Main Points :

- A regulated crypto bank has joined Europe’s first blockchain-based securities settlement platform under the EU’s DLT Pilot Regime.

- This marks the first participation of a fully regulated bank in the EU’s experimental tokenized securities market.

- The move aims to bridge traditional capital markets and blockchain infrastructure.

- Institutional adoption of Real-World Asset (RWA) tokenization is accelerating globally.

- However, interoperability, regulatory limits, and market scale remain key obstacles.

- Europe risks falling behind the United States unless regulatory frameworks evolve faster.

1. A New Era for Tokenized Securities in Europe

The integration of blockchain technology into traditional financial markets has long been discussed as one of the most transformative developments in global finance. Yet despite years of experimentation, institutional participation in tokenized securities markets has remained limited. That situation may now be changing.

A major milestone occurred when Swiss-regulated digital asset bank AMINA joined the 21X blockchain securities settlement platform, which operates under the European Union’s Distributed Ledger Technology (DLT) Pilot Regime. With this move, AMINA becomes the first fully regulated bank to participate directly in the EU’s experimental blockchain securities infrastructure.

The significance of this step extends far beyond a single institutional partnership. It signals a broader effort to merge regulated financial institutions, blockchain infrastructure providers, and tokenization platforms into a cohesive digital capital market ecosystem.

The collaboration also involves Tokeny, a Luxembourg-based tokenization technology provider, which will enable companies to issue tokenized securities on the 21X platform with institutional-grade infrastructure and compliance support.

If successful, the initiative could serve as a blueprint for how blockchain markets evolve from speculative crypto trading into fully regulated financial markets capable of handling equities, bonds, and other financial instruments.

2. Understanding the EU’s DLT Pilot Regime

To understand why this development matters, it is necessary to examine the regulatory framework that makes it possible.

The DLT Pilot Regime, introduced by the European Union in 2023, is essentially a regulatory sandbox for blockchain-based financial market infrastructure. It allows selected market operators to experiment with trading, clearing, and settlement of financial instruments using distributed ledger technology while remaining under regulatory supervision.

This framework enables platforms such as 21X to operate blockchain-based securities markets within controlled limits.

Key characteristics of the DLT Pilot Regime include:

- Permission for blockchain-based trading and settlement of securities

- Regulatory supervision by EU authorities

- Market size limits designed to contain systemic risk

- Experimental regulatory flexibility

While traditional securities markets typically rely on complex chains of intermediaries—custodians, clearing houses, settlement agents—the DLT model allows these processes to occur directly on blockchain infrastructure, potentially reducing costs and settlement times dramatically.

However, the sandbox nature of the framework also means that the maximum market size is currently restricted, which has led to criticism from industry participants.

3. Why Banks Are Critical for Institutional Adoption

One of the largest barriers to tokenized securities adoption has been the absence of regulated banking institutions.

Institutional investors such as pension funds, asset managers, and insurance companies are subject to strict compliance requirements. They typically cannot interact directly with unregulated crypto infrastructure.

Banks therefore play several critical roles:

- Custody of digital assets

- Compliance and regulatory oversight

- Settlement and liquidity provision

- Institutional onboarding

The entry of AMINA into the 21X ecosystem addresses this gap.

By acting as a listing sponsor and institutional gateway, the bank can help companies issue tokenized securities while ensuring compliance with financial regulations.

This could significantly reduce the perceived risk for institutional investors considering participation in blockchain-based markets.

4. The Rapid Rise of Real-World Asset (RWA) Tokenization

The development also reflects a broader global trend: the rapid growth of tokenized real-world assets (RWA).

RWA tokenization refers to representing traditional financial assets on blockchain networks.

Examples include:

- Government bonds

- Corporate debt

- Real estate

- Equities

- Private credit

The market has expanded dramatically over the past two years.

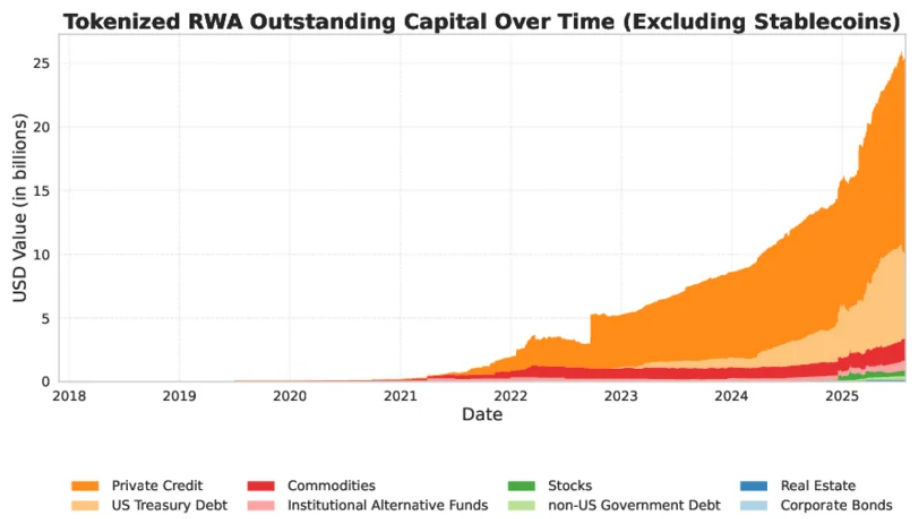

As of recent estimates, the total value of tokenized real-world assets has reached approximately $26.5 billion.

Major drivers of this growth include:

- Institutional demand for on-chain settlement

- Lower operational costs compared with traditional infrastructure

- Increased transparency through blockchain records

- Programmable financial instruments

Financial institutions increasingly see tokenization as a way to modernize capital markets rather than replace them.

5. Global Institutional Momentum

The European development is part of a much broader movement among major financial institutions.

In the United States, several financial giants have begun building blockchain-based financial infrastructure.

Examples include:

- BNY Mellon developing digital asset custody solutions

- Nasdaq exploring blockchain settlement technology

- S&P Global supporting blockchain data infrastructure

- The expansion of the Canton Network, a blockchain system designed specifically for regulated financial markets

The Canton Network initiative is particularly notable because it focuses on interoperability between financial institutions, allowing multiple market participants to transact on interconnected blockchain systems.

This highlights a key difference between early cryptocurrency ecosystems and the emerging institutional blockchain landscape.

Rather than creating isolated platforms, institutions are increasingly prioritizing interconnected infrastructure capable of supporting global financial markets.

6. Interoperability: The Biggest Barrier

Despite the rapid growth of tokenization, experts argue that lack of interoperability between platforms remains the biggest challenge.

Financial institutions require standardized infrastructure that allows assets to move across multiple systems.

According to analysts and legal experts in financial services, tokenized asset markets will only achieve meaningful scale once many market participants trade on shared or interconnected platforms.

Without interoperability:

- Liquidity becomes fragmented

- Asset transfers become complex

- Institutional adoption slows

This issue is already visible in today’s blockchain ecosystem, where hundreds of networks operate independently.

Solving interoperability may require new technological solutions such as:

- cross-chain settlement layers

- standardized token frameworks

- shared financial messaging protocols

7. Regulatory Competition: Europe vs the United States

While Europe has taken an early lead with the DLT Pilot Regime, some industry observers worry that the regulatory framework may be too restrictive.

The current sandbox imposes limits on:

- trading volume

- market size

- types of financial instruments

These restrictions were designed to protect financial stability during early experimentation.

However, critics argue they may unintentionally slow Europe’s ability to compete with the United States and Asia in building large-scale tokenized financial markets.

In fact, earlier this year eight EU digital asset companies publicly urged policymakers to accelerate digital asset legislation, warning that Europe could fall behind other regions.

The United States, despite regulatory uncertainty around cryptocurrencies, has seen strong institutional experimentation with tokenized securities and blockchain infrastructure.

8. New Blockchain Securities Platforms Are Emerging

Meanwhile, exchanges and trading platforms are beginning to launch tokenized securities products.

One example is the Kraken xStocks platform, which allows European investors to trade tokenized versions of U.S. listed equities on blockchain networks.

These systems aim to offer several advantages:

- 24-hour trading markets

- fractional ownership of stocks

- faster settlement times

- programmable compliance features

While still in the early stages, these innovations could eventually transform how securities markets operate globally.

9. What This Means for Crypto Investors and Builders

For readers interested in discovering new crypto assets or revenue opportunities, the rise of regulated tokenized securities markets is extremely significant.

Historically, the cryptocurrency industry focused primarily on native digital assets such as Bitcoin and Ethereum.

However, the next phase of blockchain finance may revolve around tokenized versions of traditional assets.

This could create opportunities across several sectors:

- tokenization platforms

- blockchain settlement infrastructure

- compliance technology providers

- digital asset custody services

- decentralized identity systems

Projects building infrastructure for RWA tokenization could become some of the most valuable segments of the blockchain industry.

10. The Long-Term Vision: Blockchain Capital Markets

Ultimately, initiatives such as the 21X platform represent the early stages of a much larger transformation.

If blockchain technology successfully integrates with regulated financial markets, the future capital market infrastructure could look very different from today’s system.

Possible long-term outcomes include:

- near-instant securities settlement

- global trading access for investors

- automated compliance through smart contracts

- reduced dependence on financial intermediaries

However, reaching this stage will require solving several challenges:

- interoperability

- regulatory clarity

- institutional trust

- technological scalability

Conclusion

The participation of a regulated bank in Europe’s blockchain securities market represents a crucial milestone in the evolution of digital finance.

While the cryptocurrency industry initially developed outside traditional financial systems, the current trend suggests a gradual convergence between blockchain infrastructure and institutional capital markets.

The rise of tokenized real-world assets, the expansion of blockchain financial networks, and the involvement of major banks and exchanges all point toward a future where securities may increasingly exist and trade on distributed ledgers.

Yet the path forward remains complex. Regulatory limitations, technological fragmentation, and market infrastructure challenges must still be addressed before blockchain securities markets reach global scale.

Nevertheless, the direction is clear: the next stage of the blockchain revolution will not simply be about cryptocurrencies—it will be about rebuilding the architecture of global finance.