Key Points :

- Dollar-denominated stablecoins are expanding rapidly across multiple jurisdictions

- The Financial Stability Board warns of serious risks to emerging economies

- Risks include currency substitution, weakened monetary policy, and capital control bypass

- Despite growth, real-economy adoption remains limited

- Regulators are prioritizing systemic risk monitoring and global coordination in 2026

1. Introduction: The Rise of Dollar Stablecoins and Global Concern

The rapid growth of dollar-denominated stablecoins has become one of the most transformative developments in the global financial system. Initially designed as a bridge between traditional finance and blockchain ecosystems, stablecoins have evolved into a parallel monetary layer—particularly in regions with unstable currencies.

However, this evolution has triggered growing concern among global regulators. The Financial Stability Board, established in the aftermath of the 2008 financial crisis, has recently issued a stark warning: dollar-backed stablecoins could pose systemic risks to emerging and developing economies.

Unlike developed markets where financial systems are deep and resilient, emerging markets are more vulnerable to external monetary influences. The increasing circulation of dollar-denominated digital assets introduces a new dimension of financial instability—one that is decentralized, borderless, and difficult to regulate.

2. Core Risks Identified by the FSB

The FSB outlines several critical risks associated with the widespread adoption of foreign-currency stablecoins:

2.1 Currency Substitution (“Digital Dollarization”)

One of the most immediate risks is currency substitution, where local populations begin using stablecoins instead of domestic currencies. This phenomenon—often called “digital dollarization”—can undermine national sovereignty over monetary systems.

In countries experiencing inflation or currency depreciation, stablecoins pegged to the US dollar become attractive stores of value. While this may offer short-term stability for individuals, it reduces demand for local currency, potentially accelerating its decline.

2.2 Weakening of Monetary Policy

Central banks rely on tools such as interest rates and liquidity controls to manage economic stability. However, when a significant portion of economic activity shifts to stablecoins, these tools lose effectiveness.

For example, if consumers and businesses transact primarily in dollar stablecoins, central banks cannot easily influence credit conditions or money supply. This erosion of policy effectiveness is a major concern highlighted by the FSB.

2.3 Decline in Domestic Payment Systems

The adoption of stablecoins can reduce reliance on domestic payment infrastructure. While blockchain-based systems may offer efficiency, they also bypass regulated financial institutions.

This leads to:

- Reduced transaction volumes in domestic systems

- Lower fee revenues for local banks

- Potential weakening of financial infrastructure

2.4 Capital Flow and Regulatory Arbitrage

Stablecoins enable near-instant cross-border transfers, which can bypass capital controls imposed by governments. This creates a channel for unregulated capital outflows, increasing volatility in already fragile economies.

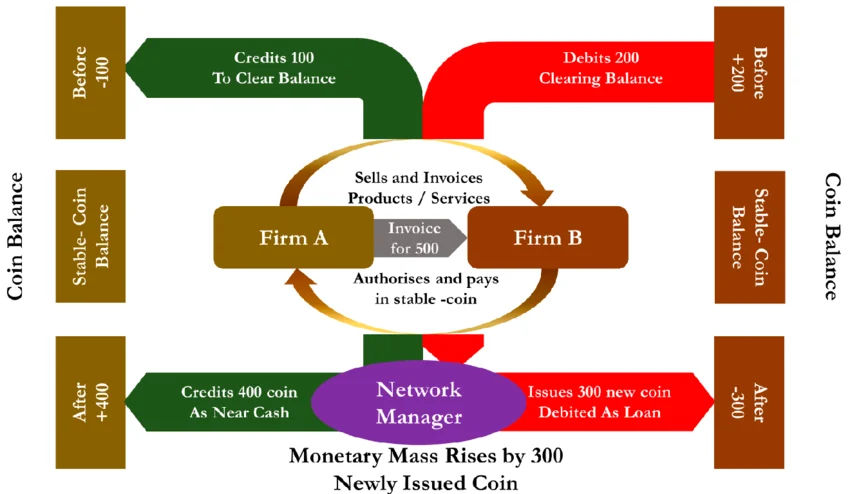

3. Structural Vulnerabilities in the Stablecoin Ecosystem

Beyond macroeconomic risks, the FSB also emphasizes systemic vulnerabilities within the stablecoin ecosystem itself:

- Liquidity Risk: Sudden redemption waves could destabilize issuers

- Operational Risk: Smart contract failures or infrastructure outages

- Interconnectedness: Growing links with traditional finance amplify contagion risk

As stablecoins become more integrated with banks, payment providers, and fintech platforms, the potential for systemic spillover increases.

4. Limited Real-Economy Adoption

Despite rapid market expansion, the FSB notes that stablecoins are still not widely used in real economic activities such as payments for goods and services.

Instead, their primary use cases remain:

- Crypto trading and liquidity provision

- DeFi collateral and yield generation

- Cross-border remittances (limited but growing)

This gap between market growth and real-world utility suggests that stablecoins are still largely financial instruments rather than true payment solutions.

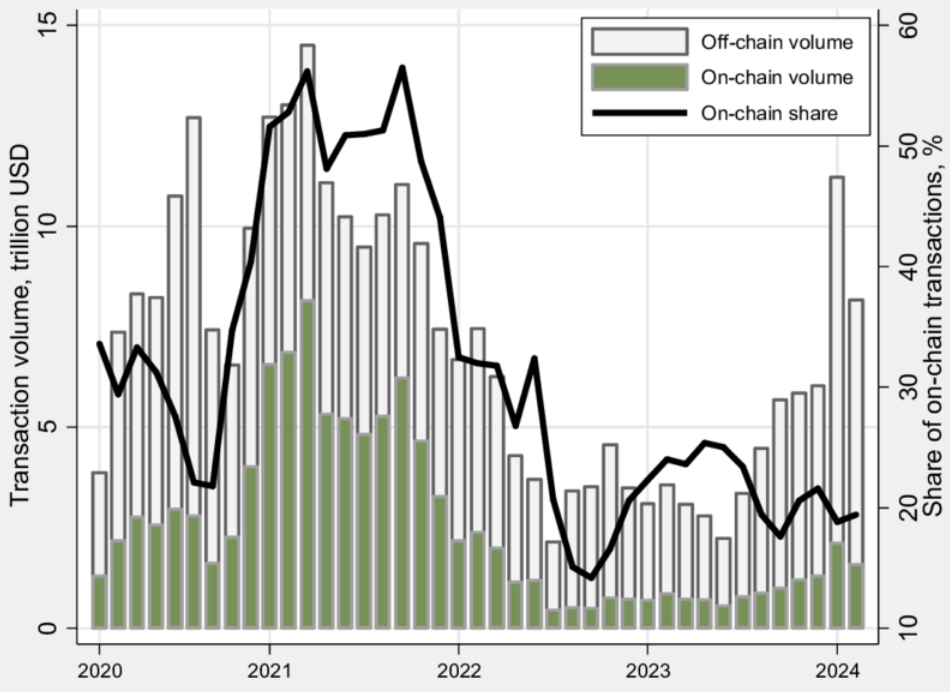

Global Crypto Market Capitalization and Monthly Trading Volume

5. Regulatory Gaps and Global Coordination Challenges

The FSB’s report builds upon its 2023 global regulatory framework for crypto assets and stablecoins. While the framework was updated in 2025, significant implementation gaps remain across jurisdictions.

Key challenges include:

- Inconsistent regulatory definitions

- Lack of cross-border supervision

- Fragmented compliance standards

This inconsistency creates opportunities for regulatory arbitrage, where issuers operate in less restrictive jurisdictions while serving global users.

6. 2026 Priorities: Monitoring and Modernization

Looking ahead, the FSB has outlined several priorities for 2026:

6.1 Enhanced Monitoring of Stablecoin Risks

Regulators will focus on tracking:

- Liquidity conditions

- Redemption mechanisms

- Systemic linkages

6.2 Digital Innovation Oversight

Emerging technologies such as tokenized assets and blockchain-based payment systems will be closely evaluated.

6.3 Strengthening Crisis Response Frameworks

Given the potential for rapid contagion, authorities aim to improve:

- Early warning systems

- Cross-border coordination

- Emergency liquidity tools

Interconnected Risks in the Stablecoin Ecosystem

7. Emerging Trends Beyond the Report

Recent developments reinforce the FSB’s concerns:

7.1 Institutional Stablecoin Expansion

Major financial institutions are exploring stablecoin issuance, increasing integration with traditional finance.

7.2 CBDC Acceleration

Central banks are accelerating Central Bank Digital Currency (CBDC) projects as alternatives to private stablecoins.

7.3 Regulatory Tightening

Regions such as the EU (MiCA) and Asia are implementing stricter stablecoin regulations, signaling a global shift toward oversight.

8. Strategic Implications for Investors and Builders

For readers seeking new crypto opportunities, this evolving landscape presents both risks and opportunities:

Opportunities

- Infrastructure for compliant stablecoin issuance

- Cross-border payment solutions with regulatory alignment

- Blockchain analytics and risk monitoring tools

Risks

- Regulatory crackdowns

- Reduced yields in DeFi due to compliance costs

- Fragmentation of global liquidity

Projects that align with regulatory expectations while maintaining decentralization advantages are likely to dominate the next phase.

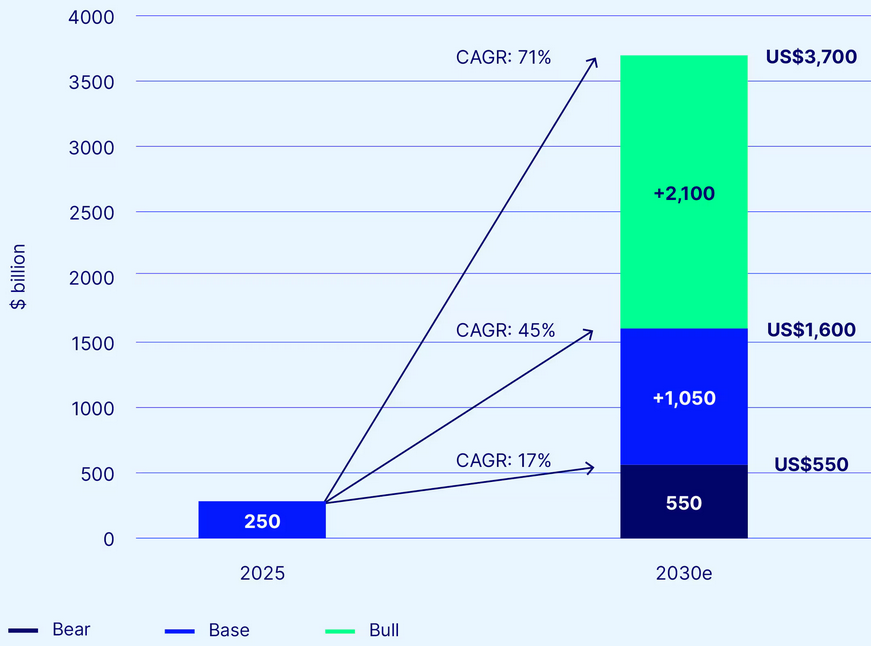

Projected Growth of Regulated Crypto Financial Markets

9. Conclusion

The FSB’s warning marks a pivotal moment in the evolution of stablecoins. While these digital assets offer undeniable advantages—efficiency, accessibility, and global reach—they also introduce systemic risks that cannot be ignored, particularly in emerging markets.

The future of stablecoins will likely be shaped by a delicate balance between innovation and regulation. For investors, developers, and policymakers, understanding this balance is critical.

Stablecoins are no longer مجرد tools for crypto trading—they are becoming a core component of the global financial architecture. Whether they evolve into a stabilizing force or a source of instability will depend on how effectively risks are managed in the years ahead.