Main Points:

- Definition Guardrails: Restrict “staking” to protocol-level validation services to prevent confusion with passive yield products

- Yield Caps: Propose capping advertised staking yields at the network’s base rewards rate to curb misleading marketing

- Fee Limits: Suggest a maximum 5% intermediary fee, with higher fees requiring clear, auditable justification

- Real-Time Disclosures: Call for standardized interfaces displaying fees, yields, and risks in real time

- Validator Transparency: Recommend mandatory public dashboards tracking validator influence and performance

- Licensing Large Validators: Advocate a bank-style licensing regime for validators controlling significant stake

- Context of SEC Guidance: These proposals follow the SEC’s May 29, 2025 Staff Statement clarifying that many protocol staking activities are not securities

- Industry Implications: Platforms must adapt marketing and disclosure practices; investors gain clearer risk profiles

Introduction

On June 25, 2025, representatives of leading U.S. universities submitted a comprehensive set of recommendations to the Securities and Exchange Commission (SEC) targeting the burgeoning market of crypto asset staking. Their letter comes on the heels of the SEC’s landmark May 29 Staff Statement, which held that certain proof-of-stake (PoS) protocol staking activities do not amount to securities offerings under federal law. While that guidance clarified the regulatory status of core staking services, academic leaders warn that explosive marketing of high-yield products risks confusing retail investors and undermining network integrity.

Background on Crypto Staking and Yield Advertising

Staking, at its core, involves locking crypto assets to help validate transactions on PoS blockchains. Participants earn new tokens or transaction-fee shares as protocol rewards. As PoS networks like Ethereum, Cosmos, and Tezos have scaled, annual yields can range from 4% to 20%. However, yield advertisements on exchange platforms and wallets often quote net returns after fees—sometimes exceeding network base rates—leading unsophisticated investors to mistake speculative products for pure staking services.

University Recommendations to the SEC

A coalition of university deans, economics professors, and blockchain researchers urged the SEC to:

- Limit Use of “Staking”:

Only services that perform protocol-level consensus validation should use the term “staking.” Retail products promising fixed or enhanced returns should be labeled differently to avoid misperception. - Cap Advertised Yields:

Require platforms to advertise only the base reward rate provided by the blockchain protocol—no inclusion of intermediary rebates, bonus schemes, or mega-stake incentives. - Cap Intermediary Fees at 5%:

Any fees charged by custodians or node operators must not exceed 5% of gross rewards. Fee increases beyond this threshold are permissible only if providers publish auditable cost data in a standardized format. - Standardize Real-Time Disclosures:

Mandate APIs or user interfaces that show, in real time, all protocol yields, applicable fees, and risk factors (e.g., unbonding periods, slashing risk). - Enhance Network Oversight:

Introduce public dashboards detailing each validator’s share of total stake, performance metrics, and historical slashing incidents. - License Large Validators:

For validators with more than 10% of a network’s active stake, establish a bank-style licensing regime including capital requirements, periodic audits, and insurance obligations.

They argue these measures will help investors make informed choices, reduce “yield tourism,” and strengthen network decentralization by discouraging extreme concentration of stake.

SEC’s Protocol Staking Guidance: A Quick Recap

On May 29, 2025, the SEC’s Division of Corporation Finance issued a Staff Statement titled “Certain Protocol Staking Activities.” Key takeaways:

- Not Securities: Core PoS staking—“self-staking,” “self-custodial staking with a third party,” and “custodial staking”—falls outside the Howey investment-contract definition.

- Covered Crypto Assets Only: Applies only to assets that don’t carry intrinsic promises of passive yield beyond protocol rewards.

- Ancillary Services: Technical conveniences like early unbonding or slashing protection, by themselves, are not deemed “managerial efforts.”

While providing welcome clarity, the guidance is narrow in scope, and does not shield providers from private-party lawsuits or ensure full regulatory certainty. Legal counsel continues to advise caution for staking service offerings.

Industry Response and Recent Trends

Platforms and custodial services have swiftly updated marketing materials and user interfaces to align with the SEC’s core staking interpretation. Recent industry moves include:

- Rebranding High-Yield Products: A number of exchanges have relabeled “enhanced yield” offerings as “reward programs,” clearly separating them from protocol staking.

- Open APIs for Transparency: Leading wallets now publish machine-readable feeds of reward rates and fees, fulfilling the universities’ call for real-time disclosure.

- Validator Licensing Pilot Programs: At least two DeFi infrastructure firms are piloting voluntary audits and insurance schemes for validators controlling over 8% of their network’s stake.

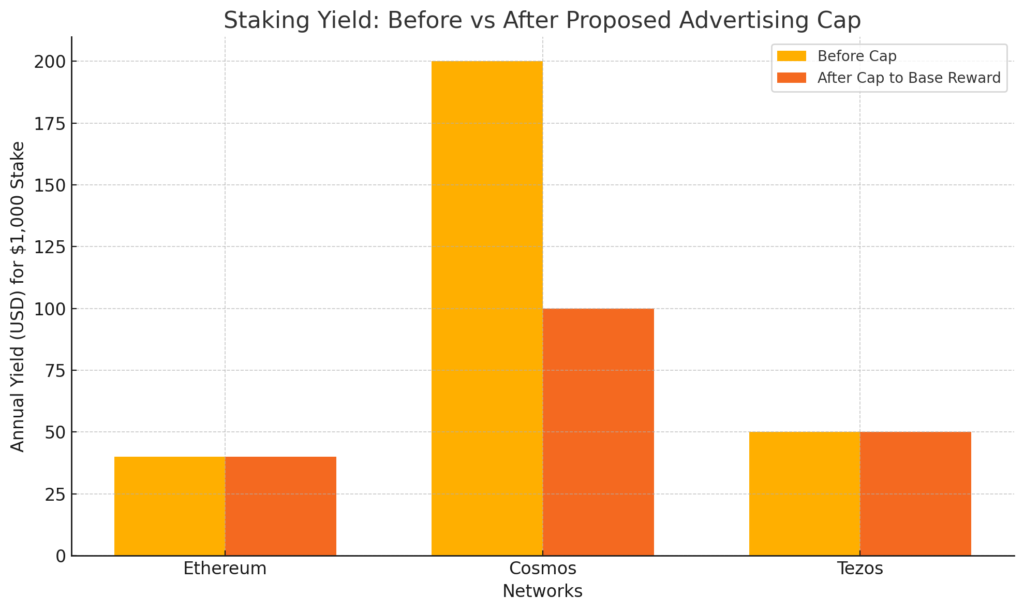

Below is a comparison of annual returns on a $1,000 stake, before and after the proposed yield-advertising cap:

Implications for Investors and Platforms

- For Investors:

- Clearer Risk Profiles: With base-reward advertising and real-time data, retail users can calibrate expectations accurately.

- Lower Fee Surprises: A strict 5% fee ceiling ensures that net yields remain closer to on-chain rates.

- Better Due Diligence: Validator dashboards help investors gauge decentralization health and avoid over-centralized nodes.

- For Platforms:

- Marketing Overhaul: Must revise collateral, remove ambiguous terms, and highlight protocol vs service fees.

- Compliance Costs: Building and maintaining disclosure interfaces, dashboards, and audit processes will raise operational overhead.

- Competitive Dynamics: Smaller staking providers may benefit as barriers curtail marketing wars among the largest platforms.

Looking Ahead: Potential SEC Actions

The university recommendations signal growing academic scrutiny of crypto financialization. Possible next steps include:

- Rulemaking on Yield Advertising: The SEC could open a rulemaking docket to formalize yield-cap regulations under Section 5 registration exemptions.

- Guidance on Validator Licensing: Staff-level guidance or an aspirational framework for validator oversight.

- Expanded Definition of Covered Crypto Assets: Tighten which tokens qualify for the protocol-staking exclusion.

The intersection of academic expertise and regulatory policy may set a new bar for transparency in decentralization finance. How the SEC balances innovation with investor protection will shape staking adoption in the years ahead.

Conclusion

As proof-of-stake networks become integral to blockchain scalability and sustainability, clear guardrails are essential. The university coalition’s multifaceted proposal—to restrict terminology, cap yields and fees, standardize disclosures, and license key validators—aims to protect retail investors and preserve network health. Coupled with the SEC’s recent protocol staking clarification, these measures could usher in a new era of transparent, responsible staking services. For investors seeking stable, yield-bearing crypto assets and practitioners building staking infrastructure, the next few months promise pivotal regulatory developments.