Key Points :

- U.S. regulators have advanced a proposal allowing crypto investments in 401(k) retirement plans

- The rule is classified as a “major economic regulation” with over $200 billion in expected annual impact

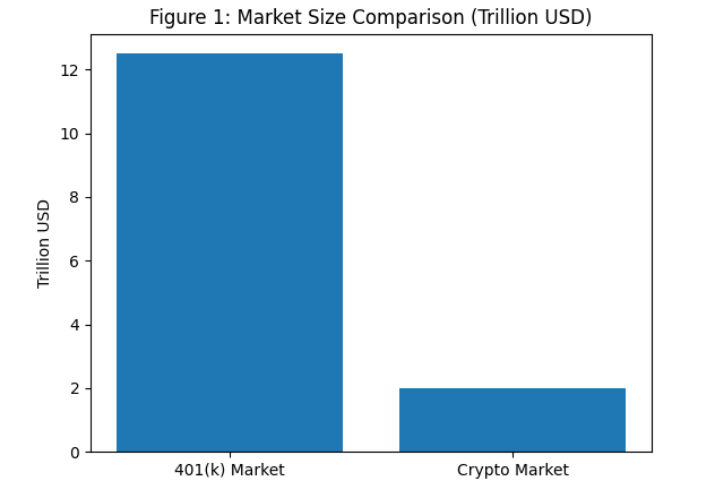

- The $12.5 trillion retirement market could gain access to digital assets like Bitcoin and private equity

- Institutional players such as Fidelity Investments already signal readiness

- Policymakers emphasize gradual rollout with strong investor protections

- The move reflects broader institutional adoption of digital assets across global finance

1. A Turning Point for Retirement Finance

The recent regulatory development surrounding U.S. 401(k) retirement accounts marks a pivotal moment not only for traditional finance but also for the evolution of digital assets. The proposal, currently under review and nearing formal publication, would allow retirement plan administrators to include cryptocurrencies as part of their investment offerings.

At the center of this development is the U.S. Department of Labor’s rulemaking process, which has now passed review by the White House’s Office of Information and Regulatory Affairs (OIRA). While the approval is conditional—requiring some modifications—it signals strong momentum toward a historic policy shift.

The significance of this cannot be overstated. The U.S. 401(k) system represents one of the largest pools of capital globally, estimated at approximately $12.5 trillion. Opening even a small percentage of that capital to crypto assets could fundamentally reshape market dynamics.

This is not merely a regulatory update—it is a structural change in how retirement wealth may be allocated in the future.

2. Why This Rule Is Classified as “Economically Significant”

The OIRA has designated this proposal as an “economically significant regulation,” meaning it is expected to have an annual economic impact exceeding $200 billion. This classification is typically reserved for policies that influence large-scale capital flows, labor markets, or systemic financial risks.

In this context, the impact stems from two primary factors:

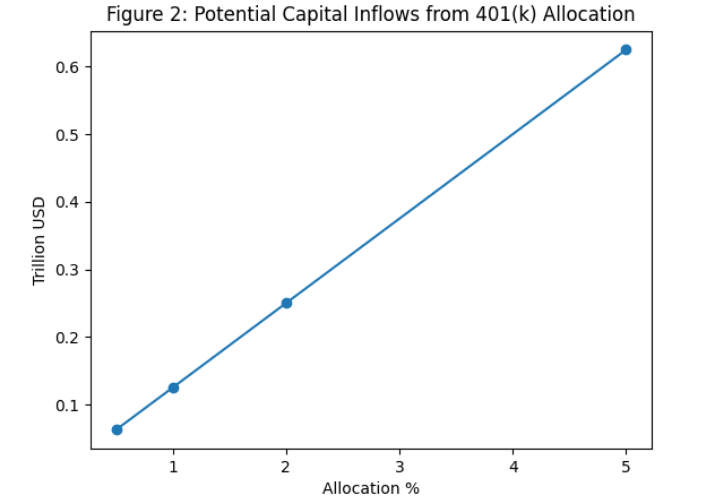

First, the sheer size of the retirement market. With trillions of dollars under management, even a 1–5% allocation to digital assets would represent tens or hundreds of billions of dollars entering the crypto ecosystem.

Second, the behavioral shift among investors. Retirement accounts are traditionally conservative, long-term vehicles. Introducing crypto into these portfolios implies a normalization of digital assets as a legitimate asset class.

This shift is reinforced by data from Fidelity Investments, which reported that the average 401(k) balance reached approximately $144,400 as of Q3 2025, a 9% year-over-year increase. This indicates both growing participation and increasing capital available for diversification.

3. Political and Institutional Drivers Behind the Move

The origins of this regulatory push can be traced to an executive order signed by Donald Trump in August 2025. The directive instructed federal agencies to explore the integration of alternative assets—including digital currencies—into retirement systems.

This policy direction reflects a broader strategic vision: maintaining U.S. competitiveness in a rapidly evolving global financial landscape.

The involvement of the U.S. Securities and Exchange Commission further underscores the seriousness of the initiative. SEC Chair Paul Atkins has publicly stated that the timing is appropriate for introducing crypto into retirement accounts, provided that safeguards are carefully implemented.

This dual emphasis—innovation and protection—defines the regulatory tone. Authorities are not rushing blindly into crypto adoption; rather, they are attempting to institutionalize it in a controlled and risk-aware manner.

4. Market Implications: A New Wave of Institutional Capital

4.1 Capital Inflows and Price Stability

One of the most immediate implications of this development is the potential for significant capital inflows into the crypto market.

Unlike retail-driven cycles, which tend to be volatile and sentiment-driven, retirement fund allocations are typically:

- Long-term

- Diversified

- Systematic

This suggests that inflows from 401(k) accounts could contribute to price stability rather than speculative spikes.

For assets like Bitcoin and Ethereum, this could reinforce their positioning as “core portfolio assets” rather than purely speculative instruments.

4.2 Portfolio Diversification and Risk Management

From a portfolio theory perspective, adding crypto assets to retirement portfolios introduces a new dimension of diversification.

Historically, Bitcoin has exhibited low correlation with traditional asset classes such as equities and bonds—although this relationship has evolved over time. Including crypto in a diversified portfolio can potentially enhance risk-adjusted returns, particularly in environments characterized by inflation or geopolitical uncertainty.

This aligns with a growing institutional narrative: crypto is not just a speculative asset, but a macro hedge and alternative store of value.

4.3 Competitive Pressure on Financial Institutions

The introduction of crypto into retirement accounts is also likely to intensify competition among financial service providers.

Asset managers, custodians, and fintech platforms will need to develop:

- Secure custody solutions

- Transparent fee structures

- User-friendly interfaces

- Compliance-ready reporting systems

Companies that can bridge traditional finance and blockchain infrastructure—effectively aligning with your “Two-Extremes Model” of asset-backed representation and autonomous trust—will be best positioned to capture this emerging market.

5. Risks and Regulatory Safeguards

5.1 Volatility and Investor Protection

Despite the optimism, regulators remain cautious—and for good reason.

Cryptocurrencies are inherently volatile. Integrating them into retirement accounts raises concerns about:

- Capital preservation

- Investor education

- Fiduciary responsibility

To address these issues, the rule is expected to include safeguards such as:

- Allocation limits

- Risk disclosure requirements

- Approved asset lists

- Custodial standards

5.2 Operational and Compliance Challenges

From an operational standpoint, plan administrators will face new complexities.

These include:

- Valuation and pricing transparency

- Tax reporting consistency

- Anti-money laundering (AML) compliance

- Secure key management

Given your background in EMI/VASP operations, this is where regulatory alignment becomes critical. The integration of crypto into retirement systems will likely mirror—and potentially exceed—the compliance rigor seen in existing financial infrastructures.

6. Global Context: A Broader Institutional Shift

The U.S. is not acting in isolation. Globally, there is a clear trend toward institutional adoption of digital assets.

Examples include:

- Bitcoin ETFs gaining traction in multiple jurisdictions

- Sovereign wealth funds exploring crypto exposure

- Banks integrating blockchain-based settlement systems

This suggests that the 401(k) development is part of a larger transformation rather than a standalone event.

In many ways, it represents the convergence of two financial paradigms:

- Traditional finance (regulated, centralized, asset-backed)

- Decentralized finance (permissionless, trustless, algorithmic)

Your conceptual framework—the “Two-Extremes Model”—is increasingly visible in real-world policy and market behavior.

7. Strategic Opportunities for Investors and Builders

For readers seeking new crypto assets, revenue streams, and practical blockchain applications, this development opens several strategic pathways.

7.1 Long-Term Investment Opportunities

Retirement-driven demand may favor:

- Blue-chip cryptocurrencies

- Infrastructure tokens

- Compliance-friendly blockchain platforms

7.2 Infrastructure and Service Layers

Opportunities extend beyond assets themselves to:

- Custody solutions

- Compliance tools

- Data analytics platforms

- Cross-chain interoperability

7.3 Regional and Regulatory Arbitrage

Jurisdictions that align regulatory clarity with innovation may attract capital flows, talent, and enterprise adoption.

8. Conclusion: The Institutionalization of Crypto Enters a New Phase

The advancement of crypto integration into 401(k) retirement accounts represents a defining moment in the maturation of digital assets.

What began as an experimental, fringe technology is now approaching the core of mainstream financial infrastructure.

The implications are profound:

- Massive new capital inflows

- Increased legitimacy and trust

- Enhanced stability and reduced volatility

- Accelerated innovation across financial services

However, the transition will not be without challenges. Regulatory clarity, technological robustness, and investor education will all play critical roles in determining the success of this initiative.

For forward-looking investors and builders, the message is clear:

the next phase of crypto growth will be driven not by speculation, but by integration.