Key Points :

- Kenya has opened public consultation for its Virtual Asset Service Providers Regulations 2026, signaling imminent enforcement

- Clear rules introduced on licensing, stablecoin reserves, audits, and transaction fees

- Regulatory responsibilities split between Central Bank of Kenya and Capital Markets Authority

- Rapid market growth (~$19 billion inflow, 6+ million users) is driving regulatory urgency

- Kenya may become a model framework for emerging markets and compliant crypto ecosystems

1. Introduction: Kenya Moves from Adoption to Regulation

Kenya, long recognized as one of Africa’s most dynamic digital finance markets, is now entering a decisive phase in its crypto evolution. With the Ministry of Finance opening public comments on the Virtual Asset Service Providers Regulations 2026, the country is transitioning from organic adoption to structured governance.

This move is not merely procedural. It reflects a broader global trend: jurisdictions that once tolerated or cautiously observed cryptocurrency are now formalizing regulatory frameworks to capture economic value, ensure consumer protection, and integrate blockchain into national financial systems.

The consultation period, which runs until April 10, 2026, provides stakeholders with a final opportunity to shape the regulatory environment before full implementation. Public forums scheduled across multiple regions further reinforce Kenya’s intention to build an inclusive and practical regulatory regime.

2. Regulatory Architecture: Multi-Agency Oversight and Defined Roles

A notable feature of Kenya’s approach is its multi-agency regulatory structure, designed to reflect the hybrid nature of digital assets.

- The Central Bank of Kenya (CBK) will oversee:

- Stablecoin issuers

- Payment and settlement services

- The Capital Markets Authority (CMA) will supervise:

- Exchanges

- Brokers

- Token issuance platforms

This division mirrors frameworks emerging in jurisdictions such as the EU (MiCA) and parts of Asia, where different financial authorities handle payment versus investment-related crypto activities.

Such a structure is particularly relevant for operators like EMI/VASP hybrid businesses (similar to WIBS PHP), where both payment flows and trading functionalities coexist. Kenya’s model implicitly acknowledges that crypto is not a single category but a multi-layered financial infrastructure.

3. Licensing Framework: Market Entry with Defined Accountability

The proposed regulations introduce a standardized licensing regime:

- Applicable to:

- Corporations

- Limited liability partnerships

- Key features:

- Approval timeline: within 90 days

- License validity: 12 months (renewable)

This is strategically significant. A relatively short license duration ensures ongoing regulatory oversight, while a clear approval timeline reduces uncertainty for market entrants.

From a strategic perspective, this creates both opportunity and constraint:

- Opportunity: Faster entry into a regulated market

- Constraint: Continuous compliance burden and renewal risk

For startups and international operators, Kenya becomes accessible—but not lightly regulated.

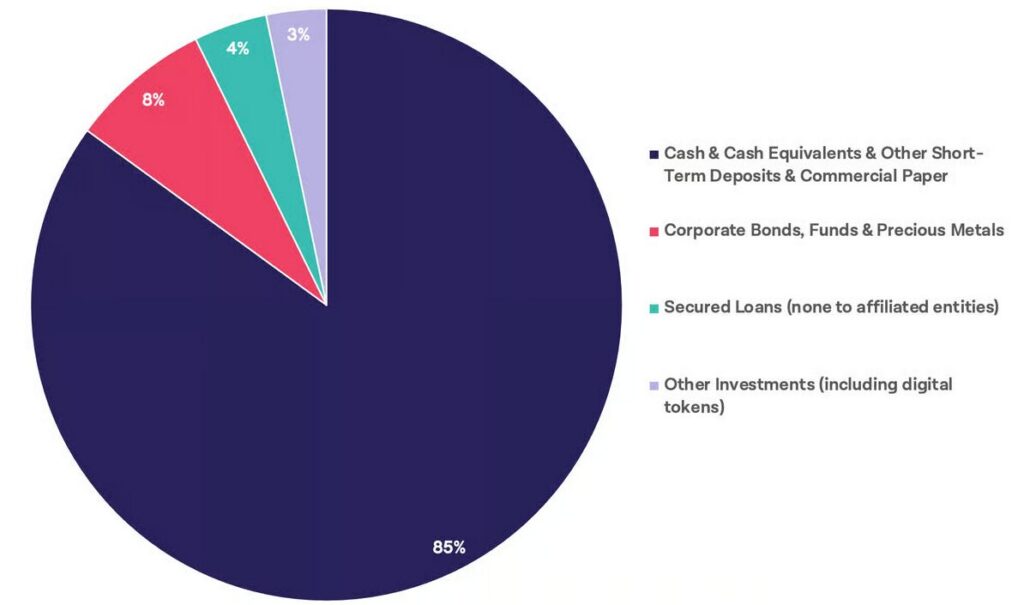

4. Stablecoin Regulation: A Conservative but Practical Reserve Model

One of the most important aspects of the draft regulation is its treatment of stablecoin reserves, which are increasingly central to global crypto infrastructure.

Key Requirements

- Minimum 30% of customer funds must be held in segregated accounts in Kenyan banks

- Remaining reserves must be allocated to low-risk assets such as:

- Short-term government securities

- Bank deposits

- Repurchase agreements (repos)

This hybrid reserve model is noteworthy.

It does not impose a strict 100% cash reserve requirement (as seen in some jurisdictions), but it still enforces a strong risk-control framework. This allows:

- Yield generation (through low-risk instruments)

- Liquidity assurance (through domestic bank holdings)

For stablecoin issuers, this creates a balanced capital efficiency model, albeit with operational complexity.

5. Compliance and Audit Requirements: Institutional-Grade Controls

The regulations emphasize operational integrity through strict compliance requirements:

- Mandatory local bank accounts

- System audits every two years, covering:

- Internal controls

- Data protection

- Cybersecurity

This aligns closely with global expectations for regulated financial institutions.

From a practical standpoint, this has several implications:

- Infrastructure must be audit-ready by design

- Logging, monitoring, and access control systems become critical

- Security frameworks must meet institutional standards, not startup-level practices

For organizations already building audit logs, AML frameworks, and internal controls (as you are doing), this is fully aligned with global regulatory direction.

6. Fee Structure: Embedded Regulatory Cost Model

The draft proposes explicit fee structures:

- 0.05% transaction fee charged to both parties on trading platforms

- 0.5% issuance fee on total token fundraising

These fees are effectively regulatory monetization mechanisms, ensuring that:

- Authorities capture value from market activity

- Compliance costs are partially internalized by platforms

From a business model perspective, this is critical:

- Platforms must integrate regulatory fees into pricing strategies

- Margins will be directly affected

- High-frequency trading models may face compression

This is similar to trends seen globally where compliance becomes a core cost center, not a peripheral expense.

7. Market Context: Why Kenya Is Moving Now

Kenya’s regulatory push is driven by undeniable market growth:

- Approx. $19 billion in crypto inflows (July 2024 – June 2025)

- Over 6 million users engaging in crypto activities

The country’s long-standing leadership in mobile money (e.g., M-Pesa) has naturally extended into crypto adoption. For many users, crypto is not speculative—it is functional infrastructure for payments, savings, and cross-border transfers.

Historically, regulators issued warnings (2015 CBK, 2018 CMA), but adoption continued regardless. This regulatory shift acknowledges a reality:

Crypto is no longer optional—it is already embedded in the economy.

8. Tax Evolution: From Transaction Tax to Service-Based Taxation

Kenya has also refined its taxation approach:

- 2023: 3% digital asset tax on transaction volume

- 2024 onward: Shift to 10% excise tax on service fees

This transition is significant.

The earlier model taxed gross transaction value, which:

- Discouraged trading activity

- Increased friction for users

The newer model taxes platform revenue instead, aligning incentives more effectively.

This mirrors global best practices and supports sustainable industry growth while still generating government revenue.

9. Global Implications: A Blueprint for Emerging Markets

Kenya’s framework has implications far beyond its borders.

Why This Matters Globally

- Provides a practical regulatory template for developing economies

- Balances innovation with control

- Integrates crypto into existing financial supervision structures

For regions like Southeast Asia, Latin America, and parts of Africa, Kenya’s model may serve as a reference architecture.

Relevance for Operators

For companies operating EMI/VASP models:

- Dual regulatory oversight (payments + trading) will become standard

- Stablecoin reserve requirements will tighten globally

- Audit and cybersecurity expectations will increase

In short, Kenya is not an outlier—it is part of a global convergence toward structured crypto regulation.

Kenya Crypto Market Growth vs Regulatory Timeline

(Visual: Timeline showing adoption growth vs regulatory milestones)

Stablecoin Reserve Allocation Model (Proposed)

(Visual: Pie chart showing 30% bank reserve + 70% low-risk assets)

Regulatory Structure (CBK vs CMA Responsibilities)

(Visual: Diagram showing division of oversight roles)

10. Conclusion: Regulation as an Enabler, Not a Constraint

Kenya’s Virtual Asset Service Providers Regulations 2026 represent a critical inflection point—not just for the country, but for the global crypto ecosystem.

Rather than restricting innovation, the framework aims to:

- Formalize trust

- Protect users

- Enable institutional participation

For entrepreneurs, investors, and operators, the message is clear:

The next phase of crypto growth will be regulated, compliant, and infrastructure-driven.

Those who adapt early—by building audit-ready systems, transparent reserve models, and compliance-integrated platforms—will be best positioned to capture the next wave of opportunity.