Key Points :

- Coinbase partners with Better to launch crypto-backed home mortgages

- Borrowers can use BTC and USDC as collateral without liquidation

- Backed by Fannie Mae, enhancing credibility

- First regulated mortgage product integrating crypto collateral at this level

- Preserves upside exposure to crypto assets while enabling home ownership

- Signals convergence between traditional finance and blockchain-based capital

Introduction: A Structural Shift in Finance

The announcement by Coinbase on March 26, 2026, marks a pivotal moment in the evolution of both real estate finance and the cryptocurrency industry. By collaborating with Better, Coinbase is enabling a new type of mortgage product that allows borrowers to use crypto assets—specifically Bitcoin (BTC) and USDC—as collateral without needing to sell them.

This innovation is not merely a new financial product. It represents a structural convergence between decentralized finance (DeFi)-inspired asset models and regulated, government-backed financial systems. The involvement of Fannie Mae adds a layer of institutional legitimacy that has long been absent in crypto-collateralized lending.

For readers seeking new crypto income strategies and real-world blockchain applications, this development deserves close attention.

1. Crypto as Collateral: Unlocking Dormant Capital

Traditionally, purchasing a home requires liquid capital for a down payment. For crypto holders, this has meant selling assets—often triggering tax events and forfeiting future gains.

Coinbase’s new mortgage model changes that paradigm.

Borrowers can pledge Bitcoin or USDC held in their Coinbase accounts as collateral. This allows them to:

- Maintain exposure to Bitcoin’s potential price appreciation

- Continue earning yield or rewards on stablecoins like USDC

- Avoid taxable liquidation events

This model effectively transforms crypto from a speculative asset into productive collateral, aligning it with traditional financial assets like equities or bonds.

In practical terms, a borrower holding $500,000 worth of Bitcoin could use that value as collateral to secure a mortgage—without selling a single satoshi.

2. The Role of Fannie Mae: Institutional Validation

One of the most important aspects of this initiative is its backing by Fannie Mae.

Fannie Mae plays a central role in the U.S. housing finance system by purchasing mortgages from lenders and packaging them into mortgage-backed securities (MBS). Its involvement signals that this crypto-backed mortgage product meets regulatory and risk standards comparable to traditional mortgages.

This is a major milestone because:

- It bridges crypto with government-supported financial infrastructure

- It provides legal protections similar to conventional home loans

- It reduces perceived risk for both lenders and borrowers

Historically, crypto lending has largely operated in unregulated or lightly regulated environments. This move represents a transition into fully compliant, systemically integrated finance.

3. Coinbase’s Strategy: From Exchange to Financial Platform

Coinbase has been steadily expanding beyond simple trading services.

This mortgage initiative aligns with a broader strategy:

- Integrating crypto into everyday financial activities

- Building a “full-stack” financial ecosystem

- Increasing user retention through utility-driven services

The inclusion of benefits for Coinbase One subscribers—such as potential rebates—further reinforces this ecosystem approach.

Rather than positioning itself solely as a marketplace, Coinbase is evolving into a crypto-native financial institution, competing with banks, brokers, and fintech platforms simultaneously.

4. Market Context: The Rise of Asset-Backed Crypto Finance

This development fits into a broader trend: the emergence of asset-backed financial models in crypto.

In recent years, we have seen:

- Crypto-backed loans from platforms like BlockFi (before its collapse)

- Institutional custody solutions enabling collateralization

- Tokenization of real-world assets (RWAs) such as real estate and bonds

However, most of these efforts lacked regulatory integration.

Coinbase’s approach is different because it combines:

- On-chain asset ownership

- Off-chain legal enforceability

- Government-backed financial structures

This hybrid model aligns closely with what could be described as an “Asset-Backed Representation” framework—where blockchain assets are integrated into traditional financial systems without fully replacing them.

5. Risk Considerations: Volatility and Liquidation

Despite its promise, crypto-backed mortgages introduce new risks.

Price Volatility

Bitcoin’s price can fluctuate significantly. If the value of the collateral drops below a certain threshold, borrowers may face:

- Margin calls

- Forced liquidation of their crypto assets

Liquidity Constraints

In extreme market conditions, liquidity could become constrained, affecting both collateral valuation and loan stability.

Regulatory Evolution

Although backed by Fannie Mae, the regulatory landscape for crypto remains dynamic. Future changes could impact:

- Eligibility criteria

- Collateral requirements

- Tax treatment

Understanding these risks is critical for both retail and institutional participants.

6. Economic Implications: Expanding Credit Access

This model has broader macroeconomic implications.

By allowing crypto holders to access credit without liquidation, it:

- Increases capital efficiency

- Expands access to home ownership

- Unlocks trillions of dollars in dormant crypto wealth

In markets like the United States, where housing affordability remains a challenge, alternative collateral models could significantly reshape lending dynamics.

Moreover, this approach could extend beyond mortgages to:

- Business loans

- Personal credit lines

- Cross-border financing

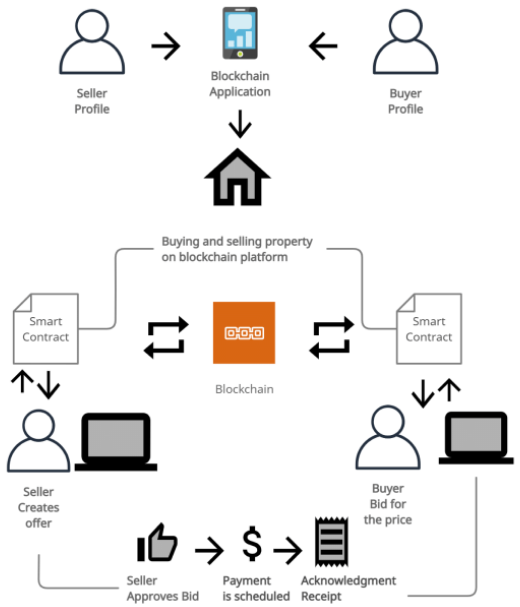

7. Visual Model: How Crypto-Backed Mortgages Work

[Crypto Mortgage Flow Diagram]

Explanation:

The diagram illustrates how a borrower deposits BTC/USDC as collateral, secures a mortgage through Better, and receives legal protections via Fannie Mae-backed structures.

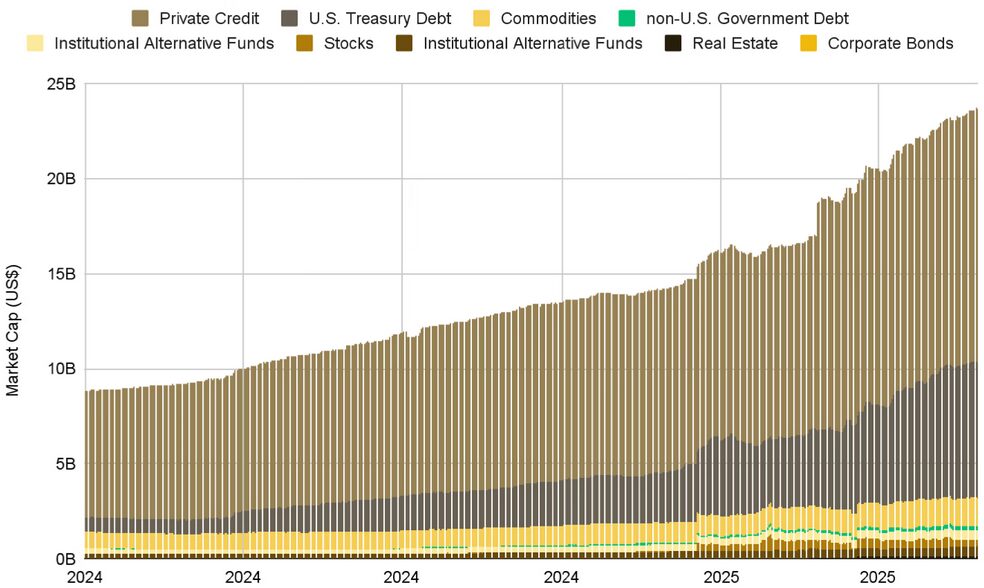

8. Market Trend Visualization: Growth of Crypto Collateralization

[Growth of Crypto-Backed Lending]

Explanation:

This chart highlights the rapid expansion of crypto-backed lending and the transition toward regulated financial integration.

9. Comparative Framework: Traditional vs Crypto Mortgage

[Comparison Table Visualization]

Explanation:

This comparison shows how crypto mortgages differ in collateral type, liquidity preservation, and exposure to market volatility.

Conclusion: A Turning Point for Financial Architecture

The introduction of crypto-backed mortgages by Coinbase, in partnership with Better and supported by Fannie Mae, represents more than a new product—it signals a fundamental shift in financial architecture.

This model demonstrates that crypto can move beyond speculation into core economic infrastructure, enabling:

- Real-world utility

- Capital efficiency

- Institutional integration

For investors and builders alike, the implications are profound. The boundary between traditional finance and blockchain systems is no longer theoretical—it is operational.