Main Points :

- JPMorgan Chase (JPM) under CEO Jamie Dimon is entering the stablecoin space, though with cautious acknowledgement of uncertainty.

- JPMorgan is already experimenting with a deposit-token (“JPMD”) on a public blockchain (Base, developed by Coinbase) and exploring joint stablecoin issuance with other banks.

- Beyond JPMorgan, major U.S. banks including Citigroup, Bank of America and others are stepping up their stablecoin strategies now that regulatory clarity is improving.

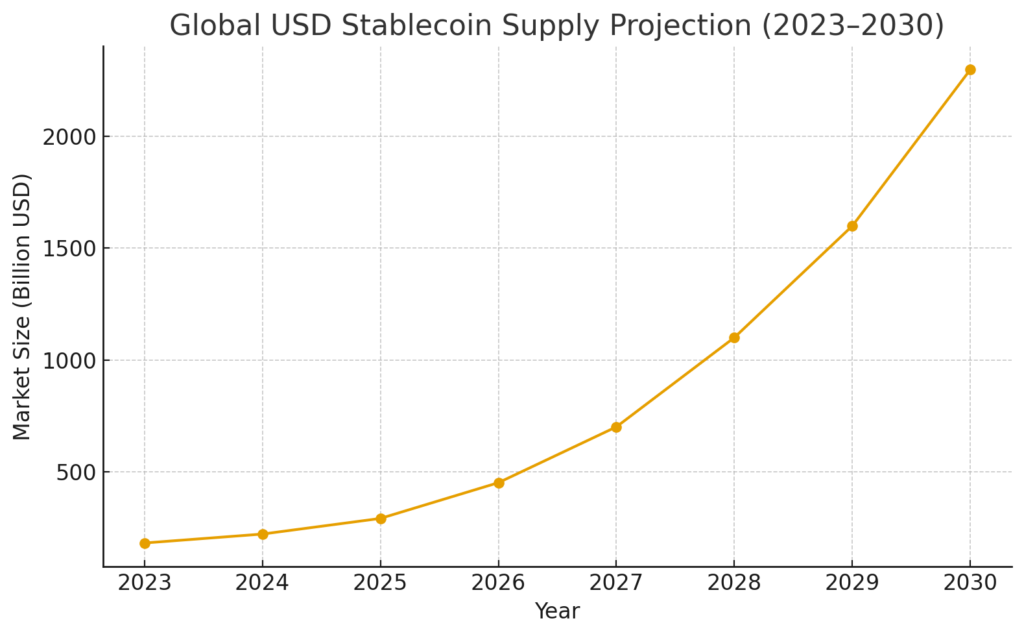

- The broader stablecoin market is already substantial — U.S. dollar-pegged stablecoins have a supply around US$290 billion — and this shift by large banks may herald growth to “trillions” of dollars in the coming years. (From the original article)

- For investors and practitioners in blockchain and new crypto assets, this institutional adoption of stablecoins and tokenised bank deposits signals a major infrastructure shift with opportunities in payments, settlement, tokenisation services, and new yield mechanisms.

1. JPMorgan’s Pragmatic Shift into Stablecoins

JPMorgan’s CEO Jamie Dimon recently remarked at the America Business Forum that while the future of stablecoins remains unclear, the bank prefers “playing to learn” rather than staying on the sidelines. He stressed that experimentation with smart contracts and blockchain tools is already under way at JPMorgan: “Any of these tools that you want to use for smart contracts, we are simply going to do … I don’t care what the budget says.”

Historically, Dimon has been critical or skeptical of cryptocurrencies such as Bitcoin, yet he now emphasises that frontier technologies must be engaged with regardless of personal opinion. JPMorgan has already launched a deposit-token (JPMD) on Base, allowing institutional clients to move dollars on-chain and earn interest.

For new crypto asset seekers, this indicates that even the most traditional of banking giants is evolving to incorporate digital-asset rails. For blockchain practitioners designing wallets, token issuance services, or settlement networks (such as your wallet project, “dzilla Wallet”), this trend underscores the growing importance of interoperability between legacy finance and decentralised rails.

2. From Internal Token to Inter-Bank Stablecoin Collaboration

While JPMorgan’s internal deposit token is a meaningful start, the more significant development lies in collaborative stablecoin issuance across major banks. According to Reuters, JPMorgan, Bank of America, Citigroup, and Wells Fargo are among the banks reportedly exploring a joint bank-stablecoin initiative.

Crypto Briefing reports that JPMorgan may build a stablecoin together with other banks—“We are building a stablecoin. We may build it with other banks.”

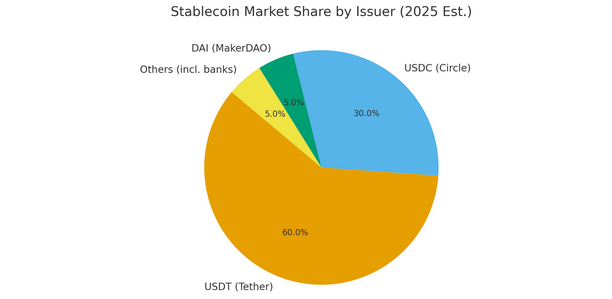

Such inter-bank efforts could set technical and regulatory standards for the next wave of digital assets: common rails, trust frameworks, and shared compliance infrastructure. For blockchain developers and token issuers, this means the likely emergence of “bank-grade” stablecoins that may sit between current token-native coins (like USDC or USDT) and central-bank digital currencies (CBDCs). This is a fertile space for innovation: wallet integration, liquidity routing, cross-chain settlement, programmable payments.

3. Regulatory Tailwinds and Market-Scale Implications

One of the big accelerants for bank stablecoin interest is improving regulatory clarity. In the U.S., legislation such as the GENIUS Act (recently passed) provides a clearer framework for stablecoin issuance by banks and financial institutions.

At the same time, the existing stablecoin market already commands nearly US$290 billion in USD-pegged supply alone (from the original article). Analysts anticipate multi-trillion dollar scale growth in coming years. For investors on the lookout for the “next income source,” this means stablecoins are evolving from niche crypto instruments to infrastructure-level assets.

From the academic side, recent research models (e.g., Wen & Lau, October 2025) show how fiat-backed stablecoins embedded in a regulated architecture can reduce systemic risk and improve monetary resilience. For those designing token systems or auditing EMI/VASP platforms (as your remit implies), this means risk modelling and system-design for stablecoin issuance are becoming vital.

4. Implications for Crypto Assets, DeFi and Tokenisation

4.1 New Revenue Streams & Payment Solutions

With banks entering stablecoins and deposit-tokens, the payment landscape is shifting. For example, faster settlement, programmable money (via smart contracts), and tokenised deposit rails mean new opportunities: tokenised debt issuance, real-time loyalty programmes, cross-border settlements with lower friction.

For your token presale or wallet project (dzilla Wallet), consider how integration with bank-token rails can become a differentiator: e.g., enabling users to hold interest-paying stable-tokens, pay with bank-issued programmable assets, or integrate KOL rewards tied to deposit-token usage.

4.2 Impact on Altcoins & New Assets

As banks standardise stablecoin issuance, it provides a stronger foundation for layered networks of tokenised assets. New crypto assets built on top of bank-issued stabletokens might gain traction: e.g., tokenised credit, real-world asset (RWA) tokens pegged to stablecoins, or cross-chain yield strategies involving bank-token liquidity.

For investors seeking the “next big thing,” one thesis might be: stablecoin rails + tokenised real-world assets = yield-generating ecosystems with institutional-grade backing. The banks’ involvement shifts the risk profile: increased trust, larger scale, potential for institutional productisation.

4.3 DeFi & Audit/Regulatory Considerations

Your audit framework for an EMI/VASP is directly relevant: bank-token issuance introduces compliance, KYC/AML, smart-contract risk, interoperability, and token redemption risk. Research shows that stablecoin runs and liquidity risks remain material concerns. DeFi platforms that support bank-tokens may benefit from lower risk profiles but also face higher regulatory scrutiny. For example, cross-chain redemption, multi-jurisdiction compliance, and deposit-token redemption certainty are key concerns.

5. Investor Perspective: What This Means for You

For readers hunting new crypto assets or designing blockchain applications, here are key takeaways:

- Infrastructure play: Bank stablecoins may become foundational rails. Early integrations (wallets, tokenisation platforms, payments) offer strategic advantage.

- Yield opportunities: Interest-paying deposit-tokens (like JPMD) may provide alternatives to crypto yield products, especially if issued by banks with regulatory backing.

- Tokenised real-world assets: As stablerails scale, tokenised assets (real-estate, debt, trade-finance) pegged to or interoperable with bank tokens may become investable.

- Risk-adjusted view: Bank-issuing tokens may carry lower counterparty risk relative to purely crypto native tokens, which may appeal to institutional or semi-institutional investors.

- Regulation as catalyst: With frameworks like the GENIUS Act, regulatory risk is diminishing (though not eliminated). Projects and tokens aligned with compliant infrastructure may benefit.

- Watch interoperability: Even if a bank token is launched, its utility depends on ecosystem adoption, partner banks, wallet support, redemption mechanics, and cross-chain connectivity. Without that, its value may be limited (analogous to commentary on JPMD).

6. Key Risks and Considerations

While the trend is positive for blockchain innovation and new assets, several risks merit attention:

- Regulatory uncertainty remains: Especially cross-border stablecoin issuance, redemption rights, and systemic-risk oversight.

- Adoption hurdle: A token issued by banks still needs ecosystem adoption: wallets, exchanges, merchants, tokenisation platforms. Until then, its liquidity/use case may be limited.

- Interoperability constraints: If only a subset of banks or chains support a given token, the “network effect” may not materialise.

- Asset/backing transparency: For stablecoins to function trust-worthily, full reserve backing, redemption guarantees, and auditability matter.

- Competition from CBDCs: Central bank digital currencies (CBDCs) may compete with private bank tokens, altering the “stablecoin” landscape.

- Technical & operational risks: Smart-contract vulnerabilities, key-management failings, cross-chain bridges, and settlement failures remain persistent hazards.

Conclusion

The announcement by JPMorgan’s Jamie Dimon and the broader moves by major banks to explore and collaborate on stablecoin issuance mark a pivotal moment for digital assets, blockchain infrastructure, and tokenisation. For investors and practitioners focused on new crypto assets, yield opportunities, and real-world blockchain applications, this shift signals that the stablecoin sector is no longer purely crypto-native—it is becoming mainstream finance.

For your wallet project (dzilla Wallet), your audit frameworks for EMI/VASP, and your token-issuance plans, this trend opens doors: bank-token integrations, programmable payment capabilities, tokenised real-world assets built on stable rails. At the same time, it underscores the importance of robust compliance, interoperability, ecosystem adoption, and risk management. The bridge between traditional finance and decentralised assets is expanding—and the next wave of innovation will ride that bridge.