Key Takeaways :

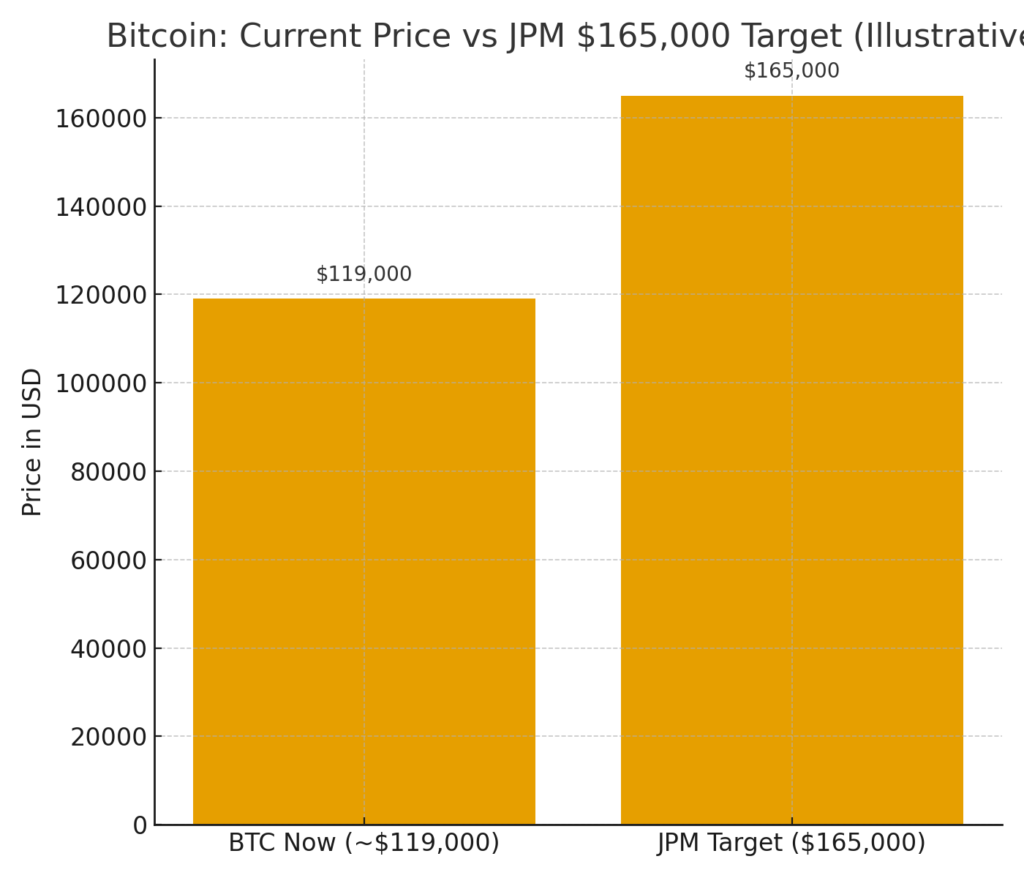

- JPMorgan projects that, on a volatility-adjusted basis relative to gold, Bitcoin could surge from ~$119,000 to ~$165,000 (≈ +40 %).

- The so-called “debasement trade” — hedging fiat currency devaluation via gold and Bitcoin — is driving rising retail inflows into ETFs.

- While institutional players engage via futures (especially CME), their momentum currently trails that of retail ETF flows.

- Bitcoin ETF flows have been extremely strong lately — adding billions in short windows, sometimes exceeding the BTC mined supply.

- Meanwhile, gold’s surge and renewed ETF inflows are narrowing the relative strength gap between gold and Bitcoin.

- Newer research suggests evolving roles for Bitcoin in diversified portfolios, via sentiment-aware allocation models and shifting correlation patterns with equity markets.

Introduction: Setting the Stage

JPMorgan’s recent forecast has stirred renewed excitement in the crypto space: based on a volatility-adjusted comparison with gold, the bank estimates that Bitcoin could reach $165,000 — roughly 40 % above its current price (~$119,000) as of the time of reporting. This is not a sweeping “fundamental valuation” in isolation, but rather a relative valuation rooted in the idea that Bitcoin remains undervalued vs. gold considering their risk profiles. The core narrative hinges on what JPMorgan calls the “debasement trade” — the idea that investors are increasingly seeking hedges against fiat currency depreciation via assets like gold and Bitcoin.

For readers interested in spotting the next crypto opportunity, understanding this thesis — plus how ETF flows, institutional vs. retail dynamics, and macro factors feed into it — is crucial. In what follows, I’ll break down JPMorgan’s argument, contrast it with recent data and counterpoints, and explore implications for practitioners, investors, and protocol builders alike.

1. JPMorgan’s Valuation Rationale: Bitcoin vs. Gold

JPMorgan’s analysts, led by Nikolaos Panigirtzoglou, base their forecast on a model that adjusts for volatility differences between Bitcoin and gold. They point out that:

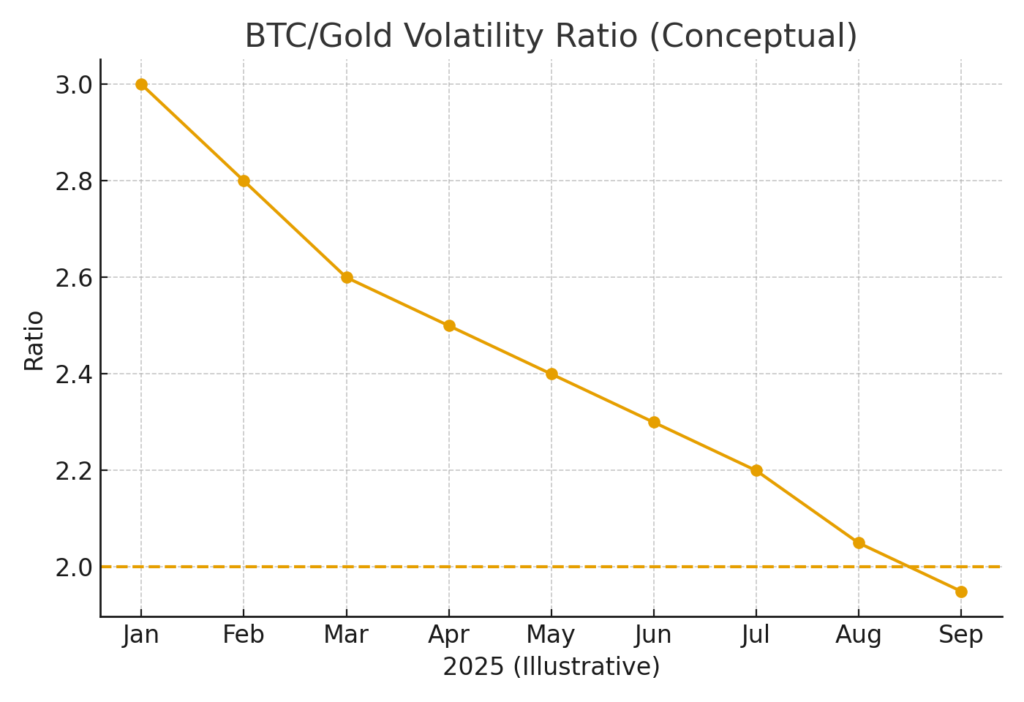

- The Bitcoin-to-gold volatility ratio has fallen below 2.0, meaning Bitcoin now “consumes” somewhat less incremental risk capital relative to gold than in past periods.

- To bring Bitcoin’s risk-adjusted market capitalization in line with the roughly $6 trillion private gold market (bars, ETFs, coins) would require Bitcoin to appreciate by ~42 % on a volatility-adjusted basis — i.e. the implied target of ~$165,000.

- At the end of 2024, their model saw Bitcoin as somewhat overvalued relative to gold; today it’s seen as undervalued by roughly $46,000 in that same framework.

Thus, their call isn’t built on macro forecasts of growth or adoption per se, but on the relative “arbitrage” potential between Bitcoin and gold when adjusted for volatility, scaled against gold’s known size in the real economy.

This doesn’t guarantee a move to $165,000 — it’s a statement of “if Bitcoin were priced like gold under current risk dynamics, this is where it would land.” But it gives a compelling anchor for optimism, especially in markets where gold is rallying hard.

2. The “Debasement Trade” and Retail Demand

One of the central pillars in the narrative is the idea that many investors now see gold and Bitcoin as inflation hedges or currency devaluation hedges — a wave JPMorgan labels the “debasement trade.” Under this thesis:

- Worries about government deficits, central bank independence, weakening fiat currencies (especially the USD), and political instability all fuel demand for “real assets.”

- In recent quarters, retail investors have led the charge into spot Bitcoin ETFs and gold ETFs. JPMorgan emphasizes that retail demand has outpaced institutional momentum, especially in ETF inflows beyond what futures-based institutional strategies are capturing.

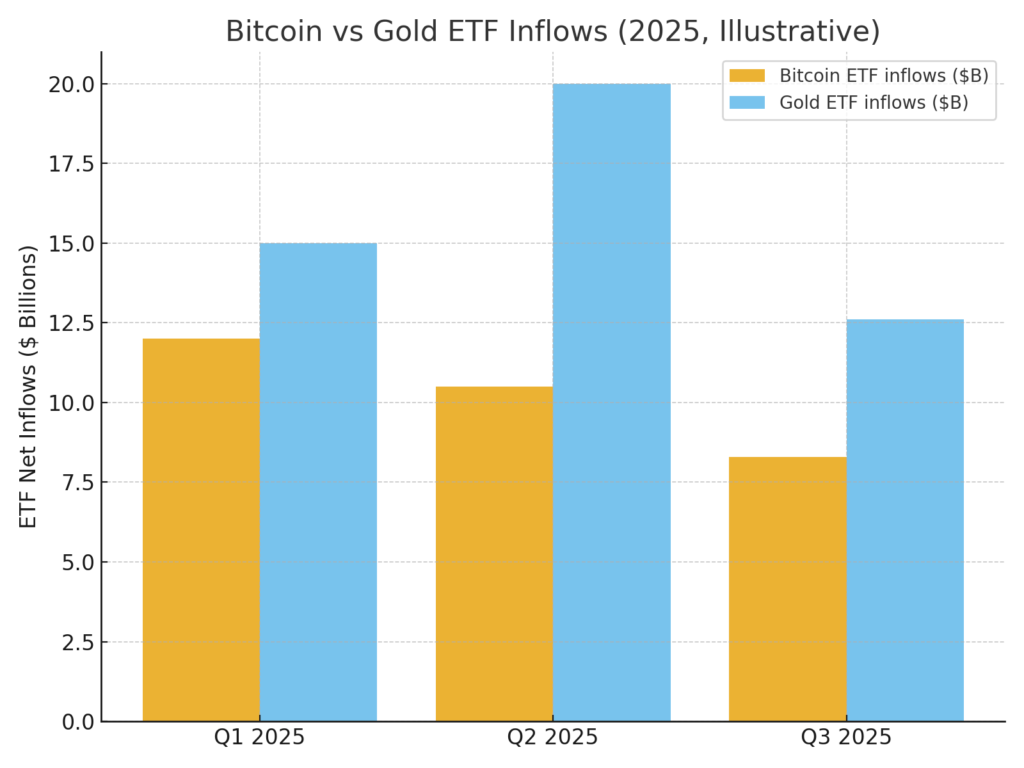

- In 2025, Bitcoin ETFs early in the year saw inflows surpass gold ETFs. But by August, gold ETF inflows sharpened, narrowing the gap.

- More recently, ETF flow data shows Gold ETPs took in ~$12.6 billion in Q3, while Bitcoin ETPs added ~$8.3 billion.

This suggests a tug-of-war: the same macro narrative driving gold demand is also benefiting Bitcoin — but timing, sentiment, and flow dynamics matter.

3. Institutional Players, Futures & Limitations

While JPMorgan’s narrative underscores retail ETF inflows, institutional participation is still important — albeit with different mechanics and perhaps slower pace. Key observations:

- Institutional capital tends to engage more through CME futures or derivatives rather than spot ETFs (especially in the U.S.), which constrains their direct footprint. JPMorgan notes that institutional momentum via futures is slower than retail ETF flows.

- An interesting metric: Bitcoin ETFs have recently added more BTC than is newly mined. Over a four-week span, U.S. spot Bitcoin ETFs added ~$3.96 billion, which, in quantity terms, implies removing ~112,000 BTC from float — about 2.7× the new issuance for a typical quarter.

- However, ETF flows explain only a modest share of daily BTC returns (R² ≈ 0.32) — meaning macro factors, derivatives, sentiment, and momentum also dominate.

- Institutions may wait for clearer regulatory clarity or deeper infrastructure before flooding in.

Thus, while institutional participation is rising, its pace and structure differ from the retail-driven ETF narrative that dominates JPMorgan’s upside case.

4. Gold’s Surge: A Tailwind or a Rival?

A key risk to JPMorgan’s argument is that gold itself has turned extremely strong lately, which both supports the inflation hedge narrative and competes for investor capital. Recent trends:

- Gold has broken record highs (e.g. over $3,800/oz) amid U.S. fiscal concerns, dollar weakness, and safe-haven demand.

- Global physically-backed gold ETFs attracted ~$5.5 billion in August alone, pushing year-to-date inflows to ~$47 billion.

- In 2025’s first half, gold ETFs drew ~$38 billion, the largest six-month inflow in ~5 years.

- Meanwhile, gold ETFs have outperformed Bitcoin ETFs year-to-date: e.g. SPDR Gold Shares (GLD) posted ~24.4 % YTD vs ~14.5 % for an iShares Bitcoin Trust ETF.

- Gold miner ETFs have also gone “parabolic” in 2025, with the VanEck GDX up ~123 % YTD.

Thus, gold’s strength is a double-edged sword: it corroborates the macro thesis but also competes for capital and could reduce Bitcoin’s relative appeal in some investors’ eyes.

5. Recent Flow & Price Trends in Bitcoin & ETFs

To assess whether JPMorgan’s projection is plausible, we should look at how recent flows and price behavior line up:

- Recently, U.S. spot Bitcoin ETFs added $1.63 billion in a single week; over four weeks, net flows totaled ~$3.96 billion (nine out of the past 12 weeks were positive).

- Year-to-date net inflows to Bitcoin ETFs stand at ~$22.78 billion; since inception, ~$58.4 billion.

- In Q3 2025, Gold ETPs took ~$12.6 billion while Bitcoin ETPs added ~$8.3 billion.

- In 2025, gold ETF gains have exceeded Bitcoin ETF gains (e.g. GLD vs IBIT).

- On the price front, Bitcoin has posted solid gains, aided by improved sentiment from gold’s rally.

These data points suggest that strong capital flows are already supporting upward Bitcoin pressure. If that continues or accelerates, reaching $165,000 becomes less speculative.

6. Emerging Research & Thematic Considerations

Beyond valuations and flows, a few newer angles are worth noting for those seeking the next frontier:

- A recent paper proposes a sentiment-aware mean-variance optimization strategy for crypto portfolios. By combining technical indicators (like RSI, SMA) with sentiment scores (via VADER / LLMs), one can potentially outperform simple Bitcoin or equal-weighted strategies — though drawdowns remain significant.

- Another study looks at changing correlation dynamics: as institutional adoption increases, Bitcoin’s correlations with equity indices (like Nasdaq, S&P) have intensified in some regimes, meaning Bitcoin may be less of an idiosyncratic “alt asset” and more integrated into macro risk cycles.

- On the on-chain / protocol side, if new layer-1 / layer-2s or alt tokens can capture narratives around inflation hedging, tokenization, or programmable finance, they may attract capital even beyond Bitcoin’s headline gains.

For practitioners, these emerging frameworks — sentiment-integrated allocation or treating Bitcoin as a partial macro beta instrument — should be on the radar.

Summary & Outlook

JPMorgan’s call that Bitcoin could reach ~$165,000 by year-end — on a volatility-adjusted comparison to gold — is bold and anchored in a clear narrative: Bitcoin remains undervalued versus gold, and the “debasement trade” could continue fueling inflows. But the path isn’t guaranteed.

Gold’s own rally adds both tailwinds and competition. Institutional flows remain slower and structured differently. But with Bitcoin ETF flows already outstripping BTC issuance in short windows, the dynamics are alive. Emerging research hints at deeper integration of sentiment, macro, and correlation into crypto portfolio strategies.

For readers hunting new cryptos or thinking about the next yield opportunities, the message is: don’t just treat Bitcoin as isolated crypto — view it as a macro-asset with flow dynamics and relational valuation (especially relative to gold and real assets). If you can spot where capital might flow next — whether into altcoins, tokenized real-world assets, or infrastructure protocols — you may ride the wave that follows Bitcoin’s next leg up (or reallocation).