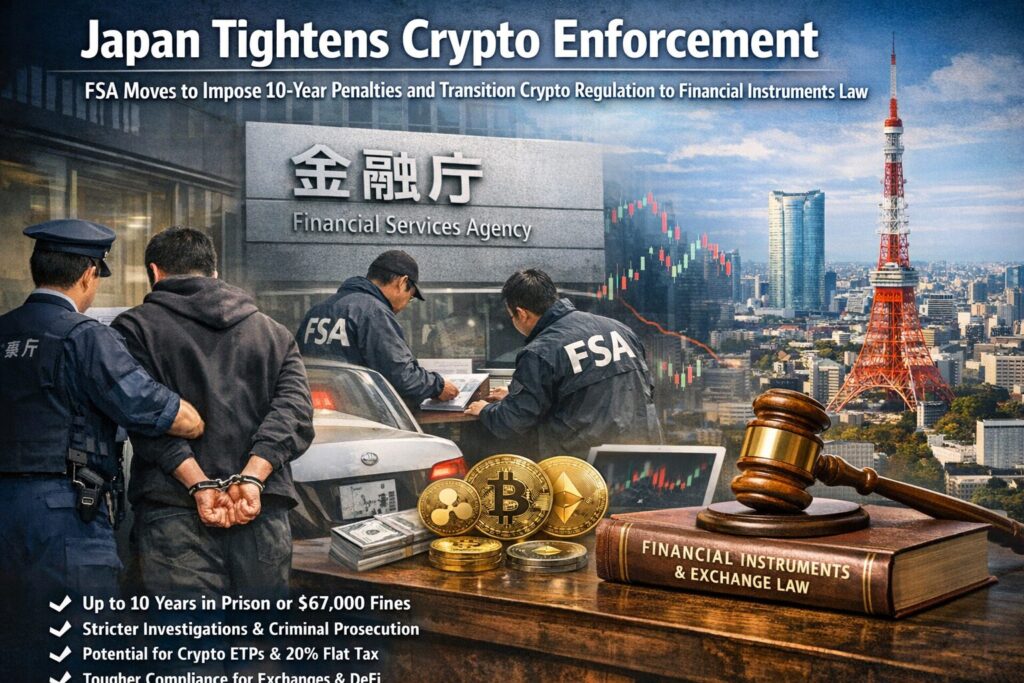

Main Points :

- Japan’s Financial Services Agency (FSA) plans to increase criminal penalties for unregistered crypto sales to up to 10 years in prison or $67,000 in fines.

- The regulatory framework for crypto will shift from the Payment Services Act to the Financial Instruments and Exchange Act (FIEA).

- Authorities will gain stronger investigative powers, including search, seizure, and criminal prosecution.

- The transition could open the door to crypto ETFs and a 20% flat tax system, making crypto investment more attractive.

- At the same time, compliance standards will rise significantly, affecting exchanges, token issuers, and DeFi-related businesses.

Part 1 — Introduction: Japan Signals a New Phase of Crypto Regulation

Japan is once again positioning itself at the forefront of global cryptocurrency regulation. According to reports from Nikkei, the country’s Financial Services Agency (FSA) is preparing to significantly strengthen penalties against companies that sell crypto assets without proper registration. The proposed changes would increase criminal penalties from the current maximum of three years imprisonment to as much as ten years.

This development is closely linked to a broader regulatory transition: Japan intends to shift the legal foundation for cryptocurrency oversight from the Payment Services Act to the Financial Instruments and Exchange Act (FIEA). The move represents a fundamental shift in how digital assets are classified and supervised in one of the world’s most mature crypto markets.

While stricter penalties may appear negative for the industry at first glance, the reform is actually part of a larger strategy aimed at strengthening investor protection while simultaneously opening the door to institutional crypto markets. In particular, the transition to the Financial Instruments and Exchange Act could enable new investment vehicles such as cryptocurrency exchange-traded funds (ETFs) and a simplified tax regime.

For investors searching for emerging crypto opportunities and practical blockchain applications, Japan’s regulatory shift may represent one of the most significant developments in the global digital asset ecosystem.

Part 2 — Stronger Criminal Penalties for Unregistered Crypto Businesses

Japan’s existing framework under the Payment Services Act imposes relatively moderate penalties on companies that sell cryptocurrencies without proper registration. Currently, violators face:

- Up to three years imprisonment,

- A fine of up to ¥3 million (about $20,000),

- Or both.

Under the proposed reforms, these penalties would become dramatically more severe:

- Up to 10 years imprisonment,

- A fine of up to ¥10 million (about $67,000),

- Or both.

This represents more than a three-fold increase in maximum prison sentences.

The stricter penalties will not only apply to companies directly operating crypto exchanges but also to businesses that solicit or promote crypto derivative transactions without authorization. This expansion significantly broadens the enforcement scope of regulators.

From a global perspective, the move aligns Japan with increasingly strict enforcement seen in jurisdictions such as the United States and the European Union, where regulators have intensified their actions against unlicensed digital asset services.

For crypto entrepreneurs and token issuers, the message is clear: operating outside the regulatory framework will carry far greater legal risks in Japan moving forward.

Part 3 — Expanded Enforcement Powers: Search, Seizure, and Criminal Investigations

Beyond tougher penalties, the FSA also intends to strengthen the country’s enforcement infrastructure.

Until now, regulators primarily relied on administrative actions such as:

- Issuing warning letters to unregistered companies

- Requesting court orders to suspend operations

- Ordering business improvements

However, the new framework would allow authorities to treat illegal crypto operations as criminal investigations under financial law violations.

This means the Securities and Exchange Surveillance Commission (SESC), Japan’s financial watchdog, will be able to conduct:

- On-site inspections

- Evidence seizure

- Search warrants

- Formal criminal referrals to prosecutors

Such powers represent a significant escalation in enforcement capabilities.

For comparison, similar enforcement powers have been used in traditional securities markets to investigate insider trading, market manipulation, and illegal brokerage operations. Applying them to the crypto industry indicates that regulators increasingly view digital assets as part of the mainstream financial system rather than a separate experimental market.

Part 4 — Transition to the Financial Instruments and Exchange Act

The most transformative element of the policy change is the transition of cryptocurrency regulation from the Payment Services Act to the Financial Instruments and Exchange Act (FIEA).

Under the current Payment Services Act, cryptocurrencies are treated primarily as means of payment or settlement instruments.

Under the FIEA, however, digital assets would increasingly be treated as financial investment instruments.

This shift has several important implications:

1. Greater Investor Protection

The FIEA imposes strict rules on financial products, including:

- Disclosure obligations

- Suitability requirements for investors

- Market manipulation prevention

- Custody and segregation of client assets

Applying these standards to crypto markets could significantly improve investor protection.

2. Institutional Market Participation

Because the FIEA governs securities markets, its application to cryptocurrencies could allow regulated financial institutions such as banks, brokerages, and asset managers to participate more actively.

This may lead to:

- Institutional trading platforms

- Crypto investment funds

- Regulated custody services.

3. Potential Approval of Crypto ETFs

One of the most anticipated outcomes of the regulatory transition is the potential approval of cryptocurrency exchange-traded funds.

In the United States, the launch of spot Bitcoin ETFs in 2024 triggered massive institutional inflows and dramatically increased market liquidity.

If Japan follows a similar path, domestic crypto markets could experience substantial growth.

Part 5 — Tax Reform and the 20% Flat Tax Possibility

Another highly anticipated aspect of the transition to the Financial Instruments and Exchange Act is the possibility of introducing separate taxation for cryptocurrency investments.

Currently, crypto profits in Japan are generally treated as miscellaneous income, meaning they are taxed under progressive income tax rates that can exceed 50% for high-income earners.

If cryptocurrencies become financial instruments under the FIEA, they could potentially be taxed under a separate flat tax system similar to stock investments.

This would likely mean:

- A tax rate of approximately 20% on capital gains

- Simplified tax reporting

- Increased participation from retail investors.

Many Japanese crypto investors have long advocated for this change, arguing that the current tax regime discourages long-term investment and innovation.

Part 6 — Global Context: Regulation Tightens Worldwide

Japan’s regulatory tightening is occurring alongside broader global developments in crypto regulation.

Several major jurisdictions have recently introduced new frameworks:

United States

The SEC and other regulators have aggressively pursued enforcement actions against unregistered exchanges and token issuers. At the same time, the approval of spot Bitcoin ETFs has brought billions of dollars into the market.

European Union

The EU’s MiCA (Markets in Crypto-Assets) regulation has established a comprehensive regulatory framework covering exchanges, stablecoins, and token issuers.

Singapore and Hong Kong

Both jurisdictions are attempting to balance strict compliance requirements with efforts to attract institutional crypto businesses.

Japan’s new policy appears to follow a similar philosophy: strict compliance rules combined with opportunities for regulated innovation.

Part 7 — Implications for Crypto Investors and Builders

For investors, Japan’s regulatory overhaul may actually create a more stable and attractive crypto market environment.

Key potential benefits include:

- Higher market transparency

- Stronger consumer protection

- Institutional investment inflows

- ETF market development.

For builders and entrepreneurs, however, the environment will become more demanding.

Companies operating in Japan will need to ensure:

- Proper licensing

- AML/KYC compliance

- Financial reporting standards

- investor protection mechanisms.

Failure to comply will carry significantly higher legal risks under the new regime.

Evolution of Crypto Regulation in Japan

2017 — Payment Services Act recognizes Bitcoin2020 — Crypto custody regulations strengthened2023 — Stablecoin legal framework introduced2026 — Shift to Financial Instruments and Exchange Act

Comparison of Penalties

| Regulation | Prison Term | Maximum Fine |

|---|---|---|

| Current Law | 3 years | $20,000 |

| New Proposal | 10 years | $67,000 |

Potential Market Impact

Stronger Regulation ↓Higher Investor Confidence ↓Institutional Participation ↓Crypto ETFs & Market Growth

Conclusion — A Turning Point for Japan’s Crypto Industry

Japan’s decision to strengthen penalties for unregistered cryptocurrency sales and transition regulation to the Financial Instruments and Exchange Act represents a pivotal moment for the country’s digital asset ecosystem.

While the new framework introduces stricter compliance requirements and harsher enforcement mechanisms, it also lays the foundation for a more mature and institutionally integrated crypto market.

If implemented successfully, the reforms could bring several long-term benefits:

- Improved investor protection

- Greater institutional participation

- New financial products such as crypto ETFs

- A more competitive global crypto market for Japan.

For investors seeking the next wave of blockchain innovation and digital asset opportunities, Japan’s evolving regulatory framework may serve as a model for how mature economies integrate cryptocurrencies into their financial systems.