Key Takeaways:

- A7A5 is a ruble-pegged stablecoin developed by Russian-linked entities, now the largest stablecoin not pegged to the U.S. dollar.

- Its rapid growth (transaction volume, adoption) has drawn scrutiny from the U.S., U.K., and EU as a potential conduit for sanctions evasion.

- After prior sanctions, operators burned and reissued over 80% of tokens to break traceability.

- The EU is considering broad sanctions to ban any direct or indirect involvement by EU-based entities, and to penalize banks in Russia, Belarus, and Central Asia that facilitate its use.

- Enforcement faces serious technical, jurisdictional, and compliance challenges, as cross-border crypto rails complicate “cutouts” or intermediaries.

- For investors and blockchain professionals, A7A5 offers both a case study in state-backed digital payments infrastructure and a cautionary tale about regulatory risk.

Below is a combined English article and then a full Japanese translation (without summary), with subtitles for each section, concluding with a wrap-up.

What Is A7A5 and Why It Matters

A7A5 is a stablecoin pegged 1:1 to the Russian ruble (RUB), created by a consortium that includes A7 (a cross-border payments firm) and Promsvyazbank (PSB), a state-connected bank already under Western sanctions.

The issuing entity is Old Vector, an operating vehicle based in Kyrgyzstan.

Because of its ruble peg, A7A5 is appealing as a means to convert rubles into dollar-denominated crypto, effectively creating an on-ramp/bridge between sanctioned Russian finance and international crypto markets.

One notable twist: A7A5 promises to pay users a passive yield equivalent to half the interest earned by the ruble deposits backing it, distributed daily.

This yield incentive helps drive demand—but also raises risk, as the underlying ruble reserves are held in Promsvyazbank, which is under sanction.

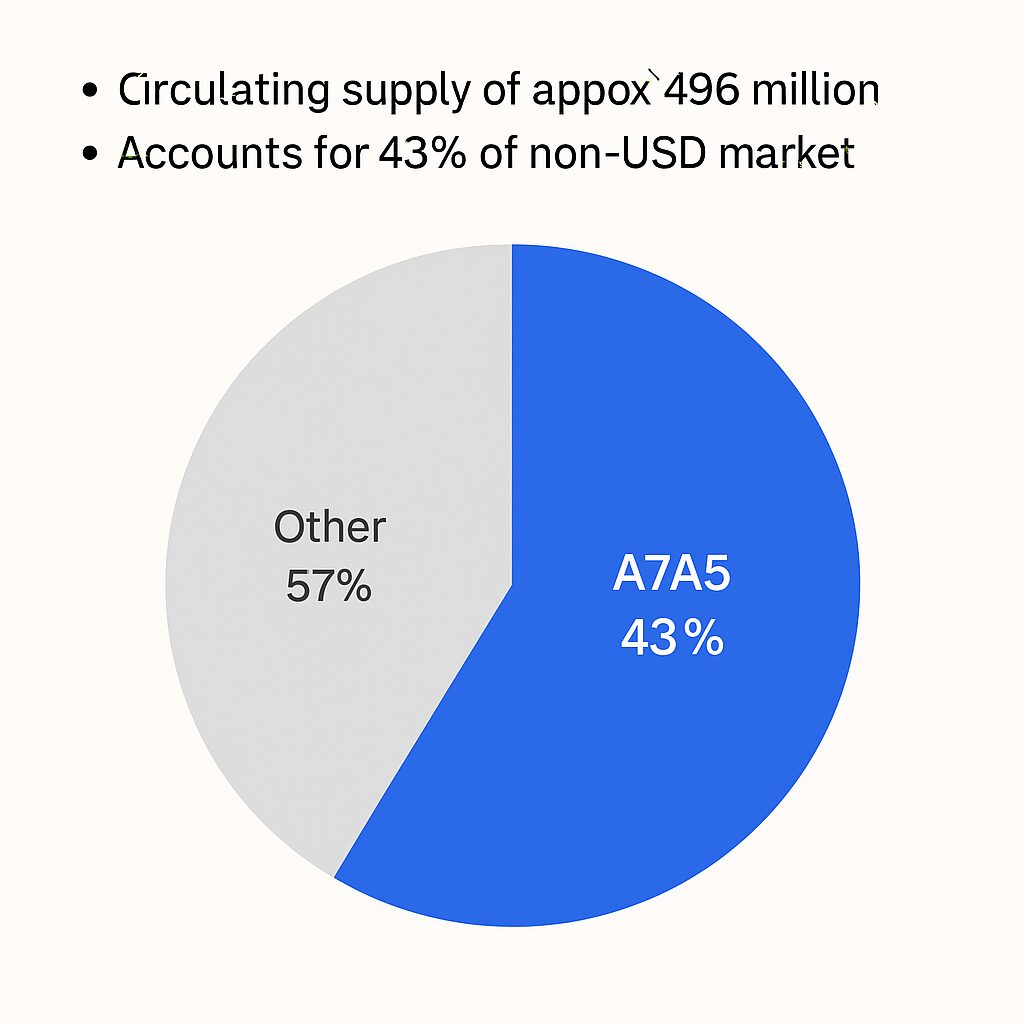

As of late September 2025, about 41.6 billion A7A5 tokens were in circulation, valued at roughly US$496 million, and cumulative transaction volume had reached about US$68 billion.

It now claims the top spot among non-USD pegged stablecoins, representing ~43% of that narrower market.

All this matters because A7A5 has the potential to undermine sanctions regimes by providing a crypto-based veil for sanctioned Russian entities to move capital. Its rapid adoption and state backing make it a unique experiment at the intersection of geopolitics, finance, and blockchain.

How It Evolves Under Sanctions: “Burn and Reissue” & Address Cleansing

In mid-August 2025, following U.S. and UK sanctions on Garantex and related entities, A7A5 operators activated a function called “destroyBlackFunds.” Through that, over 80% of token supply tied to sanctioned addresses was burned and then reissued under fresh addresses, severing on-chain traceability to their prior wallets.

After that reset, a new tranche of ~US$6.1 billion (61 billion in nominal units) was processed through these new addresses, with activity clustering during Moscow business hours—signaling coordination and a desire to mimic prior usage patterns.

This reissuance tactic has made forensic tracing of prior illicit flows significantly harder. Enforcement agencies must chase new addresses without backward linkage, complicating sanctions enforcement.

EU’s Proposed Sanctions: What and Whom They Target

The European Union is now actively considering sanctions on A7A5. The draft proposal would:

- Ban any direct or indirect engagement of EU-based entities (companies, individuals, service providers) in transactions involving A7A5.

- Penalize banks in Russia, Belarus, and Central Asia that process or facilitate crypto payments associated with the A7A5 network.

- Require unanimous approval across all 27 EU member states before enactment.

The logic is that restricting European participation will choke off liquidity and global on-ramps, making A7A5 less usable in western jurisdictions. It also aligns with prior EU moves to block cryptocurrency transactions for Russian residents and restrict ties with foreign banks facilitating crypto flows.

However, there are caveats: some reports suggest that only a small portion of Bitcoin trading in the EU is actually routed through ruble-backed stablecoins like A7A5—around 2.37%—which limits how much the sanctions might disrupt core European crypto markets.

Recent Developments & Global Reactions

- Even after sanctions, A7A5 has moved over US$6 billion since August, including via the reissuance trick to dodge traceroutes.

- A7A5’s issuer appeared as a sponsor at the TOKEN2049 crypto conference in Singapore. After media pressure, references to the project were later removed.

- Singapore authorities have clarified that their sanctions do not automatically apply to non-licensed entities like crypto projects, giving A7A5 some safe harbor locally.

- Data suggests its geographic footprint is expanding: 78% of A7A5 transactions reportedly route through Chinese jurisdictions. Offices and traction in Africa (e.g. Nigeria, Zimbabwe) are growing.

- In July 2025, cumulative A7A5 flows passed US$40 billion, with daily throughput exceeding $1B.

- The sharp spike in market capitalization—e.g. a 250% jump one day in September—has raised red flags among analysts and regulators.

Challenges in Enforcing Crypto-Sanctions

Enforcing these proposals faces multiple obstacles:

1. Jurisdictional gaps & global rails

Since A7A5 is issued in Kyrgyzstan and traded across multiple blockchains (Ethereum, Tron), enforcement by any single jurisdiction (like the EU) has limited reach.

Operators can shift portions of operations outside of formal financial systems to evade restrictions.

2. Address resets and mixing techniques

Burning and reissuing tokens severs traceable chains, complicating blockchain forensics. The use of mixing services or cross-chain bridges may further obfuscate flows.

3. Indirect relationships & intermediaries

EU entities could be cut off, but collateral providers (e.g. custodians, wallet services, VASPs) may unintentionally facilitate routing. Holding “guilt by association” risk may deter legitimate crypto services from operating in Europe at all.

4. Compliance cost & legal uncertainty

Virtual Asset Service Providers (VASPs) in Europe will need to invest heavily in compliance systems (KYC, blockchain analytics) to ensure none of their flows indirectly involve A7A5. This raises barriers to entry and raises legal liability.

5. Potential retaliation & fragmentation

Russia or other aligned nations may respond with their own crypto controls or create parallel networks that completely bypass EU oversight.

What This Means for Crypto Investors & Builders

For those looking for new crypto projects or infrastructure opportunities, the A7A5 case is instructive:

- It shows how state-backed stablecoins might evolve as de facto national financial rails in geo-strategic domains.

- The yield incentive model (50% of interest) is a feature worth understanding for designing token economics, though it carries systemic risk if backing assets are under sanction.

- Regulatory risk is an existential threat—no matter how technically novel a project is, it can be curtailed by evolving sanction regimes.

- For blockchain infrastructure builders, designing resilient auditing/traceability tools or compliance layers that can adapt to address resets may become valuable.

- On the flip side, projects exploring permissionless, neutral rails must consider how they might be co-opted or regulated in extreme geopolitical contexts.

Conclusion

A7A5 is more than a niche stablecoin—it is a bold attempt to monetize geopolitical friction using blockchain. Its fast growth, yield mechanics, and ability to dodge traceability pose a real challenge to conventional sanctions architecture. The EU’s effort to regulate or even ban involvement shows that crypto regulation is catching up to states’ ambitions to weaponize digital finance.

For crypto practitioners, A7A5 offers lessons: technology without legal discipline is vulnerable, but state-level backing can push projects into new territory. Ultimately, how enforcement plays out—whether regulators can outpace reissuance tricks and jurisdictional escape hatches—will determine whether this experiment becomes a caution or a template for future digital finance.