Key Points :

- China is accelerating the use of blockchain in its “Bank–Tax Interaction” (银税互动) financing model

- The goal is to reduce data asymmetry and unlock lending for small and medium-sized enterprises (SMEs)

- Blockchain and privacy computing are being encouraged for secure, tamper-proof data sharing

- The policy reflects a broader trend: separating crypto speculation bans from blockchain infrastructure adoption

- This initiative could reshape global fintech models for credit scoring, embedded finance, and SME lending

Introduction: A Strategic Shift in Financial Infrastructure

China has taken another decisive step toward integrating blockchain into its national financial infrastructure. In a joint directive issued by the State Taxation Administration and the National Financial Regulatory Administration, authorities have explicitly encouraged the use of blockchain and privacy-enhancing technologies to deepen the “Bank–Tax Interaction” financing model.

This policy move is not merely a technical upgrade. It represents a structural transformation in how credit is assessed, how financial data is shared, and how small businesses access capital. At its core, the initiative aims to solve one of the most persistent problems in emerging and developed economies alike: the financing gap for SMEs.

For readers exploring new crypto assets, revenue streams, and practical blockchain applications, this development is particularly significant. It signals where real-world adoption is happening—not in speculative trading, but in financial plumbing.

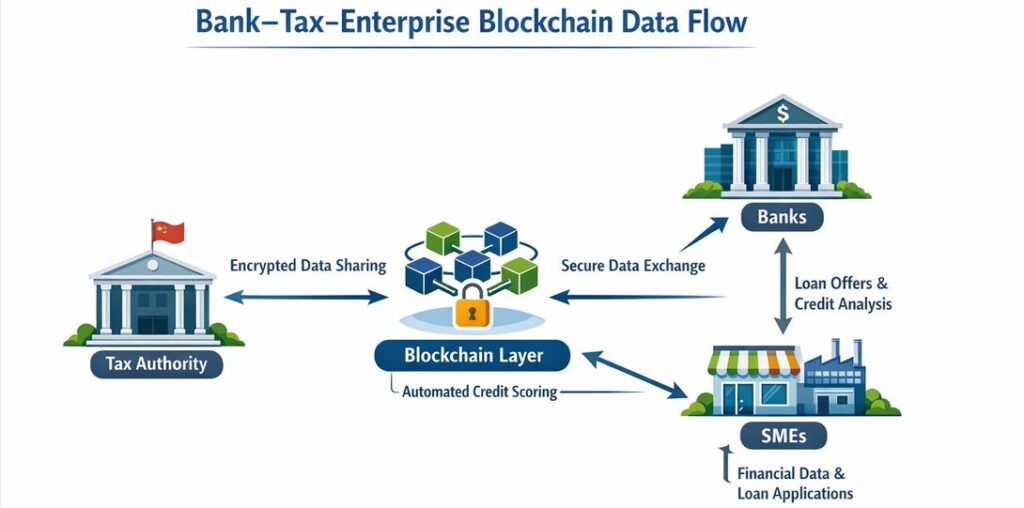

Bank–Tax–Enterprise Blockchain Data Flow Diagram

(Description: A diagram showing Tax Authority ↔ Blockchain Layer ↔ Banks ↔ SMEs, highlighting encrypted data sharing and credit scoring automation.)

Understanding the “Bank–Tax Interaction” Model

The “Bank–Tax Interaction” model, introduced around 2019, allows banks to use verified tax data to assess the creditworthiness of businesses. Instead of relying solely on collateral or traditional credit histories, financial institutions can evaluate a company’s tax payments as a proxy for operational health and compliance.

This is particularly valuable for SMEs, which often lack:

- Long credit histories

- Sufficient collateral

- Formal financial documentation

By leveraging tax records, banks gain access to a more reliable and standardized dataset.

However, the model has historically faced limitations:

- Data silos between tax authorities and banks

- Manual processes and document verification

- Risk of data tampering or inconsistency

- Privacy concerns around sensitive financial information

The introduction of blockchain aims to address all of these issues simultaneously.

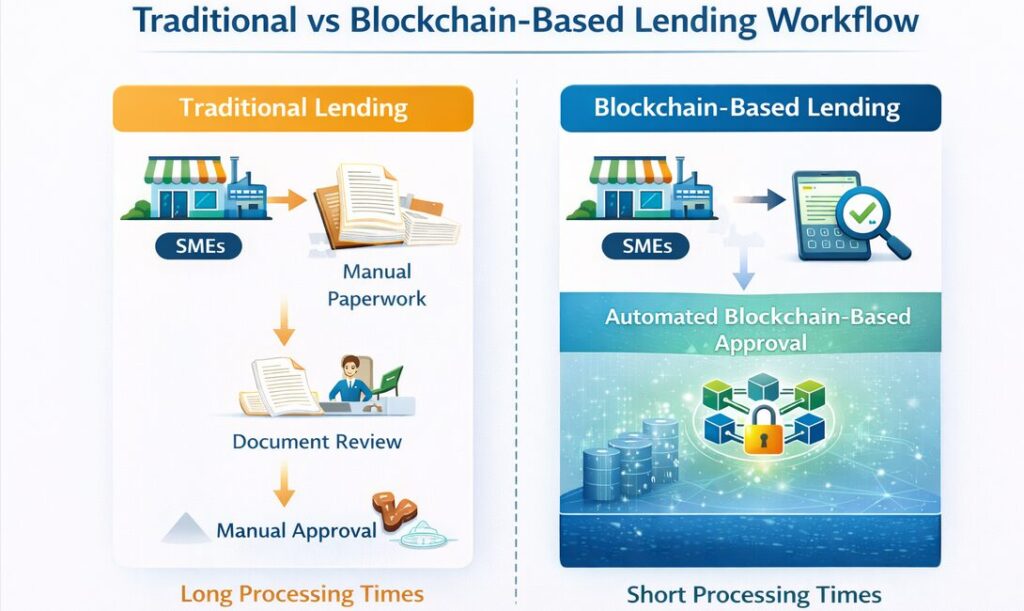

Traditional vs Blockchain-Based Lending Workflow

(Description: Side-by-side comparison showing manual paperwork vs automated blockchain-based approval flow.)

How Blockchain Enhances Financial Data Sharing

Blockchain technology introduces three critical capabilities to the Bank–Tax Interaction model:

1. Tamper-Resistant Data Integrity

Once tax data is recorded on a blockchain, it cannot be altered without consensus. This ensures that banks are working with authentic, verified information.

2. Standardized Data Sharing

The directive calls for standardized data formats between tax authorities, banks, and enterprises. Blockchain can act as a shared infrastructure layer, reducing fragmentation.

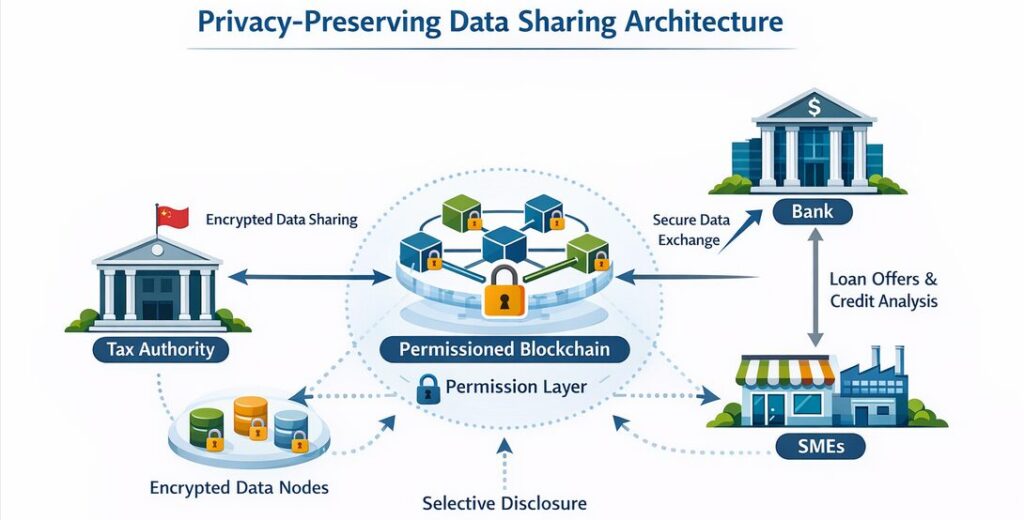

3. Permissioned Access and Privacy

Through techniques such as privacy computing and permissioned blockchain systems, sensitive data can be shared selectively without exposing raw information.

This combination allows for a secure yet efficient data exchange ecosystem.

Privacy-Preserving Data Sharing Architecture

(Description: Encrypted data nodes, permission layers, and selective disclosure between institutions.)

Reducing Information Asymmetry in SME Lending

One of the most important aspects of this policy is its focus on eliminating information asymmetry.

In traditional finance, lenders often have less information about borrowers than the borrowers themselves. This imbalance leads to:

- Higher interest rates

- Loan rejections

- Conservative lending practices

By integrating tax data into lending models—and securing it with blockchain—banks can make more informed decisions. This is expected to:

- Increase loan approval rates for compliant SMEs

- Reduce risk premiums

- Accelerate loan processing times

In practical terms, a small business that consistently pays taxes can now translate that behavior into immediate financial credibility.

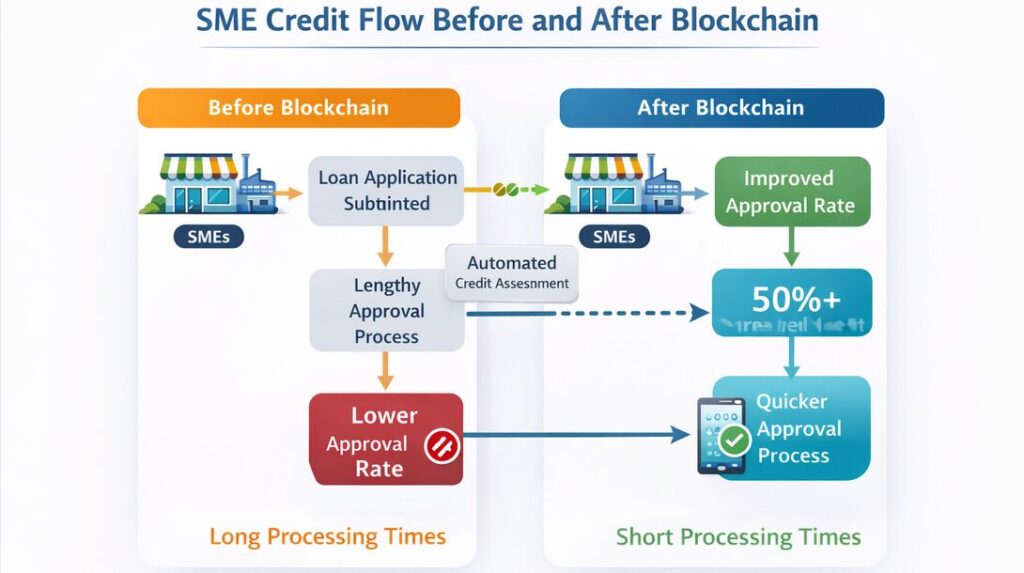

SME Credit Flow Before and After Blockchain

(Description: Flowchart showing improved approval rates and reduced processing time.)

Policy Context: Blockchain vs Cryptocurrency in China

It is crucial to understand that China’s blockchain strategy operates independently from its stance on cryptocurrencies.

Since 2021, China has banned cryptocurrency trading and mining. However, it has simultaneously accelerated investment in blockchain as a core infrastructure technology.

This dual approach reflects a broader philosophy:

- Blockchain = Infrastructure (Encouraged)

- Cryptocurrency = Speculation (Restricted)

The current directive reinforces this distinction. By promoting blockchain in financial administration, China is positioning itself as a leader in enterprise and government blockchain applications—without embracing open, permissionless crypto systems.

China’s Dual Policy Framework

(Description: Split diagram showing “Blockchain Infrastructure Growth” vs “Crypto Restrictions.”)

Global Context: A Growing Trend in Institutional Blockchain Adoption

China is not alone in exploring blockchain for financial infrastructure. Globally, several trends are emerging:

1. Central Bank Digital Currencies (CBDCs)

Countries are experimenting with digital currencies that leverage blockchain or distributed ledger technologies.

2. Tokenized Assets

Financial institutions are tokenizing bonds, equities, and real-world assets to improve liquidity and settlement efficiency.

3. Embedded Finance and Open Banking

APIs and data-sharing frameworks are enabling seamless financial services integration across platforms.

4. On-Chain Credit Scoring

Projects are emerging that use blockchain data—such as transaction histories—to assess creditworthiness.

China’s Bank–Tax blockchain initiative fits squarely within this global movement, but with a unique focus on government-driven data integration.

Global Blockchain Finance Landscape

(Description: Map showing CBDCs, tokenization hubs, and blockchain adoption regions.)

Implications for Crypto Investors and Builders

For those seeking new opportunities in the crypto and blockchain space, this development offers several insights:

1. Real Value Lies in Infrastructure

Speculative tokens may dominate headlines, but long-term value is being built in systems that solve real problems—like SME financing.

2. Enterprise Blockchain Is Expanding

Permissioned blockchain systems are gaining traction among governments and financial institutions.

3. Data Is the New Collateral

In the future, verified data—tax records, transaction histories, behavioral metrics—may replace traditional collateral.

4. Interoperability Opportunities

Projects that can bridge traditional finance and blockchain systems will be in high demand.

5. Compliance-First Models Are Emerging

Regulatory alignment is becoming a competitive advantage, not a constraint.

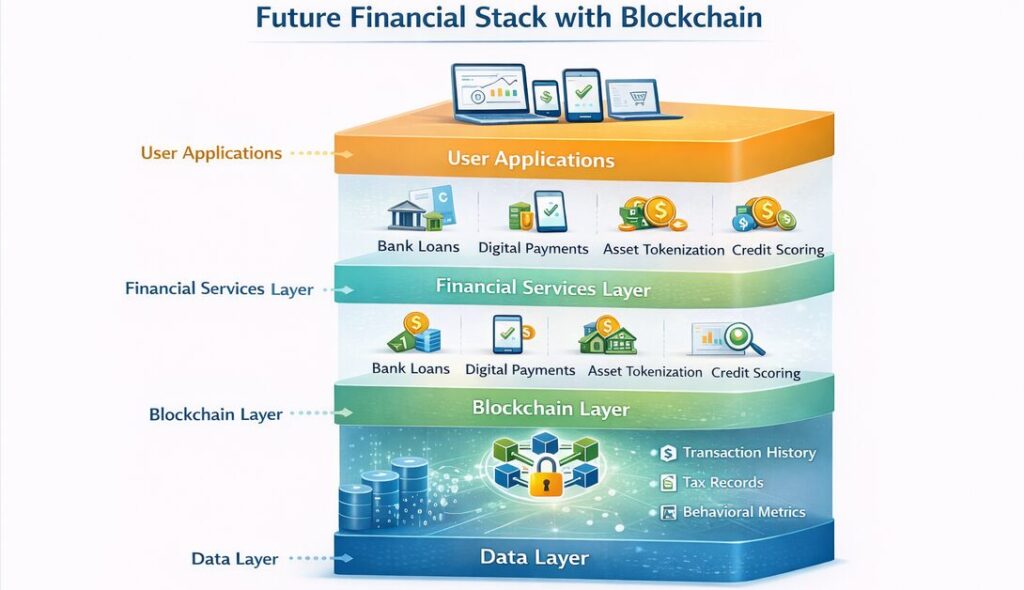

Future Financial Stack with Blockchain

(Description: Layered architecture showing data, blockchain, financial services, and user applications.)

Challenges and Risks

Despite its promise, the initiative is not without challenges:

- Data Privacy Risks: Even with encryption, large-scale data sharing raises concerns

- Standardization Complexity: Aligning data formats across institutions is difficult

- Adoption Barriers: Banks and SMEs must adapt to new systems

- Centralization Concerns: Permissioned systems may limit transparency

These factors will determine how effectively the policy translates into real-world impact.

Conclusion: A Blueprint for the Future of Finance

China’s push to integrate blockchain into its Bank–Tax Interaction model is more than a domestic policy update—it is a blueprint for the future of financial infrastructure.

By combining trusted government data with secure, decentralized technologies, the initiative addresses one of the most fundamental inefficiencies in finance: the gap between information and trust.

For SMEs, this could mean faster access to capital.

For banks, better risk management.

For the blockchain industry, a clear signal that real-world adoption is accelerating.

As global financial systems continue to evolve, the convergence of data, regulation, and blockchain technology will define the next generation of economic activity.