Main Points :

- Tokenized deposits backed by fiat currencies (USD, EUR) will be adopted by Alibaba’s B2B platform.

- Partnership with JPMorgan’s JPMD blockchain infrastructure enables faster, lower-cost cross-border settlement.

- Tokenized deposits differ from stablecoins by being issued on regulated bank balance sheets.

- Alibaba will prioritize bank-issued digital tokens first, with stablecoins only considered later depending on regulatory clarity.

- Tokenized deposits may redefine global trade settlement, supply-chain finance, and multi-currency liquidity.

- The trend aligns with broader institutional adoption: BlackRock, Citi, DBS, and HSBC are all scaling tokenized assets.

Introduction: A Turning Point in Global Trade Finance

Alibaba’s latest move—integrating tokenized deposit payments in partnership with JPMorgan—signals one of the most significant institutional steps toward blockchain-based global commerce. Rather than experimenting with speculative cryptocurrencies or unregulated stablecoins, Alibaba opted for the safest institutional-grade digital asset category: tokenized deposits, fully backed by fiat currencies and issued by regulated banks.

This decision positions Alibaba.com as a first mover in a new model of cross-border settlement—one where digital dollars or euros move instantly across a permissioned blockchain network, bypassing the spaghetti-like corridors of correspondent banking.

The shift is not only about operational efficiency. It reflects a much deeper trend: global corporations and financial institutions are converging around regulated digital money rails. For crypto investors, start-ups, blockchain builders, and traders, this transformation marks a pivotal new market cycle where real-world payments, tokenization, and institutional blockchains dominate the conversation.

1: Why Tokenized Deposits Matter More Than Stablecoins Right Now

1.1 What Exactly Are Tokenized Deposits?

Tokenized deposits are 1:1 digital representations of bank deposits, issued directly by regulated banks.

They differ from stablecoins in three key ways:

| Feature | Tokenized Deposits | Stablecoins |

|---|---|---|

| Issuer | Regulated banks | Non-bank entities (Circle, Tether, fintechs) |

| Backing | Bank balance sheet deposits | Treasuries, cash, money market funds |

| Regulatory clarity | Very high | Depends on jurisdiction |

| Primary users | Institutions, enterprises | Traders, crypto markets |

Alibaba’s decision reflects a major priority: global compliance. Tokenized deposits are fully aligned with banking law and audit requirements across the US, EU, and Asia.

1.2 Why This Matters for Large Corporations

Alibaba processes millions of B2B payments every month.

Its buyers and suppliers face three pain points:

- Slow settlement (2–5 days)

- High intermediary fees

- Multi-step currency conversion

Tokenized deposits solve all three:

- Instant or near-instant transfers

- Reduced reliance on correspondent banking

- Fewer conversion legs

- Lower FX spread leakage

- Transparent audit trails

In other words, this decision is not a speculative crypto experiment—it is a cost-compression strategy and an upgrade of global trade pipes.

2: The JPMorgan × Alibaba Architecture — JPMD

JPMorgan’s JPMD system (JPMorgan Digital Deposits) forms the backbone of this integration.

2.1 What JPMD Does

- Moves tokenized deposits between financial institutions

- Functions on a permissioned blockchain

- Processes international transfers in near real-time

- Supports multi-currency liquidity management

- Enables “atomic settlement” (payment + confirmation at the same time)

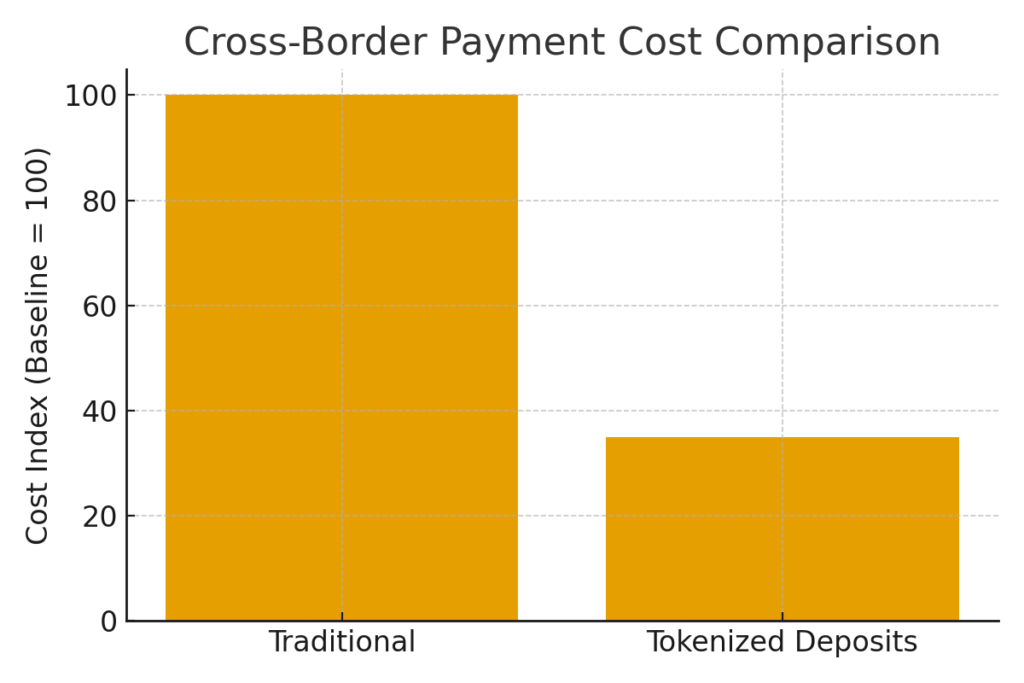

This is a monumental shift from existing SWIFT-based cross-border settlement, which was designed 50 years ago for paper-based payment messaging—not instant digital money transfer.

2.2 A Simple Example

Current method (slow):

US → Correspondent Bank A → Correspondent Bank B → China Supplier Bank → Supplier

Process: 2–7 banks involved

Tokenized deposit method (fast):

US Buyer Wallet → JPMD Tokenized USD → Supplier Wallet

Process: 1 step

Time: Seconds

This makes web-scale payments—for example, thousands of small supply-chain invoices—financially viable and faster.

3: Why Not Stablecoins? Alibaba’s Regulatory Logic

Alibaba publicly confirmed that it may explore stablecoins later but prioritizes tokenized deposits for now.

3.1 Regulatory Clarity

Stablecoins face:

- MiCA restrictions in the EU

- Uncertain US regulatory frameworks

- Asia-Pacific fragmentation

- Licensing requirements for issuance and redemption

- Varying AML/KYC rules

Tokenized deposits, however:

- Already fall under banking supervision

- Use existing KYC frameworks

- Are accounted for in familiar balance-sheet structures

- Present minimal systemic risk

For a multinational corporation like Alibaba, regulatory predictability is more valuable than speed of innovation.

4: Global Trend — Tokenization Is Becoming the New Default

Alibaba is not alone. In 2024-2025, major institutions have accelerated real-world asset tokenization.

4.1 Banks and Institutions Moving Fast

- BlackRock: $500M tokenized fund BUIDL

- Citi: Receivables tokenization for corporate clients

- HSBC: Gold tokenization platform

- DBS: Asia’s first large-scale tokenized bond issuance

- Japan’s MUFG: Progmat tokenization platform

- United Arab Emirates: CBDC for cross-border settlement

- Singapore: MAS Project Guardian (tokenized FX, bonds, liquidity pools)

The Alibaba-JPMorgan partnership is part of a synchronized wave where blockchain transforms payments at the institutional layer, not the retail crypto layer.

5: Implications for Crypto Builders and Traders

5.1 Demand for New Token Standards

With tokenized deposits becoming mainstream, new opportunities arise:

- Enterprise-grade wallets

- Multi-currency settlement smart contracts

- Global B2B liquidity pools

- Automated invoice financing

- Tokenized FX hedging

- On-chain KYC/AML modules

Startups that integrate payment rails + compliance rails will dominate.

5.2 Impact on Crypto Traders

Short-term impact:

- More liquidity enters blockchain environments

- Higher institutional participation

- Lower settlement friction for OTC desks

Long-term impact:

- Tokenized deposits could compete with USDC/USDT usage

- More regulated liquidity may reduce volatility in parts of the market

- Better stable money rails support growth of DeFi institutional pools

5.3 New Assets to Watch

Investors seeking new crypto assets with high real-world utility may watch:

- Tokenized FX pools

- Tokenized treasury assets (yield-bearing)

- Bank-issued digital dollars

- Liquidity routing protocols

- B2B settlement layer tokens

- Enterprise-focused blockchain L2s

6: Market Outlook — What Happens Next

Alibaba’s adoption is not isolated. It represents:

- A new global standard for B2B blockchain payments

- Pressure for competing platforms (Amazon, Flipkart) to integrate tokenized rails

- The potential creation of on-chain supplier reputation scores

- A future where 95% of cross-border trade moves through tokenized money by 2030

6.1 China’s and Asia’s Role

China’s enterprises control a large percentage of global manufacturing supply chains.

If these corporations collectively adopt tokenized payments, the entire global settlement ecosystem will accelerate its shift.

6.2 Western Regulation Acceleration

The US and EU are pushing frameworks for digital dollar regulations:

- EU: MiCA II

- US: Stablecoin Act (pending)

- UK: FCA digital asset promotion rules

- Asia: Hong Kong’s digital asset regime

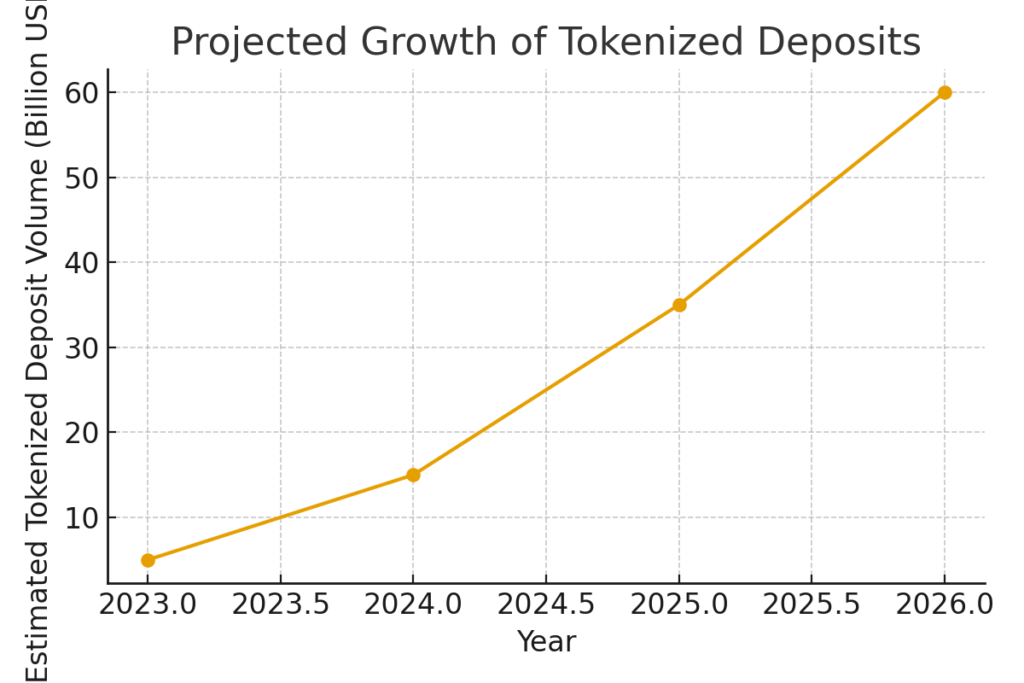

Institutional adoption will be shaped heavily by these frameworks in the next three years.Insert the Figure Here

[Insert Image: tokenized_deposit_growth.png]

This graph illustrates estimated growth in tokenized deposit volumes (2023–2025) reflecting institutional adoption.

(Download file)

👉 tokenized_deposit_growth.png

Conclusion

Alibaba’s adoption of tokenized deposits is not simply another blockchain news story—it marks the transition from crypto as an alternative system to blockchain as the underlying global settlement infrastructure.

For businesses: it promises faster, cheaper, and more predictable payments.

For banks: it opens new revenue models and compliance-aligned digital money issuance.

For crypto builders: it presents a massive opportunity to build middleware, wallets, APIs, and liquidity systems for enterprise tokenization.

For investors: it signals which assets will dominate the next cycle—institutional-grade money, tokenized real-world assets, and blockchain settlement rails.

We are entering a new era where blockchain becomes the invisible backbone of global commerce. Alibaba and JPMorgan are simply the first among many giants who will shape this landscape.