Key Points :

- Hong Kong has issued its first official stablecoin issuer licenses under a new regulatory framework.

- Licenses were granted to Anchorpoint Financial and HSBC.

- Anchorpoint is backed by Standard Chartered, Animoca Brands, and HKT.

- The move represents a major milestone in regulated crypto finance led by the Hong Kong Monetary Authority.

- Signals growing convergence between traditional finance and Web3 infrastructure.

- Expected to accelerate real-world adoption of stablecoins in payments, remittances, and tokenized finance.

Introduction: Regulation Meets Real Adoption

On April 10, 2026, Hong Kong took a decisive step toward becoming a global hub for regulated digital finance. The Hong Kong Monetary Authority (HKMA) officially granted its first-ever stablecoin issuer licenses to Anchorpoint Financial and HSBC under the newly enacted Stablecoin Ordinance.

This development is not just another regulatory headline—it marks a structural shift in how stablecoins are perceived and deployed. No longer confined to crypto-native ecosystems, stablecoins are increasingly being positioned as regulated financial instruments capable of supporting real economic activity.

For investors, builders, and institutions seeking the next wave of blockchain-driven revenue and utility, this moment represents a critical inflection point.

A New Regulatory Era for Stablecoins

The licensing framework introduced by the HKMA is designed to strike a delicate balance: enabling innovation while ensuring financial stability and consumer protection.

Unlike earlier crypto-friendly jurisdictions that relied on lighter-touch oversight, Hong Kong’s approach is institutional-grade from day one. Licensed issuers must meet strict requirements, including:

- Full reserve backing (typically in fiat or highly liquid assets)

- Robust risk management frameworks

- Transparent auditing and reporting obligations

- Clear redemption rights for users

This positions Hong Kong as a jurisdiction where stablecoins are not just tolerated—but integrated into the financial system with regulatory clarity.

HKMA CEO Eddie Yue described the licensing as a “milestone,” emphasizing that regulation is not a barrier to innovation, but rather a foundation for sustainable growth.

Anchorpoint: A Strategic Joint Venture

One of the most interesting aspects of this development is the structure of Anchorpoint Financial.

Rather than a typical crypto startup, Anchorpoint represents a strategic convergence of banking, telecom, and Web3 expertise:

- Standard Chartered brings global banking infrastructure

- Animoca Brands contributes deep Web3 and tokenization experience

- HKT adds telecommunications and distribution capabilities

This combination is highly intentional. It reflects a broader trend: stablecoins are no longer purely financial products—they are infrastructure layers that require integration across multiple industries.

Anchorpoint is expected to focus on building stablecoin solutions that can be used in:

- Cross-border payments

- Digital commerce ecosystems

- Tokenized asset settlement

HSBC’s Entry: Traditional Finance Goes Native

The involvement of HSBC is equally significant.

As one of the largest banking institutions in the world, HSBC’s participation signals that stablecoins are moving beyond experimentation into core financial strategy.

Historically, large banks have approached crypto cautiously. However, the emergence of regulated frameworks like Hong Kong’s is changing that calculus.

HSBC’s role could include:

- Issuing fiat-backed stablecoins

- Facilitating institutional liquidity

- Integrating stablecoins into existing banking rails

This aligns with a broader global trend where major financial institutions—including JPMorgan Chase and Goldman Sachs—are actively exploring tokenization and blockchain-based settlement systems.

Global Context: The Stablecoin Race Intensifies

Hong Kong’s move does not exist in isolation. It is part of a rapidly evolving global landscape where governments and institutions are competing to define the future of digital money.

United States

The U.S. is advancing stablecoin legislation aimed at bringing issuers under federal oversight. While progress has been slower, the direction is clear: regulated stablecoins are becoming inevitable.

Europe

The European Union’s MiCA Regulation has already established a comprehensive framework for crypto assets, including stablecoins, setting a high bar for compliance.

Asia

Singapore and Japan are also advancing regulatory clarity, but Hong Kong’s aggressive push—combined with its proximity to mainland China—gives it a unique strategic position.

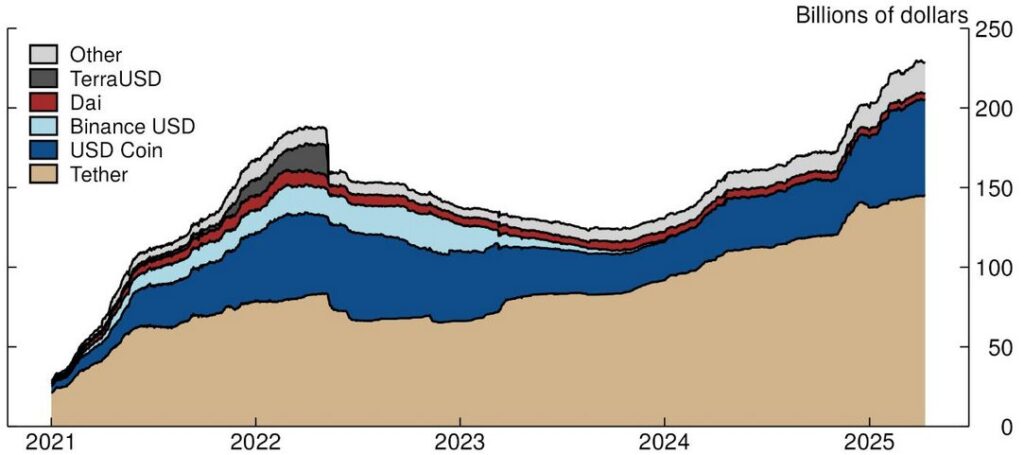

Global Stablecoin Market Growth (USD)

Growth of the global stablecoin market, highlighting increasing adoption in payments and trading ecosystems.

From Crypto Trading to Real Economy Use Cases

Stablecoins were initially popularized as tools for crypto trading—providing liquidity and a hedge against volatility.

However, their role is rapidly expanding into the real economy:

Cross-Border Payments

Stablecoins can reduce settlement times from days to minutes while significantly lowering costs. For remittance-heavy regions, this is transformative.

Merchant Payments

With proper regulation, stablecoins can be used for everyday transactions, competing directly with traditional payment networks.

Tokenized Finance

Stablecoins serve as the base layer for tokenized assets, including bonds, equities, and real estate.

Hong Kong’s licensing framework is specifically designed to enable these use cases by providing legal certainty and institutional trust.

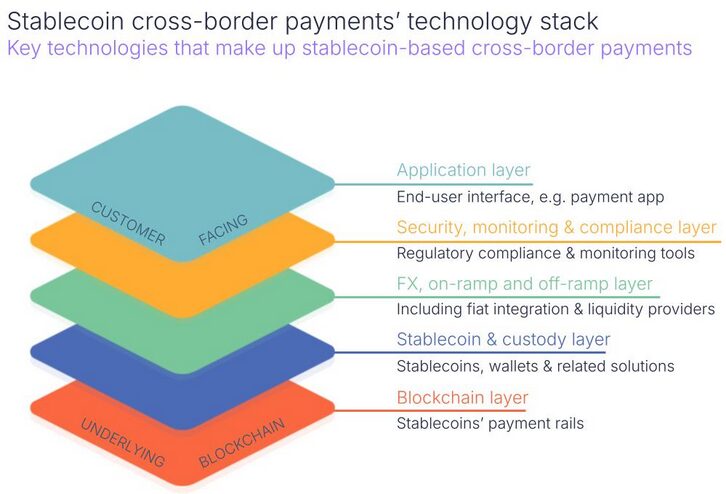

Stablecoin Use Case Flow

How stablecoins integrate into payments, remittances, and tokenized financial systems.

Implications for Investors and Builders

For readers seeking new crypto assets and revenue opportunities, this development offers several key insights:

1. Infrastructure Is the New Alpha

The real value may not lie in speculative tokens, but in infrastructure layers like stablecoins, payment rails, and compliance systems.

2. Institutional Capital Is Entering

With regulated frameworks in place, large-scale capital is more likely to enter the market—bringing stability but also competition.

3. Compliance Is a Competitive Advantage

Projects that can align with regulatory requirements will have a significant edge in attracting partnerships and users.

4. New Revenue Models

Stablecoins enable new monetization strategies, including:

- Transaction fees on payment rails

- Yield generation through reserves

- Integration into DeFi and CeFi ecosystems

Risks and Challenges

Despite the optimism, several risks remain:

- Regulatory fragmentation across jurisdictions

- Dependence on fiat reserves and banking systems

- Potential competition from Central Bank Digital Currencies (CBDCs)

- Operational risks in large-scale issuance

However, Hong Kong’s framework attempts to address many of these concerns through strict oversight and clear rules.

Conclusion: A Blueprint for the Future of Finance

Hong Kong’s issuance of its first stablecoin licenses is more than a regulatory milestone—it is a blueprint for the future of finance.

By bringing together global banks, Web3 innovators, and a robust regulatory framework, Hong Kong is demonstrating how digital assets can transition from speculative tools to core financial infrastructure.

For investors, developers, and institutions, the message is clear:

The next phase of crypto is not about hype—it is about integration, utility, and real-world impact.