Main Points:

- Major Asia-Pacific stock exchanges are pushing back against publicly listed companies whose primary business is accumulating cryptocurrencies as treasury assets.

- In Hong Kong Exchanges & Clearing Ltd. (HKEX)’s case, at least five firms seeking to pivot to digital-asset-treasury (DAT) models have been questioned; none have been approved so far.

- In India and Australia, listing authorities have set rules (e.g., cash-or‐short-term investment limits) that significantly constrain the crypto‐treasury model.

- Japan remains a relative exception in the region: its listed companies hold large cash reserves and crypto-treasury models are comparatively freer, though signs of regulatory friction are emerging (e.g., MSCI Inc. proposing to exclude firms with >50% holdings in crypto assets).

- The crypto market’s sentiment around these treasury models is shifting: share prices for crypto-treasury firms have fallen, and retail investors are estimated to have lost billions.

- For practitioners and investors looking at new crypto assets or blockchain business models, the regulatory and listing environment for companies holding large crypto treasuries is now a key factor.

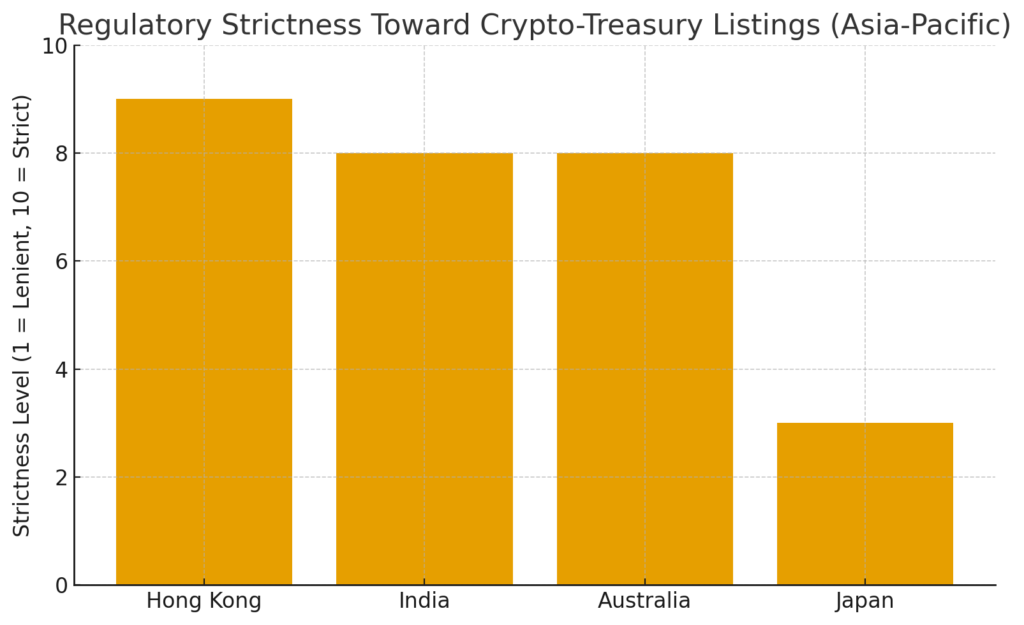

1. Regulatory Pushback in Hong Kong

In Hong Kong, the HKEX has taken a firm stance against companies that seek to restructure into what are being called Digital Asset Treasury (DAT) firms—publicly listed companies whose primary business becomes accumulating cryptocurrencies rather than traditional business operations. According to insiders, at least five firms in recent months have had their plans questioned by the exchange.

HKEX’s argument is that companies whose assets are mostly cash or short-term investments are considered “cash companies” or shell companies and may face suspension or delisting. In its rules, maintaining a “substantive business” is required.

For stakeholders in blockchain and treasury-driven crypto firms, this means that even if a company can accumulate large amounts of crypto assets, its ability to list—or remain listed—if its business model is essentially “hoard crypto & hope for price rise” is under review. This is less a comment on crypto per se and more about market-integrity regulations applied to cash-heavy entities.

2. India and Australia: Similar Constraints

In India, the Bombay Stock Exchange (BSE) recently rejected a company’s preferential share issue when that company disclosed it planned to invest part of the proceeds in crypto assets.

In Australia, the Australian Securities Exchange (ASX) has a rule that prohibits listed companies from holding more than 50% of their balance sheet in cash or “cash‐equivalent” assets. The effect is to make the classic treasury-crypto model (i.e., hold large crypto reserves) essentially unviable for a listed firm.

For those seeking new crypto investment opportunities via listed firms, this means that in these jurisdictions the option of investing in a “crypto treasury company” is becoming more restricted. It’s also a signal to private crypto companies considering going public.

3. Japan: The Exception — For Now

Japan presents a somewhat unique case in the Asia-Pacific region. According to reports, Japanese listing rules are relatively more permissive regarding companies that hold large cash reserves or invest in crypto assets.

For example, Japan has about 14 publicly listed companies that hold Bitcoin in their treasuries—the most in Asia. The CEO of the Japan Exchange Group (JPX), Mr. Hiro Yamaji, in a September 26 press conference stated that so long as proper disclosures are made, such business models are not inherently problematic.

However, cracks are appearing. The index provider MSCI is proposing to exclude companies whose crypto holdings represent more than 50% of assets from its indices—putting pressure on the premium valuations many crypto-treasury companies enjoyed.

For crypto investors and practitioners, Japan may still offer a more tolerant operational environment for treasury-centric crypto firms—but regulatory tides may be shifting.

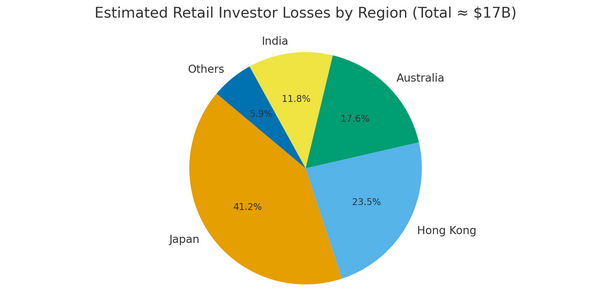

4. Market Implications: Valuation, Risk, and Strategy

The broader implications for the crypto-treasury model are significant. As companies shifted to accumulate Bitcoin and other assets (following the pioneering model of MicroStrategy Incorporated in the U.S.), valuations and investor expectations soared. However, as regulatory pushback and crypto-market corrections have occurred, that enthusiasm is cooling. Reports from Singapore-based research firm 10X Research estimate that retail investors have lost around US $17 billion trading crypto-treasury companies.

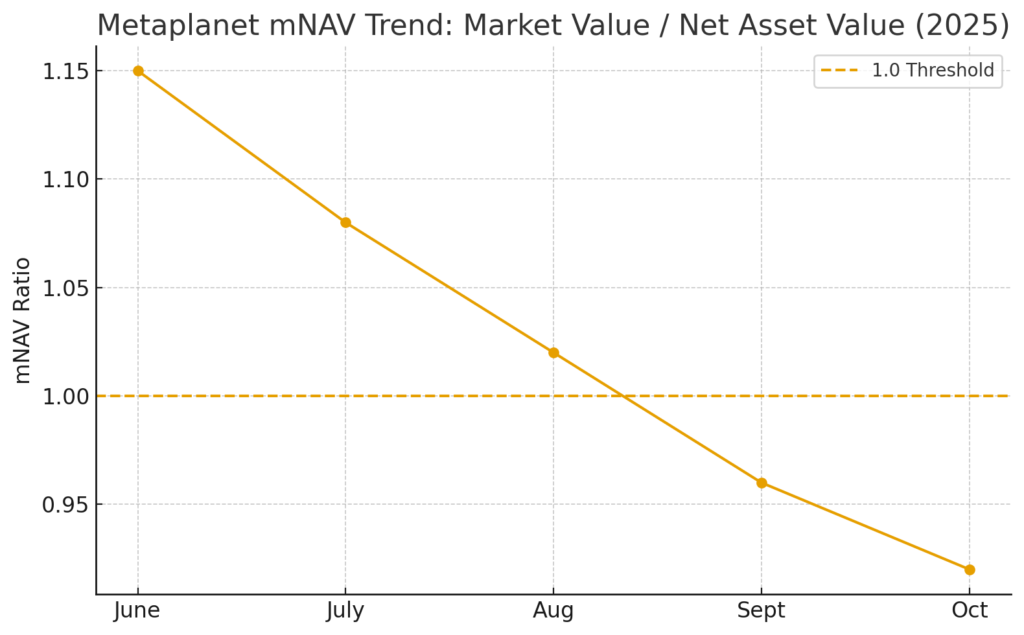

One notable example: the Japanese company Metaplanet Inc. had its enterprise-value indicator mNAV fall below 1 (i.e., market value < net asset value) to around 0.92, tracking the correction.

For blockchain and crypto practitioners, this means: models purely focused on accumulation may face higher scrutiny and risk (regulatory and market). Alternative strategies—such as real business operations, tokenization of real-world assets, or mixed treasury + business model—may have more durability.

5. Broader Blockchain & Crypto Trends to Watch

Beyond the immediate listing-and-treasury space, several related trends are emerging:

- In Japan, the Financial Services Agency is considering allowing banks (through securities subsidiaries) to provide crypto-asset services and lifting bans on banks holding crypto assets—suggesting an opening toward institutional infrastructure.

- Meanwhile, the regulatory environment is evolving globally: e.g., in Singapore, the Monetary Authority of Singapore is tightening rules on crypto exchanges, which is pressuring exchanges to relocate to more friendly hubs like Hong Kong or Dubai.

These developments suggest that while some business models (e.g., crypto-treasury firms) are coming under pressure, others (crypto financial infrastructure, regulated exchanges, tokenization of real-world assets) remain active and may present opportunities for innovation and early movers.

6. Implications for Seeking New Crypto Assets or Revenue Streams

For our readership—people looking for new crypto assets, next revenue sources, or practical blockchain business use—here are the key takeaways:

- If you’re evaluating a listed company (or one planning to list) whose business is “hold crypto and hope for appreciation,” check the jurisdiction’s listing rules: does the exchange treat large liquid holdings as problematic?

- Consider the risk that regulatory pushback may reduce valuation or market access for such companies—leading to potential discounting, forced de-listing, or index exclusions.

- Business models that combine treasury accumulation plus real operational activities (e.g., blockchain services, tokenization, DeFi infrastructure) might have more resilience.

- From a token perspective, blockchain projects that address real-world-asset tokenization, regulated exchange infrastructure, compliance services, or enterprise blockchain adoption may benefit from the regulatory shift away from pure accumulation narratives.

- Japan remains a relatively permissive environment for crypto-treasury models—but that may change, and investors should monitor index-provider actions, regulatory statements, and corporate disclosures.

7. Summary

In summary, the Asia-Pacific region’s major stock exchanges are increasingly skeptical of the crypto-treasury business model for listed companies—especially those whose primary activity is hoarding crypto assets rather than running a substantive business. Hong Kong, India, and Australia are tightening or enforcing listing rules that make the digital-asset-treasury model harder to execute. Japan is still more open, but cracks are appearing. For blockchain practitioners and investors, the message is clear: the era of simple crypto-asset accumulation as a corporate strategy is under strain—business models that combine treasury strategies with operational substance, or which participate in regulated crypto infrastructure, may be better positioned for the next phase of the market.

As you explore new crypto assets or revenue streams, pay attention not only to tokenomics but also to regulatory/listing dynamics, corporate business models, and the jurisdictional environment—they may be as important as the blockchain technology itself.