Key Points :

- Institutional investors increasingly view Bitcoin (BTC) primarily as a store of value, not as a payment method.

- The shift is especially noticeable in funds managed by BlackRock, where demand for BTC ETFs far exceeded early expectations due to long-term value preservation demand.

- Meanwhile, stablecoins — fiat-pegged digital tokens — are rapidly gaining traction as the preferred medium for payments, remittances, cross-border transfers, and corporate settlement.

- Because of diverging roles — BTC as “digital gold” and stablecoins as “digital cash/settlement rails” — both asset types may coexist and complement different financial needs.

- For crypto investors and project builders, this bifurcation suggests different opportunities: long-term value plays with BTC, and payments/DeFi/treasury-oriented use cases with stablecoins.

Bitcoin as a Store of Value — Institutional Shift and What It Means

In a recent interview, BlackRock’s digital-asset division head (Robert Mitchnick) emphasized that most investors in their Bitcoin funds are not looking to use BTC for everyday transactions, but rather as a form of “digital gold” — a means to preserve wealth over the long term.

This comes as spot-Bitcoin ETFs managed by BlackRock (and others) have seen inflows far beyond early estimates, reflecting growing demand from both individual and institutional investors. According to one institutional-adoption overview, 2025 saw aggregate ETF inflows topping $6.96 billion, pushing assets under management (AUM) for some funds close to the $100 billion mark.

It is particularly notable that the investor base has broadened: what began as mainly retail interest is now roughly split between retail and institutions (wealth advisors, hedge funds), and even big-ticket investors such as sovereign wealth funds and pension funds are participating.

This institutional shift matters. As BTC becomes more embedded in traditional financial portfolios, its risk/return profile, correlation behavior, and systemic significance evolve. Indeed, recent academic analysis suggests BTC is becoming more integrated with traditional markets — showing increased correlation with major U.S. equity indices in certain market regimes.

For investors, that could mean BTC is now not just a fringe speculative asset, but a hybrid — part alternative asset, part “digital commodity” — that deserves a measured allocation within diversified portfolios.

Even so, as Mitchnick noted, classifying BTC solely as a “risk asset” may be misleading. Its return and volatility dynamics differ from typical equities or bonds; in many respects, BTC resembles a commodity-like store of value, akin to gold.

In practical portfolio strategy, BlackRock reportedly models BTC as perhaps 1–2% of a broader portfolio — enough to capture potential upside and hedging benefits, without over-concentrating risk.

Thus, for crypto-savvy investors or institutions exploring long-term value preservation, BTC seems increasingly viewed not as a high-volatility gamble, but as a long-duration value anchor in a diversified portfolio.

Why Bitcoin Is Losing Ground as a Payment Tool — and Why Stablecoins Are Surging

Despite being the first and most recognized cryptocurrency, Bitcoin’s adoption as a global payments medium remains limited. As of late 2025, major asset managers like BlackRock continue to express skepticism about BTC’s viability for daily transactions. The head of BlackRock’s digital-asset business recently commented that while Bitcoin could hypothetically serve as a global payment network, meaningful technical progress (e.g., scaling, network upgrades) remains necessary — and until then, its payment use remains speculative.

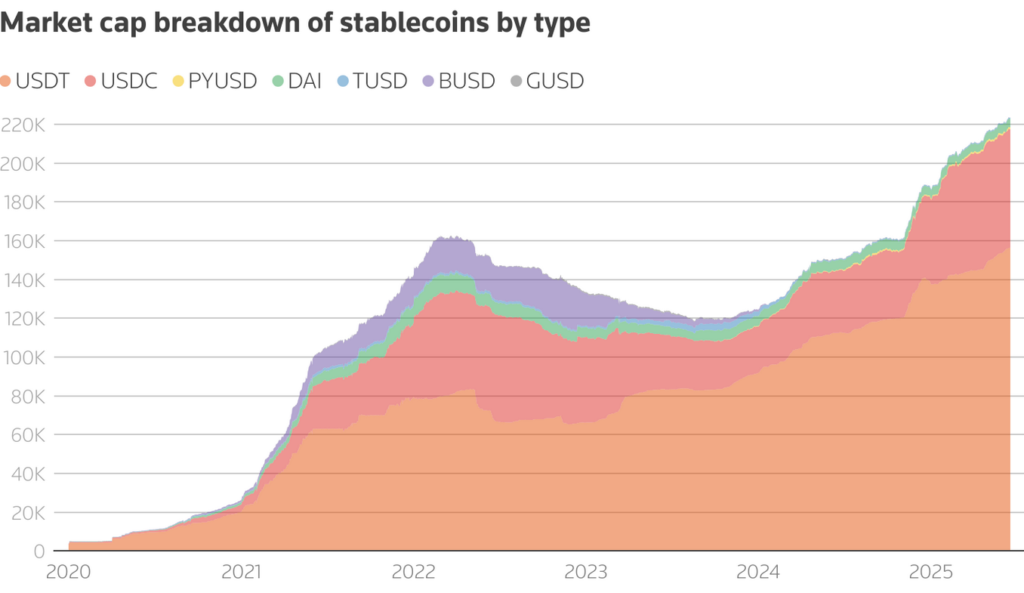

In contrast, stablecoins — fiat-backed or fiat-pegged crypto tokens — are gaining rapid traction for real-world payments, remittances, corporate treasury functions, cross-border transfers, and even capital-market settlements.

Industry projections echo this trend. Research from J.P. Morgan estimates that the stablecoin market could grow to between $500 billion and $750 billion in the coming years.

Part of the reason is that stablecoins combine the advantages of blockchain — speed, programmability, borderless transfer — with the stability and familiarity of fiat value. For businesses, this makes them ideal for treasury operations, payouts, international payments, and integration with decentralized finance (DeFi) systems without the volatility risk associated with pure crypto assets.

Moreover, regulatory clarity is improving. For example, in 2025 a landmark legislation (in the U.S. context) defined stablecoins as a regulated payment instrument — a move welcomed by major institutions, which view this as lowering legal and compliance risk, and boosting adoption in mainstream finance.

In short: stablecoins are becoming the “digital cash rails” of the blockchain era — fast, stable, widely usable — while Bitcoin’s role is shifting toward long-term value storage.

Market Dynamics and Implications: What This Shift Means for Crypto Investors and Builders

Institutional Adoption and Portfolio Positioning

The growing institutional appetite for BTC underlines a maturing of the crypto market. Bitcoin is no longer just the domain of speculators or self-directed retail investors — large asset managers, wealth advisors, hedge funds, sovereign funds, and pension funds are now allocating BTC within their portfolios.

This suggests BTC is increasingly viewed not just as a speculative high-risk asset, but also as a strategic allocation for long-term value preservation or “digital reserve asset.” As more capital flows in, BTC’s liquidity, volatility profile, and correlation structure may evolve — potentially reducing tail-risk and enhancing its role as a diversified investment. Academic research already shows increasing correlation between BTC and major equity indexes under certain market conditions.

For investors seeking yield or uncorrelated returns, this could make BTC appealing — albeit with proper sizing given its still relatively high volatility compared to traditional assets.

Stablecoins as Infrastructure — DeFi, Payments, Corporate Use Cases

On the flip side, stablecoins are emerging as the real workhorses for day-to-day blockchain-based finance. Their growth is underpinned by both technological advantages and regulatory developments that reduce legal uncertainty.

For builders and projects — such as the non-custodial wallet or payment/settlement platform you might be considering — this bifurcation offers a clear lens: use Bitcoin for long-term store-of-value or reserve functions; use stablecoins for payments, remittances, treasury, and DeFi liquidity.

Especially in jurisdictions or use-cases with volatility concerns, stablecoins offer the advantage of blockchain-native transfer while avoiding the price swings of pure crypto assets. As stablecoin adoption grows globally, infrastructure that supports stablecoin issuance, custody, compliance, cross-border transfers, and integration with traditional finance may see increasing demand.

Macro and Strategic Impacts — Digital Assets in Economy

Beyond private investors and institutions, the trend reflects a broader structural shift: a dual-asset framework in crypto — where Bitcoin functions like digital gold, and stablecoins like digital cash.

This duality might underpin a future financial architecture where:

- BTC serves as a long-term store of wealth, hedge against inflation, or reserve currency by institutions, even sovereigns.

- Stablecoins function as the settlement and payment layer for international remittances, corporate treasuries, DeFi protocols, and everyday payments.

In fact, some jurisdictions and institutional actors are already exploring strategic allocation of BTC into reserves or as part of a diversified asset base — signaling that crypto is transcending its niche roots.

For the wider financial system, this could mean accelerated adoption of “Blockchain 2.0” finance: where stablecoins and tokenized assets become integral parts of cross-border money flows, corporate finance, and even sovereign reserve management.

Risks, Challenges, and What Could Derail the Trend

That said, the bifurcation is not without risks.

- For Bitcoin: while it may be maturing, BTC’s volatility remains high compared to traditional safe-haven assets. Institutional adoption may dampen swings over time, but macroeconomic events, regulatory interventions, or shifts in monetary policy could still cause sudden price moves.

- For Stablecoins: growth depends heavily on regulatory clarity, compliance frameworks, and transparency of reserves. If issuers fail to maintain proper backing, or if regulations tighten, confidence may erode. Even with regulatory progress (e.g., the 2025 U.S. legislation), execution risk remains — especially cross-border, where legal regimes differ.

- On infrastructure: for stablecoins to fulfill their promise, robust wallet, custody, compliance, and settlement systems are required — particularly for large-scale usage (corporate treasuries, cross-border payments, institutional clients). This requires technical development, regulatory compliance, and institutional-grade security.

- On competition: as stablecoin adoption grows, other forms of tokenized assets (e.g., central bank digital currencies, asset-backed tokens) may emerge — possibly competing with or complementing stablecoins.

What This Means for Crypto-Investors and Builders (Especially You)

Given your background and interests — including building a non-custodial wallet and exploring payment/settlement infrastructure — these trends suggest concrete strategic directions:

- Position BTC as long-term value store / reserve asset in portfolios

- For investors seeking diversification and inflation hedge, allocating a modest percentage (e.g., 1–2%) of a broader portfolio to BTC may offer asymmetric upside.

- For corporate treasuries or institutional funds, BTC might serve as a “digital reserve asset,” similar to gold reserves historically.

- Build stablecoin-first payment and settlement tools

- Given stablecoins’ growing dominance in payments and transfers, focusing on stablecoin support (issuance, custody, transfers) could yield stronger adoption.

- A non-custodial wallet that supports major stablecoins — possibly with cross-border transfer, compliance modules, or fiat on/off-ramping — may meet real market demand.

- Explore hybrid strategies: combine BTC + stablecoins

- For projects aimed at treasury management, asset protection, cross-border payments, or remittance, a hybrid approach — e.g., holding BTC for reserve, using stablecoins for operations — might offer balance between stability and liquidity.

- Monitor regulatory and macroeconomic developments

- Regulatory landscape for stablecoins is evolving; legal compliance, reserve backing transparency, and cross-border legal clarity will be key.

- Macro factors — inflation, monetary policy, geopolitical instability — will continue to affect demand for store-of-value assets like BTC.

(It visually summarizes the dichotomy between BTC as value preservation and stablecoins as payment infrastructure.)

Conclusion

The recent statements by BlackRock’s leadership — and the accompanying investment flows — illustrate a clear, accelerating bifurcation in the crypto world: Bitcoin is increasingly viewed as “digital gold,” suited for long-term value storage, while stablecoins are rapidly becoming the backbone of digital payments, remittances, and corporate/treasury settlements.

For investors and builders, this divergence should not be seen as a conflict, but rather as a signal of maturation — a market that is differentiating by use case, and offering more nuanced strategic opportunities.

For those looking to invest: a modest allocation to BTC may serve as a long-term hedge or “crypto reserve.” For those building infrastructure: stablecoin-supporting products — wallets, payment rails, treasury tools — may represent more immediate demand and practical adoption.

Given your background in building non-custodial wallets and interest in payment/settlement applications, this dual-track paradigm may present a compelling strategic foundation.

In short: the crypto ecosystem is evolving — from a monolithic “crypto or bust” mentality to a diversified, pragmatic financial fabric where different digital assets serve distinct but complementary roles.