Key Takeaways :

- A projected $100 trillion generational wealth transfer is accelerating crypto adoption

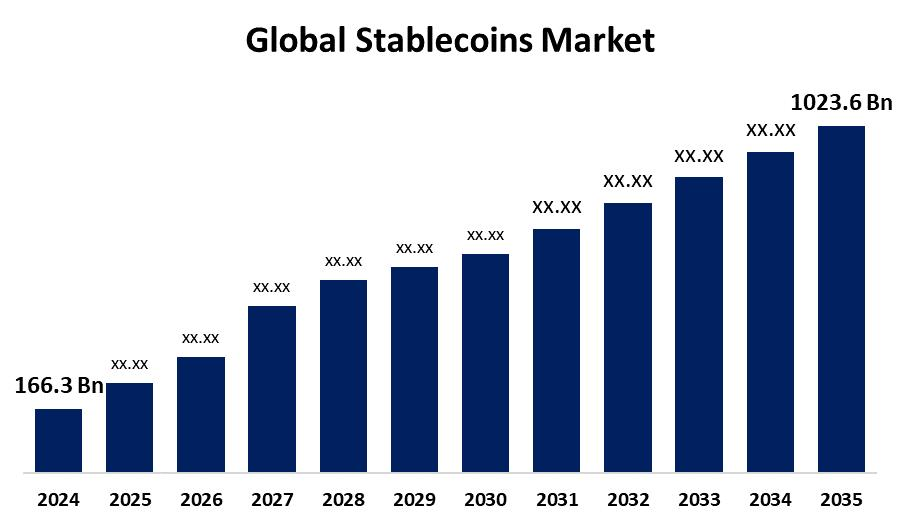

- Stablecoin transaction volume reached $28 trillion in real economic activity (2025)

- Growth rate of 133% annually since 2023 suggests exponential expansion

- Base scenario: $719 trillion annual volume by 2035

- Bull case: up to $1,500 trillion, surpassing global cross-border payments (~$1,000T)

- POS integration could add $232 trillion annually

- Stablecoins may rival or surpass Visa/Mastercard transaction volumes

- Institutional adoption is accelerating through partnerships and regulation

1. Introduction: The Dawn of a New Financial Era

The global financial system is approaching a structural transformation of unprecedented scale. A convergence of demographic shifts, technological innovation, and institutional adoption is driving what could become one of the largest reallocations of wealth in modern history. At the center of this transformation lies the rise of stablecoins—digital assets pegged to fiat currencies that are rapidly evolving from niche tools into core infrastructure for global payments.

According to recent analysis by Chainalysis, stablecoin transaction volumes—when adjusted to exclude artificial activity such as MEV (Maximal Extractable Value), bot trading, and liquidity provisioning—have already reached approximately $28 trillion in real economic usage as of 2025. This figure alone signals a paradigm shift: stablecoins are no longer speculative instruments but are becoming embedded in real-world economic flows.

2. Stablecoin Growth Projection (2025–2035)

3. Exponential Growth: From $28 Trillion to $1,500 Trillion

Since 2023, adjusted stablecoin transaction volume has grown at an astonishing compound annual rate of 133%. If this trajectory continues, the base-case projection places stablecoin volume at $719 trillion annually by 2035.

However, the more aggressive scenario—taking into account macroeconomic tailwinds—pushes this figure to approximately $1,500 trillion annually. To put this into perspective, the entire global cross-border payments market today is estimated at roughly $1,000 trillion.

This implies that stablecoins are not merely competing with existing financial rails—they are positioned to replace and redefine them entirely.

The implications are profound:

- Traditional correspondent banking systems may become obsolete

- Settlement latency could drop from days to seconds

- Financial inclusion could expand dramatically

4. The $100 Trillion Catalyst: Generational Wealth Transfer

One of the most powerful drivers behind this transformation is the impending $100 trillion intergenerational wealth transfer expected between 2028 and 2048.

This transition—from Baby Boomers to Millennials and Gen Z—is not just a transfer of capital but a transfer of financial philosophy.

Younger generations:

- Are significantly more comfortable with digital assets

- View crypto as a standard financial tool, not an alternative

- Are actively participating in on-chain ecosystems

Studies indicate that approximately 50% of Millennials and Gen Z already own or have owned cryptocurrency, according to research from Gemini.

Chainalysis estimates that this demographic shift alone could contribute an additional $508 trillion in annual transaction volume by 2035.

Beyond stablecoins, this wealth migration is also fueling adjacent sectors:

- Tokenized real-world assets (RWA)

- On-chain prediction markets

- Decentralized financial infrastructure

This is not just adoption—it is a systemic migration of value into blockchain-native systems.

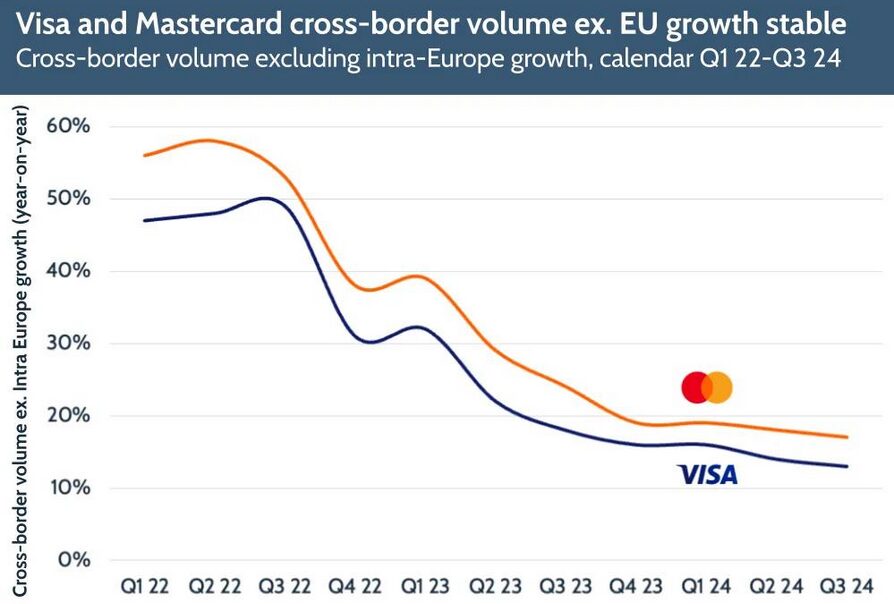

5. The Point-of-Sale Revolution: Stablecoins in Everyday Payments

Stablecoins vs Traditional Payment Networks

Another critical vector of growth lies in the integration of stablecoins into point-of-sale (POS) systems.

Today, paying with stablecoins is still a deliberate action. However, once merchants universally accept them, this distinction disappears—stablecoins become invisible infrastructure, much like credit cards today.

If transaction growth trends continue:

- Stablecoin transactions could match Visa and Mastercard volumes between 2031 and 2039

- Adoption curves could accelerate even faster due to network effects

POS adoption alone could contribute an additional $232 trillion in annual transaction volume by 2035.

6. Institutional Momentum: Stripe, Mastercard, and the Infrastructure Shift

Recent industry developments highlight a clear trend: stablecoins are being integrated into mainstream financial infrastructure.

Key signals include:

- Stripe acquiring Bridge

- Mastercard partnering with BVNK

These moves indicate that traditional payment giants are not resisting disruption—they are actively embracing it.

Why?

Because stablecoins offer structural advantages:

| Feature | Traditional Rails | Stablecoins |

|---|---|---|

| Settlement Time | 1–5 days | Seconds |

| Availability | Limited hours | 24/7/365 |

| Intermediaries | Multiple | Minimal |

| Cross-border cost | High | Low |

This efficiency is particularly critical for:

- Emerging markets

- Cross-border remittances

- Real-time treasury operations

7. Regulatory Acceleration and Global Competition

Regulation is no longer a barrier—it is becoming an enabler.

In the United States, legislative efforts such as the GENIUS Act are shaping a clearer framework for stablecoin issuance and usage. This regulatory clarity is shifting financial institutions from a “wait-and-see” approach to active execution.

In Japan, major banks are already exploring yen-denominated stablecoins, with projections suggesting a market size of approximately $7 billion (~¥1 trillion) by 2028.

Globally, this creates a competitive dynamic:

- Early adopters will define the new financial rails

- Late adopters risk becoming dependent on external infrastructure

8. Strategic Implications: Winners and Losers in the Next Financial Cycle

The rise of stablecoins introduces a binary outcome for financial institutions:

Winners

- Build or integrate stablecoin infrastructure early

- Capture transaction flow and data

- Reduce operational costs

Losers

- Delay adoption

- Become dependent on third-party rails

- Lose control over customer relationships

This dynamic mirrors previous technological shifts:

- Internet adoption in the 1990s

- Mobile payments in the 2010s

In each case, early movers defined the ecosystem.

9. Beyond Payments: The Expansion into a Tokenized Economy

Stablecoins are just the entry point.

Once capital moves on-chain, it naturally expands into:

- Lending and borrowing (DeFi)

- Tokenized securities and bonds

- Automated financial contracts

This creates a composable financial system, where services are interconnected and programmable.

For investors and builders, this means:

- New revenue streams

- New asset classes

- New infrastructure opportunities

10. Conclusion: A Once-in-a-Century Financial Transformation

The convergence of:

- $100 trillion in generational wealth transfer

- Exponential growth in stablecoin usage

- Institutional adoption and regulatory clarity

- Integration into everyday payment systems

…points to a fundamental conclusion:

We are not witnessing incremental innovation—we are witnessing the reconstruction of the global financial system.

Stablecoins are no longer optional. They are becoming the default layer for value transfer.

By 2035, the question will not be whether stablecoins are used—but how deeply they are embedded into every aspect of finance.