Main Points :

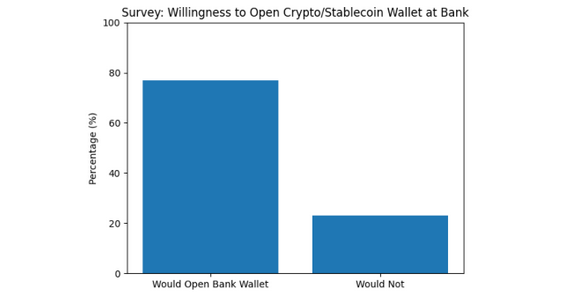

- 77% of surveyed stablecoin users say they would open a crypto or stablecoin wallet at their existing bank or fintech app if offered.

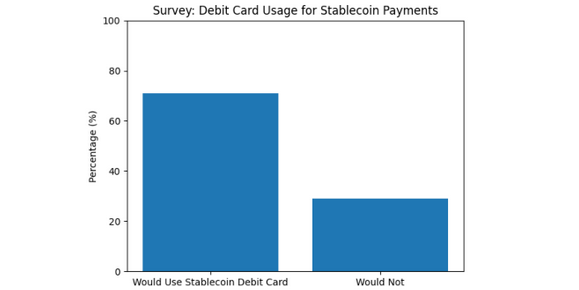

- 71% would use a debit card connected to stablecoin balances for payments.

- On average, users hold 35% of their annual income in stablecoins.

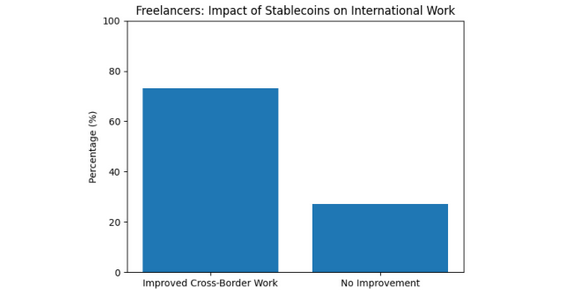

- 73% of freelancers and contractors say stablecoins improved cross-border client work.

- The convergence of banking and blockchain infrastructure is accelerating institutional adoption and reshaping payment rails.

A Structural Shift: Banks Reenter the Crypto Conversation

A recent survey commissioned by Coinbase and stablecoin infrastructure provider BVNK, covering 4,658 stablecoin users, reveals a significant structural insight: 77% of respondents would open a cryptocurrency or stablecoin wallet at their current bank or fintech app if such services were available.

This data point suggests something larger than simple curiosity. It reflects a maturation of digital asset adoption. Rather than abandoning traditional finance, most stablecoin users appear willing—even eager—to integrate their crypto activity into regulated banking environments.

[Bank Wallet Willingness]

The implication is profound. For years, crypto-native platforms positioned themselves as alternatives to banks. Today, users seem comfortable with a hybrid model: decentralized assets operating within regulated financial institutions.

For banks, this represents a tailwind rather than a threat. The narrative of disintermediation is shifting toward integration.

Stablecoins as Practical Financial Tools, Not Speculative Assets

Stablecoins—primarily pegged to $1—have evolved beyond trading instruments. They now function as:

- Cross-border settlement layers

- Payment rails for freelancers

- Corporate treasury diversification tools

- Inflation hedges in volatile economies

According to the survey, users hold on average 35% of their annual income in stablecoins. This is not a minor allocation. It signals trust in blockchain-based dollar equivalents as stores of value and mediums of exchange.

Unlike volatile assets such as Bitcoin or Ethereum, stablecoins offer price stability while preserving the advantages of blockchain:

- Near-instant settlement

- 24/7 availability

- Borderless transferability

- Programmability

From a capital allocation perspective, stablecoins are becoming operational liquidity instruments rather than speculative vehicles.

The Debit Card Bridge: Stablecoins Enter Daily Commerce

An even more striking statistic: 71% of respondents would use a debit card linked to stablecoin balances to make payments.

[Debit Card Usage]

This is the missing link between blockchain and retail adoption. While crypto trading is still niche relative to global banking, debit cards provide immediate usability.

Several fintech firms and exchanges already offer crypto-linked cards. The difference now is user appetite for bank-issued stablecoin debit cards. If regulated banks provide:

- Wallet custody

- On/off ramp services

- Card integration

- Compliance frameworks

Stablecoins may quietly integrate into everyday commerce.

This could mirror the early internet phase, where backend protocols evolved before consumer awareness caught up.

Freelancers and the Global Workforce: The Real Growth Engine

Perhaps the most practical use case emerges from freelancers and contractors. 73% report that stablecoins made working with overseas clients easier.

[Freelancer Impact]

In cross-border freelance markets, traditional wire transfers involve:

- Multi-day settlement

- High intermediary fees

- Currency conversion spreads

- Banking restrictions

Stablecoins, denominated in $ terms, eliminate most friction. Payment flows become:

Client → Stablecoin Transfer → Wallet → Local Off-ramp

This model compresses settlement from days to minutes and reduces cost structures significantly.

Given the rise of remote work platforms and digital nomad economies, stablecoins may represent the infrastructure layer for global human capital markets.

Why Banks Stand to Benefit

Rather than losing relevance, banks could gain:

- Deposit-like digital balances via stablecoin wallets

- Interchange revenue from card spending

- Custody and compliance fee income

- New cross-border settlement revenue streams

- Treasury efficiency via blockchain rails

In the United States and Europe, regulatory clarity around stablecoins is gradually forming. If stablecoin reserves are fully backed by U.S. Treasuries and cash equivalents, banks may even become custodians of those reserves.

This transforms stablecoins from “crypto experiments” into regulated monetary extensions.

Institutional Momentum and Macro Context

Recent years have seen:

- Spot Bitcoin ETF approvals

- Increasing institutional custody infrastructure

- Treasury allocation experiments

- Central bank research into digital currencies

Stablecoins already settle trillions of dollars annually on-chain. Their transaction volume often rivals or exceeds major card networks during peak crypto cycles.

For investors seeking new revenue streams, the real opportunity may not be speculative tokens but:

- Stablecoin infrastructure providers

- Compliance automation tools

- Cross-border payroll platforms

- Blockchain-based liquidity networks

In practical terms, the “picks and shovels” of the stablecoin economy may outperform pure token speculation.

Competitive Landscape: Banks vs Fintech vs Crypto-Native Platforms

The survey suggests users are not ideologically attached to decentralization. They prioritize:

- Trust

- Security

- Ease of use

- Regulatory clarity

If banks deliver seamless stablecoin integration, they may outcompete pure crypto exchanges for everyday financial usage.

However, fintech companies and crypto-native firms retain advantages:

- Faster product iteration

- Global-first mindset

- Developer ecosystems

- On-chain innovation speed

The next decade may produce a blended financial stack:

Bank compliance + Crypto rails + Fintech UX.

Risk Considerations

Despite optimism, risks remain:

- Regulatory fragmentation

- Stablecoin de-pegging events

- Custody vulnerabilities

- Over-reliance on single reserve assets

- AML/KYC burdens

For stablecoins to fully integrate into banking systems, risk management must evolve alongside innovation.

Strategic Outlook

For entrepreneurs and investors interested in:

- Blockchain’s practical applications

- Cross-border revenue optimization

- Digital payment infrastructure

- Yield generation in treasury management

Stablecoins may represent the most scalable and regulatory-aligned entry point.

The survey’s 77% figure is not just a statistic. It signals readiness for integration between traditional banking and blockchain-based dollar systems.

Conclusion

The narrative that crypto and banks are adversaries is becoming outdated. Survey data indicates that users prefer integration over replacement.

With 77% willing to open bank-issued crypto wallets, 71% ready to use stablecoin debit cards, and freelancers overwhelmingly benefiting from blockchain payments, stablecoins are no longer peripheral instruments.

They are evolving into core financial infrastructure.

For those seeking the next phase of blockchain monetization, the stablecoin-banking convergence may define the coming decade.