Regulatory reset: A new Executive Order (EO) signed on August 7, 2025 bans “politicized or unlawful” debanking and directs federal bank regulators to remove “reputational risk” concepts from guidance and examination manuals within 180 days.

Agency follow-through already underway: The Federal Reserve (June 23, 2025) and the OCC (March 2025) have already moved to strike reputational risk from bank exams; the FDIC has signaled rulemaking to do the same.

Direct crypto implications: The White House fact sheet explicitly cites the digital-asset industry as a past target of debanking; the EO orders look-backs, remediation, and penalties where appropriate—potentially easing bank access for compliant crypto firms.

Market angle: Policy momentum may catalyze U.S. banking rails for exchanges, stablecoin issuers, and service providers; a separate—but related—move discussed in D.C. would revisit retirement-plan access to crypto, with nearly $9 trillion of 401(k) assets at stake if rules change.

Still not a free pass: Banks remain bound by BSA/AML, sanctions, and safety-and-soundness obligations. Removing “reputational risk” does not prevent institutions from declining high-risk clients on objective, risk-based grounds.

What happened—and why it matters

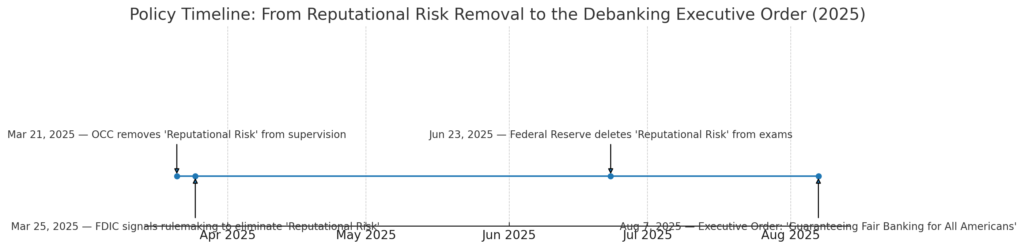

On August 7, 2025, the White House issued “Guaranteeing Fair Banking for All Americans,” an Executive Order banning “politicized or unlawful” debanking and instructing federal agencies to purge “reputational risk” from the machinery of bank supervision (guidance, exam manuals, examiner playbooks) within 180 days. The EO also mandates look-backs for past debanking, remediation for affected customers, and potential penalties for violations. The accompanying fact sheet explicitly names the digital-asset industry as one of the sectors previously targeted by unfair debanking.

The order caps months of agency movement: in June 2025 the Federal Reserve said reputational risk would no longer be a component of bank-exam programs, aligning with parallel steps by the OCC in March and anticipated action by the FDIC. In short, the supervisory “catch-all” that made lawful but controversial industries harder to bank is being dismantled.

Insert Figure 1 (Policy Timeline) here.

The policy context: From “Operation Choke Point 2.0” to an explicit prohibition

For years, crypto advocates and some lawmakers argued that prudential supervisors used reputational-risk rhetoric and informal “nudges” to discourage banks from serving lawful industries—crypto included—a pattern dubbed “Operation Choke Point 2.0.” The House Financial Services Committee held hearings on the matter in February 2025. While investigative reporting and even critical analysis concede the evidence is mixed, the perception of coordinated pressure shaped market behavior—banks avoided crypto to sidestep supervisory friction.

Concrete examples outside crypto also became political flashpoints, such as alleged account closures of Christian nonprofits by major banks, fueling claims of belief-based discrimination (claims the involved institutions dispute). These cases amplified calls for clear limits on subjective criteria in supervision and access.

The Federal Reserve’s June move formally deleting reputational risk from exam programs—and trade, legal, and mainstream-press confirmation—signaled a sharp pivot even before the EO. Now the order locks that pivot into an administration-level directive and sets clocks running for all regulators to conform.

What the Executive Order actually does

1) Prohibits politicized or unlawful debanking. The EO bars financial institutions and regulators from denying services based on political or religious beliefs or otherwise lawful activities. It directs agencies to eradicate supervisory concepts that enable such discrimination.

2) Mandates a comprehensive strategy and look-backs. Treasury is tasked to craft a national strategy—including potential regulatory or legislative options—to detect, deter, and remediate unlawful debanking, with look-backs and reinstatement as appropriate.

3) Forces manual and guidance changes on a deadline. Regulators must remove “reputational risk” and equivalents from manuals, guidance, and examiner instructions within 180 days—turning an agency trend into a binding timeline.

4) Names crypto as a beneficiary of fair access. The fact sheet says the digital-asset industry has been an unjust target of debanking and positions the EO as restoring neutral, risk-based access for lawful firms.

Immediate implications for digital-asset businesses

Access to basic rails could improve. The most immediate effect is procedural: examiners will have less room to lean on vague “reputation” concerns when reviewing a bank’s crypto exposure. That can lower perceived supervisory risk for offering operating accounts, payment processing, fiat on/off-ramps, merchant services, custody, and treasury solutions to compliant crypto firms. Banks still must—and will—assess BSA/AML, sanctions, fraud, cybersecurity, and operational risks, but the starting posture becomes neutral rather than wary by default.

Stablecoin and prime services could see momentum. Banks considering stablecoin issuer accounts, liquidity services, or prime brokerage-style offerings may revisit shelved plans, especially as the Fed and OCC changes propagate into day-to-day examinations. The FDIC’s rulemaking outlook adds further alignment across the “big three” bank regulators.

Retirement savings angle worth watching. Separately, Washington chatter points to a potential EO revisiting how 401(k) plans treat alternative assets, including crypto—if realized, this could open a channel to nearly $9 trillion in retirement assets. That said, this development is prospective and controversial; fiduciary standards under ERISA will remain stringent.

How regulators are aligning—what changes inside agencies

The OCC has already begun scrubbing its Comptroller’s Handbook and told examiners to stop examining for reputational risk. The Fed publicly removed reputational risk from its exam program and began revising supervisory materials accordingly. The FDIC has indicated plans to propose rules to ensure exam findings are not based on reputational factors alone. The EO puts an administration-wide deadline on these alignments and adds potential accountability if agencies lag.

What changes at banks—and what does not change

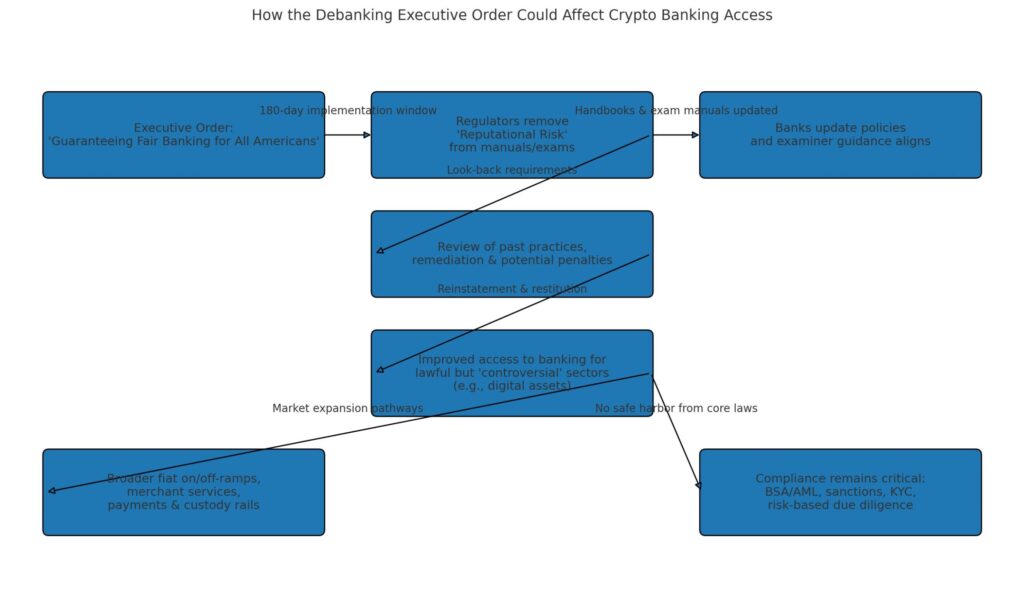

Bank policy revisions. Expect institutions to update customer-acceptance policies, industry exposure statements, and exam management playbooks to remove reputational-risk language and to reflect the EO’s fair-access posture. Supervisory dialogue may pivot from “reputation” to specific, measurable risks: liquidity, credit, operational, legal/compliance, and concentration.

No safe harbor. The EO does not override statutes or safety-and-soundness obligations. Banks can still decline or offboard crypto customers if objective risk-based analyses justify the decision (e.g., weak controls, sanctions exposure, fraud rates). Agencies have emphasized that robust risk management still applies even as they stop scoring “reputation.”

Insert Figure 2 (Impact Flow) here.

Market reaction snapshot

Below is a live price widget for BTC to monitor any near-term reaction as policy headlines settle. (Note: price moves reflect many drivers; attribution to policy alone is speculative.)

Actionable playbook for crypto businesses (next 30–180 days)

1) Re-engage target banks with a tightened risk narrative. Package your controls in the language examiners will now prioritize: KYC/KYB coverage, sanctions screening efficacy, SAR workflow SLAs, transaction-monitoring rules by risk typology, fraud-loss ratios, cybersecurity controls (SOC 2/ISO 27001), and segregation of client assets. Present quantified metrics, independent testing results, and auditor attestations.

2) Map bank-facing compliance artifacts to agency manuals. As the OCC, Fed, and (likely) FDIC update manuals, align your documentation to the latest sections on operational risk, third-party/vendor risk, model risk, and consumer compliance. This makes your file “exam-ready” when banks brief supervisors.

3) Prepare for “look-back” opportunities. The EO contemplates reinstatement where debanking was unlawful. Keep records of denial/offboarding rationales, correspondence, and remediation since 2023. If a bank signals willingness to revisit, have an updated control stack ready.

4) For stablecoin and payments firms: emphasize reserve and attestation quality. Present reserve composition, daily reconciliation, independent attestations, and liquidity stress test outputs—areas where reputational concerns once dominated the conversation will now pivot to these measurable controls.

5) Monitor the retirement-plan front—but don’t bank on it yet. If 401(k) access truly opens, it will require ERISA-grade risk disclosures, fee controls, and custodian standards. Treat it as an option value, not a base case until rules are published.

Risks and unknowns

Litigation and political swings. An EO can face court challenges or be narrowed by future administrations. Firms should avoid over-reliance on policy winds and continue building for jurisdictional diversity.

Bank risk appetite may lag. Even with formal changes, boards may proceed cautiously given residual headline risk and losses from past crises. Supervisors also warn that reputational events can morph into liquidity or operational risks—those remain in scope.

Proof vs. perception. Investigations into “Choke Point 2.0” may still conclude there was no explicit conspiracy, just risk-averse supervision. Either way, the EO reframes expectations; execution will determine outcomes.

What to watch next

Regulator deliverables: Track each agency’s 180-day updates to manuals and examiner guidance.

FDIC rule text: When proposed, it will clarify how examiners must justify findings absent reputational factors.

Congressional oversight: Follow hearings for signals on bipartisan durability (or fragility) of fair-access norms.

Bank policy memos: Expect updated crypto exposure statements from large banks and leading regionals.

Potential retirement-plan EO or DOL guidance: This could reshape on-shore distribution channels for digital assets if it materializes.

Bottom line

The anti-debanking Executive Order—paired with the Fed’s and OCC’s reputational-risk rollbacks—marks a pivotal turn in U.S. banking supervision. For crypto, it should lower procedural friction for access to essential rails, provided firms demonstrate robust, measurable controls. The EO does not create a safe harbor: expect banks to keep demanding high compliance bars. But for lawful, well-run digital-asset businesses, the path to mainstream banking just became clearer.

About Us and Media

Blockchain and cryptocurrency media covering and exposing the practical application development on the blockchain industry and undiscovered coins.

Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.