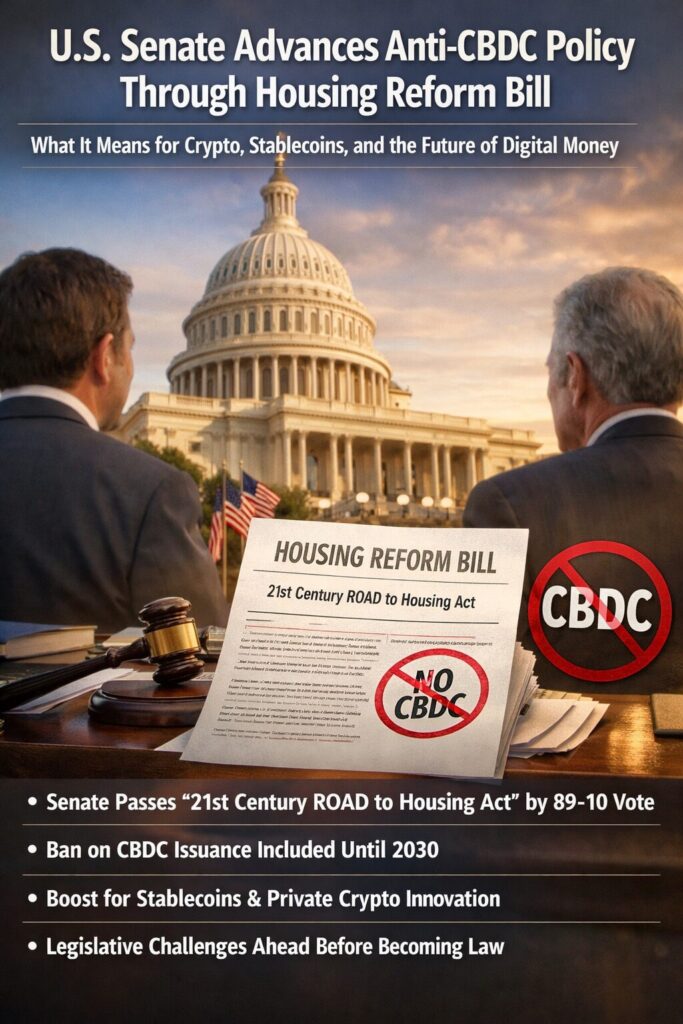

Main Points :

- The U.S. Senate passed the “21st Century ROAD to Housing Act” by a vote of 89–10, a strong bipartisan majority.

- The bill includes a provision banning the U.S. Federal Reserve from issuing a CBDC until the end of 2030.

- The anti-CBDC clause was attached to a housing reform bill, likely as a legislative strategy to push the policy forward.

- The proposal aligns with the current U.S. administration’s preference for private-sector stablecoins over government-issued digital currencies.

- Despite Senate approval, the bill still faces legislative hurdles before becoming law, including reconciliation with the House and presidential priorities.

- The policy direction could accelerate innovation in private crypto payment infrastructure and stablecoin ecosystems.

Introduction

The debate over Central Bank Digital Currencies (CBDCs) has become one of the most important policy battlegrounds shaping the future of global finance. In March 2026, the United States Senate made a significant move in this debate by approving a housing reform bill that includes a temporary ban on the Federal Reserve issuing a digital dollar.

The legislation, formally titled the “21st Century ROAD to Housing Act,” passed with overwhelming bipartisan support—89 votes in favor and only 10 opposed. Although the bill primarily addresses housing supply reform and affordability issues in the United States, it has attracted global attention because of a clause that prohibits the Federal Reserve from issuing a CBDC until December 31, 2030.

For cryptocurrency investors, blockchain developers, and financial institutions exploring digital assets, this development carries major implications. It signals a potential shift in U.S. policy toward favoring privately issued digital currencies—especially stablecoins—over government-controlled digital money.

This article analyzes the legislation, the political motivations behind it, and how the evolving regulatory landscape may shape the next phase of crypto innovation.

The Senate’s Anti-CBDC Clause: A Strategic Legislative Move

The most notable feature of the housing reform bill is the provision preventing the Federal Reserve from launching a Central Bank Digital Currency before 2030.

CBDCs are digital forms of sovereign currency issued directly by central banks. Unlike cryptocurrencies such as Bitcoin or Ethereum, CBDCs represent digitized versions of national fiat currencies and remain fully under government control.

The bill’s anti-CBDC clause reflects growing skepticism among U.S. policymakers regarding the risks of a government-issued digital dollar. Critics argue that CBDCs could potentially enable unprecedented levels of financial surveillance, allowing central authorities to monitor or even restrict individual transactions.

Attaching this clause to a housing reform bill appears to be a deliberate political strategy. Housing affordability and supply reform are top domestic priorities in the United States, making the broader bill politically difficult to oppose. By embedding the CBDC restriction within it, lawmakers increased the likelihood that the measure would advance through Congress.

This tactic is not unusual in U.S. politics, where controversial provisions are often inserted into larger legislative packages that address urgent national concerns.

Understanding CBDCs: Why Governments Are Interested

To understand the significance of the Senate vote, it is essential to examine what CBDCs are and why central banks worldwide are studying them.

A Central Bank Digital Currency (CBDC) is essentially a digital representation of fiat money issued by a country’s central bank. Unlike cryptocurrencies, which operate on decentralized networks, CBDCs are centralized and backed by state authority.

Central banks view CBDCs as a potential evolution of payment infrastructure for several reasons:

- Faster payment systems

- Reduced transaction costs

- Greater financial inclusion

- Improved monetary policy transmission

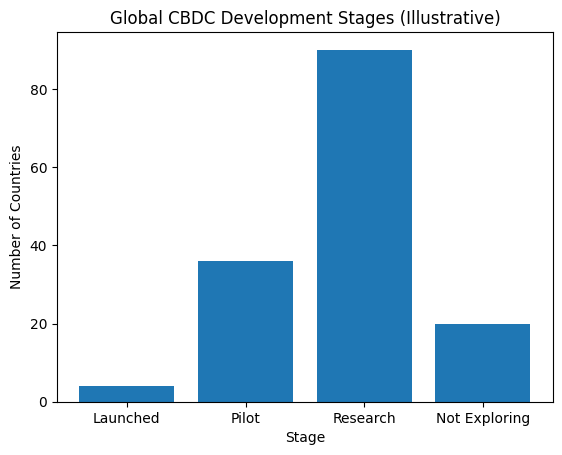

More than 130 countries, representing over 98% of global GDP, are currently researching or developing CBDCs according to data from the Atlantic Council.

China has been particularly aggressive in this area with its digital yuan (e-CNY) pilot programs. Meanwhile, the European Central Bank is progressing toward a digital euro, and many emerging economies are experimenting with national digital currencies to modernize payment systems.

Despite this global momentum, the United States has remained cautious.

Privacy Concerns and Political Resistance

The main driver behind opposition to a U.S. CBDC is the fear that such a system could compromise financial privacy.

A government-issued digital currency could theoretically allow authorities to track every transaction made by individuals or businesses. Critics argue this could lead to programmable money, where governments might impose spending restrictions or surveillance mechanisms.

Several U.S. lawmakers have framed CBDCs as a potential threat to civil liberties.

Supporters of the anti-CBDC provision argue that the private sector—particularly stablecoin issuers—can deliver the benefits of digital payments without expanding government control over financial activity.

This ideological divide reflects a broader philosophical debate about the future of money:

- State-controlled digital currency (CBDC)

- Market-driven digital assets (crypto and stablecoins)

The Senate vote suggests that, at least for now, the U.S. political climate favors the latter.

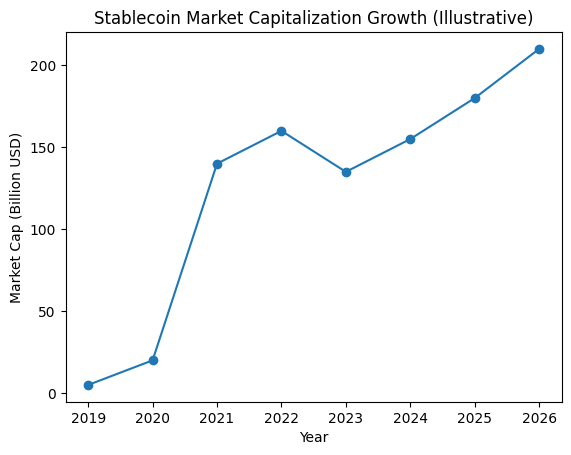

The Rise of Stablecoins as an Alternative

The current administration has previously expressed support for expanding the role of private-sector stablecoins in the financial system.

Stablecoins are digital assets designed to maintain a fixed value relative to fiat currencies—typically $1 per token. They combine the price stability of traditional currency with the programmability and global accessibility of blockchain technology.

Major stablecoins such as USDT and USDC now process trillions of dollars in annual transaction volume, often surpassing traditional payment networks during peak activity periods.

Stablecoins already play a critical role in:

- Cross-border remittances

- Crypto trading liquidity

- Decentralized finance (DeFi)

- On-chain payments

If the U.S. government continues delaying a CBDC, the stablecoin ecosystem could become the de facto digital dollar infrastructure for global finance.

This dynamic could significantly expand opportunities for blockchain developers and crypto entrepreneurs.

Legislative Hurdles Still Remain

Despite the overwhelming Senate vote, the housing reform bill is not yet law.

Several procedural steps remain before the anti-CBDC clause becomes legally binding.

First, the bill must be reconciled with the House of Representatives, where lawmakers may propose amendments or modifications.

Second, the legislation must ultimately be signed by the President.

Recent political developments may complicate the timeline. Reports indicate that the President has stated he will prioritize approval of the SAVE America Act before signing other legislation.

If that position holds, the housing reform bill—including its anti-CBDC provision—could face delays in becoming law.

Nevertheless, the Senate vote itself signals strong bipartisan momentum behind the idea of limiting CBDC development in the United States.

Global Implications for Crypto Markets

The policy shift may have broader implications for the global digital asset ecosystem.

If the United States delays CBDC issuance while other nations proceed, the global financial system could evolve along two distinct paths.

One scenario involves a world dominated by state-issued digital currencies, led by countries such as China.

Another possibility is a financial ecosystem where private blockchain-based stablecoins function as the dominant digital payment layer, particularly in dollar-denominated markets.

Because the U.S. dollar remains the world’s primary reserve currency, any decision affecting its digital form could influence the structure of international finance.

For crypto investors, this environment may create new opportunities in areas such as:

- Stablecoin infrastructure

- Blockchain payment networks

- Cross-border settlement protocols

- Tokenized financial assets

Projects focused on real-world payment utility may benefit most from this policy direction.

Practical Opportunities for Blockchain Builders

For entrepreneurs and developers exploring real-world blockchain applications, the anti-CBDC stance could create a favorable innovation environment in the United States.

Without a government-controlled digital currency competing directly with the private sector, blockchain companies may have more room to develop solutions in areas such as:

1. On-chain payment rails

Infrastructure that enables instant global settlements.

2. Tokenized financial assets

Digital representations of stocks, bonds, or commodities.

3. Stablecoin-based remittance systems

Low-cost cross-border transfers that bypass traditional banking networks.

4. Decentralized identity and compliance tools

Systems that allow regulatory compliance while protecting user privacy.

For fintech companies building wallets, payment platforms, or tokenization infrastructure, the delay of a U.S. CBDC could represent a major strategic opportunity.

[Global CBDC Development Status Map]

Visualize countries categorized by:

- CBDC launched

- Pilot stage

- Research stage

- Not exploring

This map would illustrate how the United States contrasts with other major economies.

[Stablecoin Market Growth Chart 2019–2026]

Graph showing:

- Total stablecoin market capitalization

- Transaction volume growth

- Adoption across DeFi and payments

This highlights the expanding role of stablecoins.

Conclusion

The U.S. Senate’s approval of the 21st Century ROAD to Housing Act, with its embedded anti-CBDC provision, marks a significant development in the global debate over digital currencies.

While the legislation still faces procedural hurdles before becoming law, the overwhelming 89–10 Senate vote demonstrates strong political momentum behind restricting the Federal Reserve from issuing a digital dollar until at least 2030.

For the cryptocurrency industry, the implications are substantial.

Rather than competing with a government-controlled digital currency, blockchain innovators may find themselves operating in an environment where private-sector digital money—particularly stablecoins—plays a central role in the evolution of financial infrastructure.

As the global financial system transitions toward digital assets, the United States appears poised to explore a different path from many other major economies.

Instead of building a state-issued CBDC, it may rely on regulated private crypto networks to power the next generation of digital finance.

For investors, developers, and entrepreneurs seeking the next wave of blockchain opportunity, this policy direction could shape the landscape of digital money for the rest of the decade.