Main Points :

- Stablecoin payment infrastructure is attracting massive investment from companies like Circle, Stripe, Visa, and Mastercard.

- Despite the hype, stablecoin usage in everyday commerce remains extremely small relative to global payment volumes.

- AI agents—autonomous software that can transact without human intervention—are emerging as a potentially transformative use case.

- Stablecoins are uniquely suited for machine-to-machine microtransactions due to low cost and near-instant settlement.

- The convergence of AI, blockchain, and stablecoins could create a new internet-native financial system over the next decade.

1. Stablecoin Infrastructure Investment Is Accelerating

The global financial technology industry is entering a new phase in the evolution of stablecoins. What began as a tool primarily used for crypto trading and arbitrage is now being positioned as the backbone of a new digital payment infrastructure.

Over the past year, major financial institutions and technology companies have dramatically increased their investment in stablecoin payment systems.

One of the most prominent initiatives comes from Circle, the issuer of the USDC stablecoin. The company is currently developing a blockchain network called Arc, specifically designed to optimize stablecoin payments. More than 100 companies—including payment giant Visa—are already participating in the Arc testnet.

Stripe, another global payments leader, is also pursuing a similar strategy. In collaboration with the crypto venture capital firm Paradigm, Stripe is building a dedicated stablecoin payment blockchain called Tempo. The project includes design partners such as Visa and Shopify, while financial institutions including Mastercard and UBS are participating as testnet partners.

These developments reflect a broader shift: stablecoins are no longer seen only as crypto trading instruments but as potential global settlement layers for digital commerce.

Japan has also begun exploring this space. Sony Bank recently announced a strategic partnership with JPYC Inc., a company issuing a Japanese yen-denominated stablecoin. The partnership aims to enable instant purchases of JPYC directly from bank accounts using real-time debit systems.

Meanwhile, LINE NEXT plans to integrate JPYC into its Web3 wallet service Unify, accessible through the widely used LINE messaging application. If implemented successfully, this could bring stablecoin payments into everyday consumer applications in Japan.

These initiatives signal a clear trend: the infrastructure required for stablecoin payments is rapidly expanding across multiple regions and industries.

2. Stablecoin Adoption Still Lags Far Behind Expectations

Despite the surge in investment and technological development, stablecoins have not yet achieved widespread adoption in everyday payments.

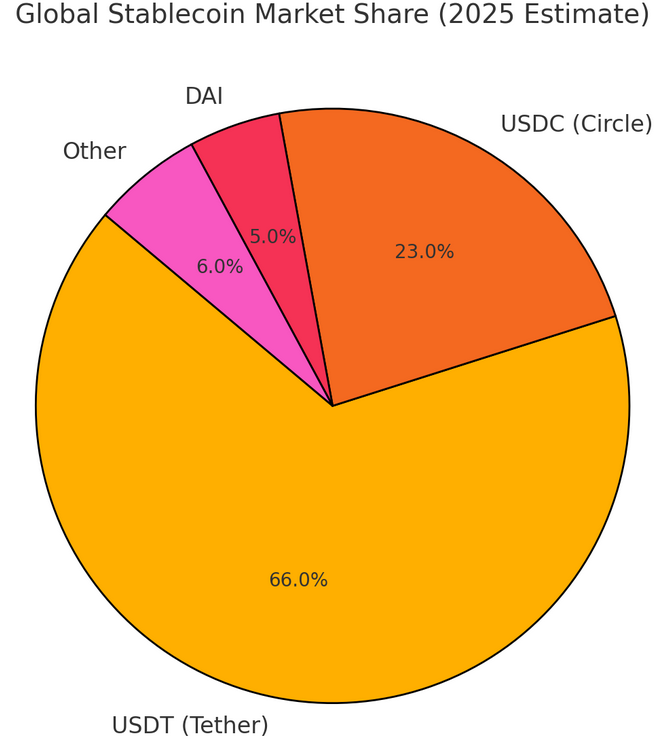

According to estimates from consulting firm McKinsey, global e-commerce sales are expected to reach approximately $6.88 trillion this year. In comparison, total annual stablecoin payment volume is estimated at roughly $390 billion.

This means stablecoins account for only a small fraction of global digital commerce.

Even more revealing is the distribution of stablecoin usage. McKinsey estimates that around $226 billion of stablecoin payments occur in B2B transactions. This suggests that businesses—particularly those involved in crypto trading or cross-border settlements—are the primary users of stablecoins today.

Retail usage remains extremely limited.

The European Central Bank estimates that only 0.5% of stablecoin transaction volume is associated with small consumer remittances. Meanwhile, a report titled Stablecoin Utility Report found that only about 6% of everyday commercial transactions currently use stablecoins for purchasing goods and services.

This gap between technological potential and real-world adoption has led many industry participants to search for a compelling new use case that could justify the massive infrastructure investments now underway.

Increasingly, that use case appears to be AI agent payments.

3. AI Agents Could Become the Largest Users of Stablecoins

AI agents are autonomous software systems capable of performing tasks on behalf of humans.

Recent advances in generative AI—particularly systems similar to ChatGPT—are transforming chatbots from simple conversational tools into fully functional “agents” capable of executing tasks, interacting with APIs, and even making economic decisions.

In an AI-driven digital economy, these agents will increasingly interact with each other rather than with humans.

For example, an AI system might automatically purchase:

- data from another service

- computing resources

- API access

- cloud storage

- specialized AI models

These transactions may occur thousands or even millions of times per day, often involving extremely small payments.

Traditional payment systems such as credit cards and bank transfers were never designed for this type of activity.

High transaction fees, slow settlement times, and regulatory friction make conventional payment rails inefficient for frequent microtransactions.

Stablecoins, by contrast, offer several advantages:

- near-instant settlement

- low transaction fees

- global accessibility

- programmable payments via smart contracts

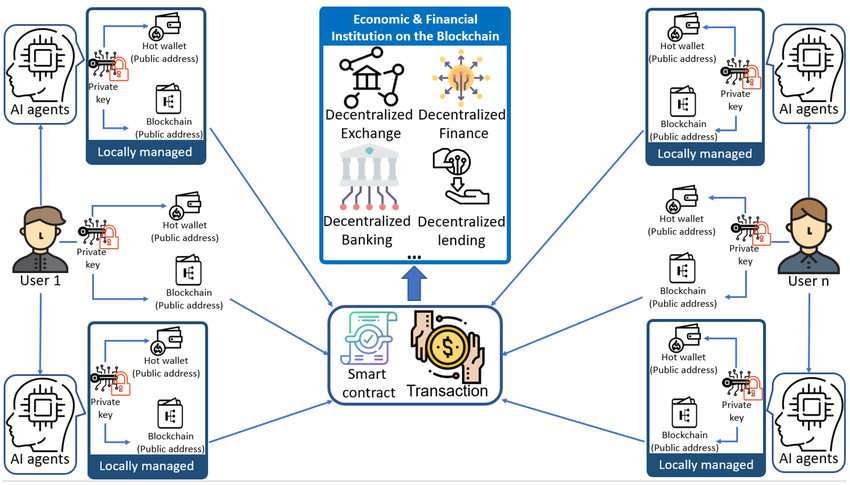

These characteristics make stablecoins uniquely suited for machine-to-machine (M2M) payments, which could become a core component of the AI economy.

4. Circle’s Vision: Billions of AI Agents Using Stablecoins

Circle CEO Jeremy Allaire recently emphasized this vision during the World Economic Forum annual meeting in Davos.

According to Allaire, within the next five years billions of AI agents may require payment capabilities, and stablecoins could become the only practical solution for enabling these transactions.

During Circle’s February earnings call, Allaire reiterated that stablecoins are likely to become the primary currency for machine-to-machine transactions in the AI era.

Circle believes that the convergence of AI, blockchain, and stablecoins will create a completely new financial system built directly on the internet.

One demonstration of this concept was recently released by the company.

Circle posted a video showing an autonomous robot dog named Bits, developed by robotics company OpenMind. In the demonstration, the robot independently pays for access to a charging station using the USDC stablecoin.

The payment occurs entirely on-chain, with no human intervention.

After completing the payment, the robot dog automatically begins charging.

While this example may appear experimental, it highlights a critical concept: machines could soon become economic actors capable of making payments autonomously.

Circle and OpenMind are currently working together to develop a machine-to-machine payment standard based on USDC, enabling autonomous systems and digital infrastructure to conduct micropayments across networks.

If successful, such standards could become foundational to the future AI economy.

5. AI Agent Commerce Could Become a Trillion-Dollar Market

According to research from McKinsey, AI agent payments could become a massive new economic sector.

The firm estimates that by 2030, AI-driven transactions in the U.S. B2C retail market alone could generate up to $1 trillion in revenue.

However, Circle’s leadership believes the most significant opportunities may not come from consumer shopping.

Instead, the true growth potential may lie in AI-to-AI service transactions.

For example, an AI agent specializing in legal analysis could process requests from corporate clients by purchasing specialized datasets or legal expertise from other AI agents.

Similarly, AI systems responsible for logistics, cybersecurity, finance, or cloud infrastructure could interact with other AI services through automated payment mechanisms.

In this scenario, the global economy would include not only human consumers and businesses but also billions of autonomous software agents engaging in economic activity.

Stablecoins could serve as the native currency of this machine-driven economy.

6. Payment Giants Are Preparing for the AI Commerce Era

Major payment networks are already preparing for this transformation.

Visa recently predicted that AI-agent commerce and stablecoins could become mainstream payment technologies by 2026.

The company believes that as leading global brands invest heavily in AI-driven shopping experiences, the next phase will involve AI agents capable of completing purchases autonomously.

Visa is currently collaborating with ecosystem partners to build the infrastructure required for such systems.

Meanwhile, Mastercard CEO Michael Miebach has also identified AI agent commerce and stablecoins as key growth drivers for the company.

Mastercard is working with major technology firms—including companies involved in advanced AI development—to design protocols that support agent-based commerce.

The company is also developing a system called Mastercard Agent Pay, which would allow AI agents to securely mediate transactions across Mastercard’s payment network.

These initiatives indicate that traditional financial institutions are not ignoring the rise of AI-driven digital economies.

Instead, they are actively positioning themselves to support and monetize this emerging market.

7. New Risks in an AI-Driven Financial System

While AI payments offer enormous potential, they also introduce significant risks.

Visa has warned that advances in AI technology could enable new forms of fraud.

Historically, payment fraud has typically targeted individual transactions.

However, AI-powered fraud schemes may instead target entire digital identities.

Techniques such as deepfakes, synthetic identities, and agent-based scams could allow attackers to take control of a victim’s entire financial profile.

If criminals succeed in hijacking an individual’s digital identity, they could potentially control all transactions associated with that identity.

Industry experts expect these risks to increase significantly by 2026 and beyond.

As a result, payment companies are investing heavily in identity verification technologies, AI-driven fraud detection, and collaborative security frameworks.

Managing these risks will be essential for building trust in the next generation of AI-powered financial infrastructure.

Conclusion: Stablecoins May Become the Financial Layer of the AI Economy

Stablecoins are at a critical crossroads.

While their adoption in everyday payments remains relatively limited today, the rapid convergence of AI and blockchain technology is creating a powerful new opportunity.

AI agents may soon require the ability to conduct millions of small transactions across digital networks. Traditional payment systems are poorly suited to this environment.

Stablecoins, with their low fees, global accessibility, and programmable infrastructure, could become the financial backbone of machine-to-machine commerce.

Major companies—including Circle, Stripe, Visa, and Mastercard—are already investing heavily in the infrastructure required to support this vision.

If these developments succeed, the next decade could witness the emergence of a new economic layer of the internet, where autonomous AI systems transact seamlessly using blockchain-based currencies.

For investors, developers, and entrepreneurs exploring the future of blockchain applications, the intersection of AI agents, stablecoins, and digital payments may represent one of the most important technological frontiers of the coming decade.