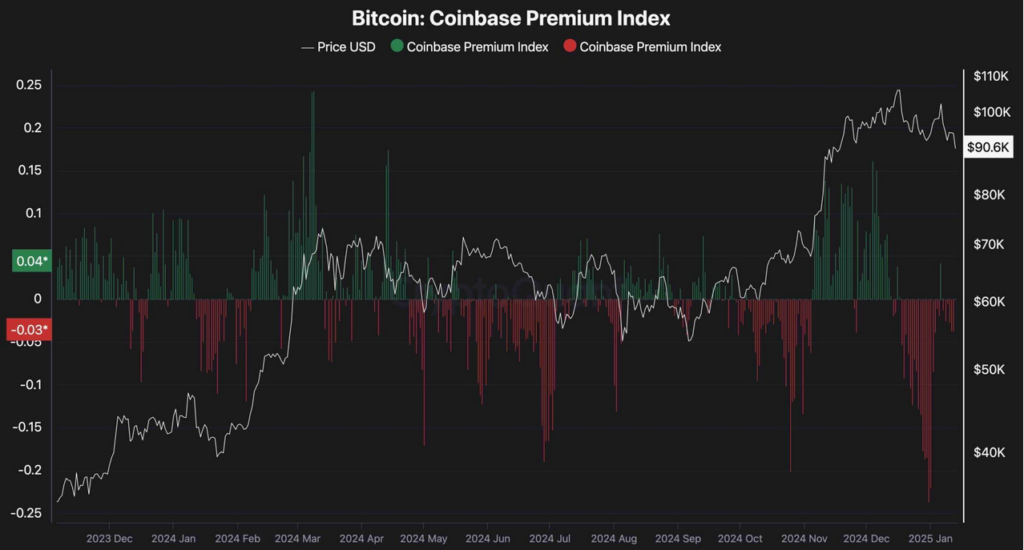

5. Bitcoin’s Unique Market Behavior: Evidence from On-Chain and Market Data

A closer look at market data reveals a compelling pattern.

Even as the VIX declines—suggesting reduced market stress—Bitcoin does not simply follow risk-on behavior. Instead, it often moves independently, maintaining its own trajectory.

This divergence is critical.

It indicates that Bitcoin is no longer behaving purely as a speculative risk asset. Instead, it is beginning to exhibit characteristics of a structural asset class.

Another key indicator is the Coinbase Premium Index, which measures the price difference between Bitcoin on U.S.-based Coinbase and global exchanges.

When this premium is positive:

- It suggests strong spot demand from U.S. investors

- It indicates institutional or high-net-worth accumulation

- It reflects long-term allocation rather than short-term trading

This pattern has been increasingly observed in recent months, reinforcing the idea that Bitcoin is being integrated into portfolios—not just traded.

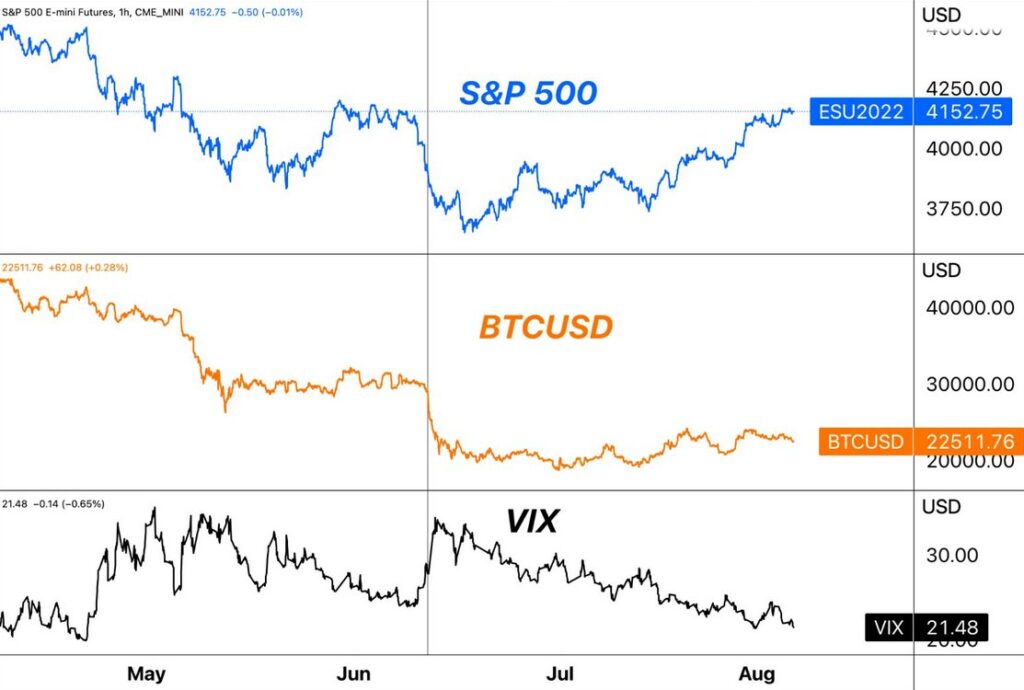

6. Decoupling from Traditional Risk Assets

Perhaps the most important observation is how Bitcoin behaves during periods of rising volatility.

Traditionally, when risk increases (i.e., VIX rises), risk assets decline. But Bitcoin does not always follow this pattern.

In some cases:

- Bitcoin remains stable while equities fall

- Bitcoin declines less than traditional risk assets

- Bitcoin even rises due to alternative demand drivers

This decoupling suggests that Bitcoin is influenced by a different set of forces—making it a candidate for true diversification.

Bitcoin vs Traditional Assets During Volatility Spikes

7. Institutional Adoption and Structural Repricing

The narrative around Bitcoin is evolving.

Once dismissed as a highly volatile speculative asset, it is now being reconsidered as part of strategic asset allocation.

Key drivers include:

- Institutional inflows via ETFs and regulated vehicles

- Increasing clarity in global crypto regulation

- Integration into payment and settlement systems

- Growing role in macro hedging strategies

Large financial institutions are no longer asking whether Bitcoin is investable—but how much exposure is appropriate.

This shift is subtle but profound.

8. Implications for Investors: Rethinking Portfolio Construction

For investors seeking new revenue opportunities and exposure to emerging technologies, the implications are clear:

- Diversification must be redefined

- Correlation—not just asset class—must be analyzed

- Alternative assets are no longer optional

Bitcoin, in this context, is not a replacement for traditional assets—but a complement that enhances portfolio efficiency.

A modern portfolio may look less like 60/40 and more like:

- Core traditional assets

- Alternative diversifiers (Bitcoin, commodities)

- Liquidity and optionality layers

9. The Bigger Picture: A Structural Shift in Global Finance

What we are witnessing is not merely a market cycle—but a transformation in the architecture of global finance.

Key trends include:

- Fragmentation of global capital flows

- Rise of digital assets as parallel financial infrastructure

- Declining effectiveness of legacy financial models

In this new paradigm, Bitcoin occupies a unique position:

- It is global yet decentralized

- It is scarce yet liquid

- It is volatile yet increasingly structured

Conclusion: Bitcoin as the New Axis of Diversification?

The current market environment should not be interpreted as a period of reduced risk—but as a phase of redefined diversification.

As traditional correlations break down, the need for truly independent assets becomes more urgent.

Bitcoin, with its distinct behavior and growing institutional adoption, is emerging as a serious candidate for this role.

The question is no longer whether Bitcoin is a risk asset.

The question is whether it can become the new axis around which diversification itself is built.

The answer is not yet definitive—but the validation process has already begun.