Key Takeaways :

- The Federal Deposit Insurance Corporation (FDIC) has released its second major regulatory framework for payment stablecoin issuers.

- The proposal introduces strict capital requirements, custody rules, and clarity on pass-through deposit insurance.

- Stablecoins themselves are not insured, but tokenized deposits may qualify for FDIC protection under certain conditions.

- Yield-bearing stablecoin marketing is expected to be heavily restricted.

- Large issuers (over $50 billion market cap) will face mandatory annual audits and stronger oversight.

- The proposal aligns with broader U.S. efforts under the GENIUS Act and ongoing debates in Congress.

- Global regulatory convergence is accelerating, impacting investment opportunities, fintech strategy, and blockchain infrastructure design.

1. Introduction: Regulation Catches Up with Reality

The global financial system is undergoing a structural transformation, and stablecoins have quietly become one of its most critical layers. What began as a niche tool for crypto traders has evolved into a multi-hundred-billion-dollar market underpinning payments, remittances, decentralized finance, and institutional settlement.

Against this backdrop, the Federal Deposit Insurance Corporation (FDIC) has unveiled a comprehensive new regulatory framework targeting payment stablecoin issuers. This marks the second major rulemaking effort tied to the GENIUS Act, signaling a decisive shift in how the United States intends to govern digital dollar instruments.

This development is not merely regulatory housekeeping—it is a foundational step toward integrating blockchain-based money into the formal financial system. For builders, investors, and institutions, this is a signal that stablecoins are no longer experimental—they are becoming regulated financial infrastructure.

2. The FDIC Framework: Core Structure and Intent

The FDIC’s proposal establishes a multi-layered regulatory structure that focuses on prudential safety, consumer protection, and systemic risk containment.

At its core, the framework mandates that stablecoin issuers maintain robust reserve backing and redemption mechanisms. Issuers must demonstrate that every token in circulation is backed by high-quality, liquid assets, ensuring that holders can redeem their tokens at par value—effectively preserving the “stable” in stablecoin.

In addition, the proposal introduces new requirements for insured depository institutions (IDIs) that provide custody services. These institutions must meet enhanced operational and compliance standards when handling stablecoin reserves, reflecting the increasing interconnection between crypto infrastructure and traditional banking systems.

A particularly notable element is the clarification of pass-through deposit insurance. Under specific conditions, funds held as stablecoin reserves in insured banks may qualify for FDIC insurance, but only if structured correctly. This distinction creates a clear separation between the token itself (which is not insured) and the underlying deposits (which may be).

3. Capital Requirements and Operational Backstops

One of the most impactful aspects of the proposal is its emphasis on capital adequacy and operational resilience.

Stablecoin issuers will be required to maintain capital buffers separate from their reserves. This ensures that operational losses, fraud incidents, or market disruptions do not compromise the integrity of the backing assets.

Additionally, issuers must maintain an operational backstop based on prior-year expenses. This requirement effectively forces companies to hold sufficient liquidity to sustain operations even under stress scenarios—an approach reminiscent of traditional financial risk management frameworks, but adapted for digital asset firms.

For large issuers with market capitalizations exceeding $50 billion, the FDIC mandates annual independent audits. This introduces a new level of transparency and accountability, aligning major stablecoin issuers with public company–like scrutiny.

4. Restrictions on Yield-Bearing Stablecoins

Another critical provision is the restriction on marketing stablecoins as yield-generating instruments.

This addresses a long-standing regulatory concern: the blurring of lines between deposits, securities, and digital tokens. By limiting the ability of issuers to advertise returns simply for holding stablecoins, regulators aim to prevent consumer confusion and reduce systemic risk associated with “shadow banking” behaviors.

This move also directly impacts business models that rely on yield distribution, forcing issuers to rethink how they generate and share revenue.

5. Stablecoins vs. Tokenized Deposits: A Critical Distinction

The FDIC framework draws a clear line between two often-confused concepts:

- Stablecoins (privately issued digital tokens pegged to fiat currencies)

- Tokenized deposits (digital representations of bank deposits)

While stablecoins themselves are not eligible for deposit insurance, tokenized deposits that meet regulatory requirements can be treated similarly to traditional bank deposits.

This distinction is crucial. It suggests that the future of digital money may bifurcate into two parallel systems:

- Regulated bank-issued tokenized deposits (fully integrated into TradFi)

- Non-bank stablecoins (subject to stricter constraints and oversight)

For fintech builders, this creates strategic decisions around licensing, partnerships, and product architecture.

6. The Bigger Picture: U.S. Regulatory Convergence

The FDIC is not acting in isolation. The United States is rapidly building a coordinated regulatory framework across multiple agencies, including:

- The Office of the Comptroller of the Currency (OCC)

- The U.S. Treasury Department

- Ongoing legislative efforts in Congress, including the proposed Clarity Act

These efforts collectively aim to define the legal and operational boundaries of digital assets, particularly stablecoins.

One key area of debate is the treatment of yield—whether stablecoin returns should be classified as interest, securities income, or something entirely new. The outcome of this debate will have significant implications for both compliance and innovation.

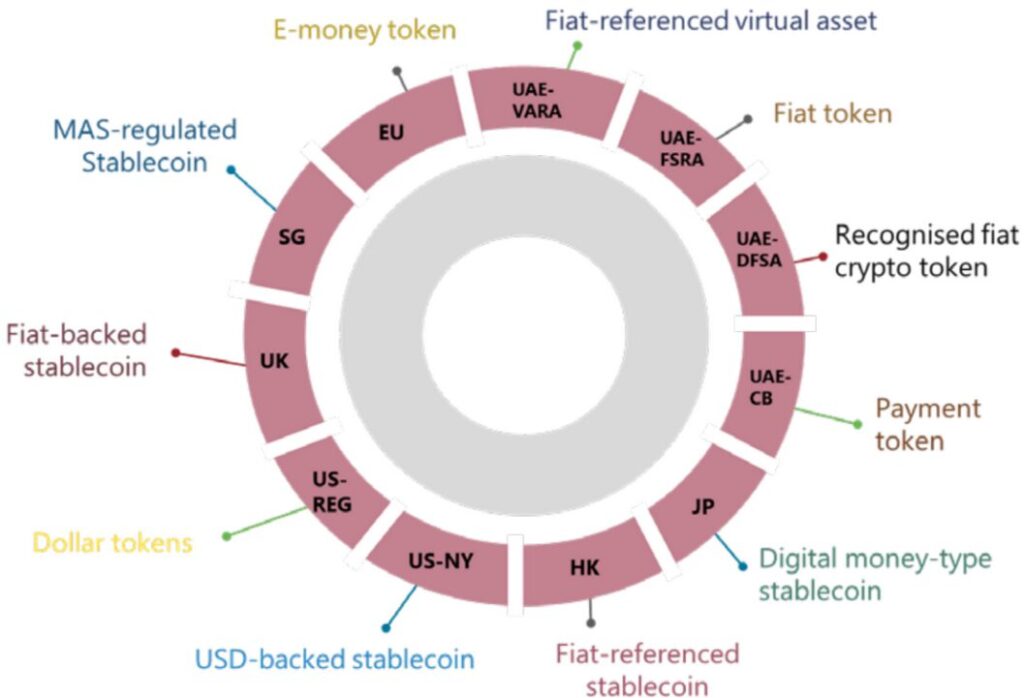

7. Global Context: Japan, Europe, and Beyond

The regulatory push in the United States mirrors similar developments globally.

In Japan, stablecoin regulations have already been formalized, allowing only licensed banks, trust companies, and certain registered entities to issue fiat-backed stablecoins. This has created a highly controlled but legally clear environment.

Meanwhile, the European Union’s Markets in Crypto-Assets (MiCA) regulation is setting comprehensive standards for stablecoin issuance, including reserve requirements, governance, and consumer protection.

These parallel efforts suggest a global convergence toward a regulated stablecoin ecosystem—one that prioritizes safety and transparency while enabling innovation.

8. Market Impact: Opportunities and Strategic Shifts

For investors and entrepreneurs, the FDIC framework introduces both constraints and opportunities.

Opportunities

- Institutional Adoption: Clear rules lower barriers for banks and financial institutions to enter the market.

- Infrastructure Demand: Compliance tools, custody solutions, and audit services will see increased demand.

- Tokenized Deposits: A new category of digital money may emerge as a dominant model.

Challenges

- Margin Compression: Restrictions on yield may reduce profitability for issuers.

- Compliance Costs: Smaller players may struggle to meet regulatory requirements.

- Market Consolidation: Larger, well-capitalized firms are likely to gain market share.

Global Stablecoin Regulatory Landscape (2026)

9. Strategic Implications for Builders (Especially Fintech & VASP Operators)

For companies building EMI, VASP, or hybrid financial platforms, this regulatory evolution requires immediate strategic consideration.

Key design implications include:

- Structuring reserves to qualify for pass-through insurance

- Partnering with insured depository institutions

- Implementing full audit trails and real-time risk monitoring

- Designing products that avoid classification as yield-bearing instruments

- Preparing for cross-border regulatory fragmentation

In particular, hybrid models—combining traditional finance controls with on-chain execution—are likely to become the dominant architecture.

10. Conclusion: From Experiment to Infrastructure

The FDIC’s stablecoin framework marks a turning point in the evolution of digital finance.

Stablecoins are no longer operating in a regulatory gray zone—they are being systematically integrated into the global financial system. This transition will reshape not only how money moves, but also who controls the infrastructure of that movement.

For forward-looking investors and builders, the message is clear:

The next phase of crypto is not about speculation—it is about regulated, scalable, and interoperable financial systems.

Those who align early with this direction—by building compliant infrastructure, forming strategic partnerships, and understanding regulatory nuance—will be best positioned to capture the opportunities ahead.