Key Points :

- The European Central Bank is accelerating technical rulemaking for the digital euro, focusing on real-world usability such as ATMs and POS terminals.

- New working groups are defining offline payments, device compatibility, and transaction processing standards.

- The digital euro remains pending political approval, with a possible launch target around 2029.

- Meanwhile, private-sector initiatives like the Qivalis project aim to launch euro-backed stablecoins as early as 2026.

- The competition between CBDCs and stablecoins is intensifying globally, shaping the future of programmable money and financial infrastructure.

1. The Digital Euro Enters the Implementation Phase

The push toward a digital euro has moved beyond theoretical discussions and into a concrete implementation phase. The European Central Bank (ECB) is now actively recruiting experts and forming working groups to define how the digital euro will function in everyday financial environments.

Unlike earlier conceptual discussions centered on monetary policy implications, the current phase is deeply technical and operational. The ECB is focusing on how the digital euro can be seamlessly integrated into existing financial infrastructure, particularly ATMs and retail payment terminals. This marks a significant shift from vision to execution.

The importance of this step cannot be overstated. For any central bank digital currency (CBDC) to succeed, it must function not just as a digital ledger entry but as a practical payment tool that users can interact with in familiar ways. By targeting ATMs and POS devices, the ECB is signaling that the digital euro is intended to behave similarly to cash and card payments, rather than existing as a niche digital asset.

From a broader perspective, this reflects a key lesson learned from the adoption of cryptocurrencies and stablecoins: usability drives adoption. Even the most technically advanced digital currency will fail if it cannot integrate into daily life.

2. ATM Integration and POS Compatibility: Bridging Old and New Finance

One of the most notable aspects of the ECB’s current initiative is its emphasis on ATM functionality. This suggests that users may eventually be able to withdraw digital euros into physical cash or vice versa, or even manage digital euro balances directly through ATM interfaces.

[“Digital Euro ATM Interaction Flow”]

Figure 1 Description:

A flow diagram showing how a user interacts with an ATM:

Wallet → Authentication → Digital Euro Balance → Conversion (Cash ↔ Digital) → Confirmation

This hybrid approach is crucial. It acknowledges that while digital payments are growing rapidly, cash still plays an essential role in many economies. By enabling interoperability between digital and physical forms of money, the ECB is attempting to future-proof the euro system without alienating existing users.

Additionally, compatibility with point-of-sale (POS) terminals ensures that merchants can accept digital euro payments without significant infrastructure upgrades. This reduces friction for adoption and aligns with how card networks like Visa and Mastercard historically scaled payment innovations.

From a technical standpoint, this requires defining:

- Transaction authorization protocols

- Settlement timing (instant vs delayed)

- Interoperability with existing card networks

- Security standards for both online and offline environments

The ECB’s working groups are tasked with addressing these complexities, effectively designing a new financial layer that sits atop—or alongside—existing systems.

3. Offline Payments: A Critical Feature for Financial Resilience

A particularly important feature under development is offline payment capability. This allows transactions to occur without an active internet connection, a capability that is essential for:

- Rural or low-connectivity regions

- Emergency situations (e.g., natural disasters)

- Privacy-conscious users

[“Offline vs Online CBDC Transaction Model”]

Figure 2 Description:

Two parallel flows:

- Online: User → Bank/Node → Validation → Settlement

- Offline: User → Device-to-Device → Local Validation → Later Synchronization

Offline functionality is one of the most challenging aspects of CBDC design. It requires balancing security, double-spending prevention, and user privacy. Unlike blockchain-based systems such as Bitcoin, which rely on network-wide consensus, offline CBDC transactions must rely on trusted hardware or pre-authorized value storage.

This is where the digital euro diverges significantly from decentralized cryptocurrencies. While Bitcoin emphasizes trustless verification, the digital euro will likely rely on centralized oversight combined with secure device-level controls.

For investors and builders, this highlights an important trend: future digital money systems will not be purely decentralized or centralized, but hybrid architectures combining both approaches.

4. Certification, Compliance, and Infrastructure Governance

Another working group is focused on certification processes for devices and infrastructure. This includes ensuring that:

- Payment terminals meet security standards

- Wallet applications comply with regulatory requirements

- Financial institutions integrate correctly with ECB systems

This layer of governance is critical, especially in a highly regulated environment like the European Union. Unlike permissionless systems, the digital euro will operate within a strict compliance framework, including anti-money laundering (AML) and know-your-customer (KYC) requirements.

For fintech companies and VASPs (Virtual Asset Service Providers), this represents both a challenge and an opportunity. Integration with CBDC systems may require:

- Enhanced compliance capabilities

- New API integrations

- Participation in certification programs

However, it also opens the door to direct interaction with central bank infrastructure, potentially reducing reliance on intermediary banks.

5. The Stablecoin Challenge: Qivalis and the Private Sector Response

While the ECB advances its CBDC initiative, the private sector is not standing still. The Qivalis project, backed by a consortium of 12 European banks, aims to launch a euro-pegged stablecoin by 2026.

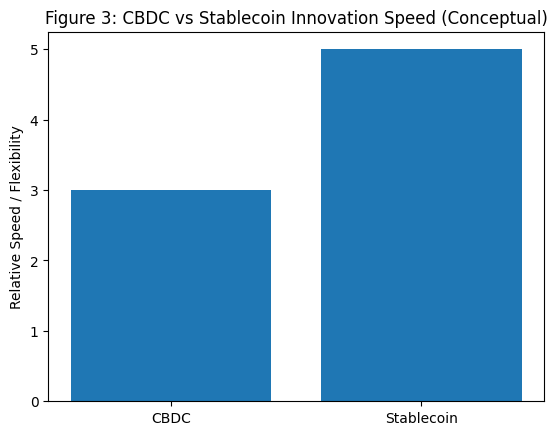

[“CBDC vs Stablecoin Competitive Landscape”]

Figure 3 Description:

Comparison chart:

- CBDC: Centralized, regulated, sovereign-backed

- Stablecoin: Private, flexible, faster to market

This creates a competitive dynamic:

| Feature | Digital Euro (CBDC) | Euro Stablecoins |

|---|---|---|

| Issuer | Central Bank | Private Entities |

| Launch Timeline | ~2029 | ~2026 |

| Regulation | High | Medium-High |

| Innovation Speed | Slower | Faster |

| Trust Model | Sovereign | Market-based |

Stablecoins have already demonstrated strong product-market fit, particularly in cross-border payments and decentralized finance (DeFi). Projects like USDC and USDT have shown that programmable money can scale rapidly when it meets real user needs.

The ECB’s challenge is clear: deliver a CBDC that is competitive with private-sector innovation while maintaining regulatory integrity.

6. Global Context: A Race Toward Programmable Money

The digital euro is part of a broader global movement toward programmable, digital-native currencies. Countries like China with its digital yuan and ongoing discussions in the United States and Japan highlight a growing consensus: the future of money will be digital.

However, the form that this digital money takes is still being defined. The key questions include:

- Will CBDCs dominate, or will stablecoins lead?

- How will interoperability between systems be achieved?

- What role will blockchain play versus traditional databases?

For readers interested in new crypto assets and revenue opportunities, this transition represents a once-in-a-generation shift in financial infrastructure. Opportunities may emerge in:

- Payment gateways and APIs

- Compliance and identity solutions

- Cross-border settlement layers

- Hybrid CBDC–crypto interoperability platforms

Conclusion: Convergence, Competition, and Opportunity

The ECB’s latest move signals that the digital euro is no longer a distant concept—it is becoming a tangible component of future financial systems. By focusing on ATM integration, offline functionality, and infrastructure certification, the ECB is addressing the practical realities of adoption.

At the same time, the rise of private-sector initiatives like Qivalis underscores a fundamental truth: the future of money will be shaped by both public and private innovation.

Rather than a zero-sum competition, we are likely to see a convergent model, where CBDCs provide stability and trust, while stablecoins and crypto networks drive innovation and flexibility.

For investors, developers, and institutions, the key is to position themselves at the intersection of these trends—where regulation meets innovation, and where traditional finance merges with blockchain technology.