Main Points :

- Standard Chartered revised its aggressive Bitcoin price forecasts downward, pushing the long-anticipated $500,000 target from 2028 to 2030.

- Digital Asset Treasury (DAT) firms—once expected to supply strong BTC demand—are now facing stock price collapses that limit their ability to accumulate more Bitcoin.

- The bank now views ETF-driven inflows as the primary driver of future BTC appreciation.

- Despite Bitcoin’s ~36% decline since its October peak, analysts argue markets remain within a normal correction range—not a new “crypto winter.”

- For investors, the downgrade reshapes the timeline but not the long-term bullish thesis, and new opportunities are emerging outside BTC in sectors such as real-world tokenization, Web3 gaming, and Layer-2 infrastructure.

Introduction: A Market Reassessment Rather Than a Collapse

On December 9, Standard Chartered’s Head of Digital Assets, Geoff Kendrick, released a notable update to the bank’s high-profile Bitcoin forecast. His memo, titled “Not a crypto winter, just a cold breeze,” emphasized that while Bitcoin’s recent performance—with a drop of approximately 36% from its October 6 high—feels painful, it remains consistent with historical volatility and does not signify structural deterioration.

However, this reassessment resulted in the bank slashing its year-end forecasts for 2025–2028 and postponing the highly publicized $500,000 price target to 2030. The reason is not simply macroeconomic pressure or ETF flows slowing temporarily. Rather, it is rooted in a deeper structural shift: the unexpected breakdown of Digital Asset Treasury (DAT) firms, whose valuations previously supported Standard Chartered’s bullish assumptions.

This article summarizes the key findings of Kendrick’s analysis, integrates current developments from broader digital-asset markets, and outlines investment implications for readers seeking new opportunities in crypto assets, income strategies, or practical blockchain applications.

Section 1: Why Standard Chartered’s Bitcoin Forecast Was Downgraded

1.1 The Collapse of Digital Asset Treasury Firms

A major assumption behind Standard Chartered’s optimistic long-term price targets was the expectation that Bitcoin-focused treasury companies—enterprises that raise capital to purchase and hold BTC on their balance sheets—would continue accumulating aggressively.

Instead, many of these firms experienced sharp declines in equity valuations. Some are now trading below the fair value of the Bitcoin they hold, meaning their market capitalization is less than the worth of their BTC reserves.

This creates a structural problem:

- They cannot justify issuing new shares to fund further Bitcoin purchases.

- Their capacity to act as major BTC accumulators—similar to MicroStrategy—has been dramatically constrained.

- The loss of this demand weakens one pillar of the bull thesis.

Kendrick notes that this does not signal a mass liquidation or a wave of selling from these firms. Rather, it diminishes a potential tailwind that had supported expectations of rapid price appreciation.

1.2 ETF Inflows as the Remaining Growth Driver

With DAT firms sidelined, Bitcoin ETFs become the primary mechanism of institutional demand.

ETFs have already brought billions in inflows globally, particularly in the U.S., Europe, and regions like Hong Kong and the Middle East.

But they take time:

- Investment committees must review exposure guidelines.

- Institutional mandates often require multi-month evaluations.

- Some pension and insurance funds move slowly due to regulatory oversight.

Kendrick still believes ETFs will bring a “second wave” of institutional participation, but the timing has shifted, forcing recalibration of forecast models.

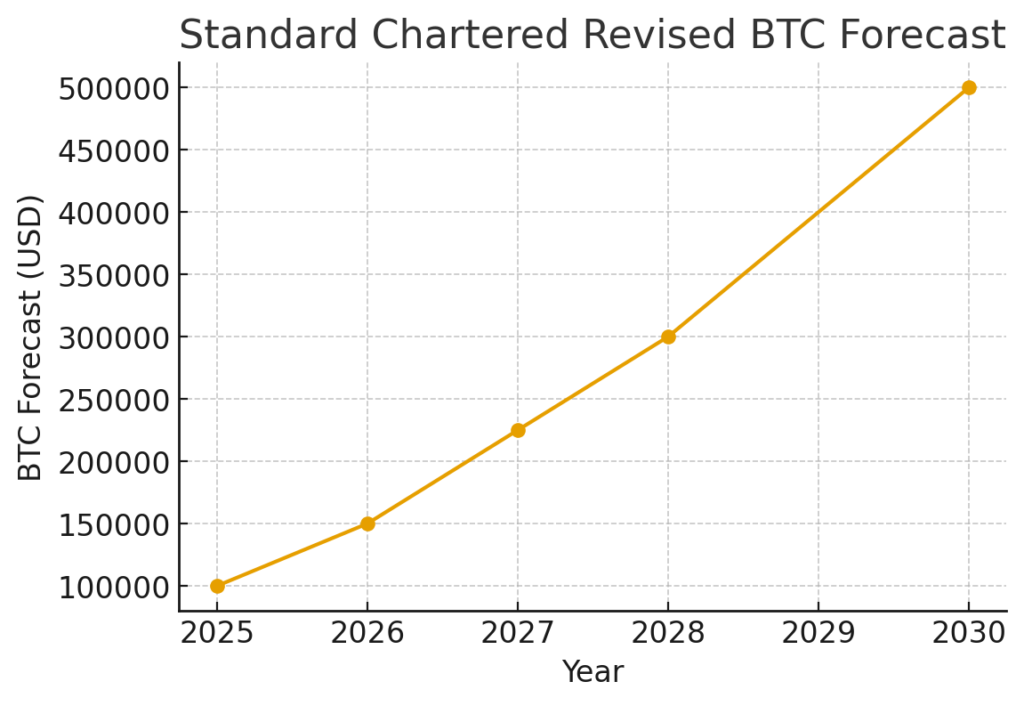

1.3 The Revision: New BTC Forecast Path

Here is the revised schedule presented entirely in USD:

| Year | Previous Forecast | Revised Forecast |

|---|---|---|

| 2025 | $200,000 | $100,000 |

| 2026 | $300,000 | $150,000 |

| 2027 | $400,000 | $225,000 |

| 2028 | $500,000 | $300,000 |

| 2030 | — | $500,000 (new timeline) |

This shift reflects a softer, slower ramp rather than abandonment of the long-term thesis.

Section 2: Is This Really Not a “Crypto Winter”?

2.1 Comparing Today’s Market to 2018 and 2022

Historically, genuine crypto winters involve:

- A collapse of liquidity

- Massive industry bankruptcies

- Long periods of flat or declining activity

- Regulatory crackdowns restricting growth

None of these conditions apply today.

Bitcoin miners remain profitable on average.

ETF inflows continue at a moderate but steady pace.

Developers across DeFi, Web3, and AI-integrated blockchain platforms are increasing, not declining.

Kendrick describes the downturn as a “cold breeze”—a deep but healthy correction in the context of Bitcoin’s broader adoption curve.

2.2 Market Liquidity and Risk Appetite Remain Intact

Derivative open interest, stablecoin supply, and exchange liquidity remain solid.

This distinguishes the current environment from past crypto winters when liquidity fully evaporated.

Most importantly, institutional products (ETFs, custody, accounting rules) continue to expand. The long-term infrastructure is stronger today than at any time in Bitcoin’s history.

Section 3: Implications for Investors Seeking the Next Revenue Source

3.1 Bitcoin’s Slower Ascent Opens Space for High-Growth Sectors

With Bitcoin’s explosive scenario delayed, capital will likely rotate toward emerging high-growth crypto segments:

Tokenized Real-World Assets (RWAs)

U.S. Treasury tokens, corporate bond tokenization, and yield-bearing digital assets are attracting billions.

Platforms such as BlackRock’s BUIDL and Franklin Templeton’s on-chain money funds demonstrate institutional commitment.

Web3 Gaming and Digital IP Platforms

Unlike the 2021 play-to-earn bubble, today’s Web3 gaming integrates sustainable economics and multi-chain interoperability.

Layer-2 Scaling and Modular Blockchain Infrastructure

Rollup-as-a-service providers, data-availability layers, and zero-knowledge systems are rapidly expanding—often outpacing L1 tokens in growth rate.

AI-Integrated Crypto Systems

AI-driven smart-contract agents and decentralized computation markets (similar to RNDR or FET) are becoming dominant themes.

Investors seeking the next revenue source increasingly diversify into these segments, using BTC as a macro hedge rather than a sole growth engine.

3.2 A Slower Bitcoin Ramp May Actually Attract More Institutions

Fast parabolic moves historically repel conservative institutions.

A smoother curve—e.g., BTC rising from $100k → $150k → $225k—allows:

- Pension funds

- Insurance companies

- University endowments

- Corporate treasuries

to integrate Bitcoin into multi-year asset allocation plans with less volatility concern.

This slower timeline may therefore increase the total eventual institutional participation, supporting Standard Chartered’s view that $500,000 remains achievable—just later.

Section 4: Immediate Market Risks Investors Should Watch

4.1 ETF Outflows and Macro Interest-Rate Shocks

If ETF outflows accelerate—especially from U.S. providers—short-term price pressure could intensify.

Similarly, a sudden rise in U.S. Treasury yields or delayed rate cuts may temporarily lower BTC demand.

4.2 DAT Firms’ Financial Health

Should additional DAT firms trade below their net BTC asset value, M&A activity or forced restructuring could raise temporary market uncertainty.

4.3 Regulatory Actions in Major Markets

Although regulation is improving overall, enforcement actions (e.g., exchange compliance issues) may create localized shocks.

Conclusion: A Delay, Not a Denial, of Bitcoin’s Long-Term Potential

Standard Chartered’s downgrade is not a retraction of its bullish stance; it is an acknowledgment that market structure—not sentiment—has changed.

The collapse of Digital Asset Treasury firm valuations removed one catalyst, forcing reliance on ETF inflows and institutional timelines.

But the core thesis remains:

- Bitcoin is still progressing toward global institutional adoption.

- On-chain metrics and infrastructure growth remain robust.

- Long-term appreciation is intact, even if delayed by several years.

For investors searching for new crypto assets, fresh revenue streams, or real-world blockchain use cases, this environment presents more opportunities—not fewer. As Bitcoin stabilizes into a more predictable institutional asset, emerging sectors such as RWAs, Web3 gaming, modular blockchains, and AI-crypto integration may deliver outsized gains in the coming cycle.

The breeze may be cold, but it is far from winter.