Main Points :

- USDT is used by more than 550 million people in emerging markets, highlighting its role as a practical digital dollar for populations excluded from traditional banking systems.

- Transaction concentration is far lower than competing stablecoins, with the largest sender accounting for only 4.97% of total transfers, compared with 23.34% for other stablecoins.

- Tether reported over $10 billion in net profit in 2025, reflecting the massive scale of the stablecoin economy.

- Total USDT circulation reached $186.5 billion, with approximately $50 billion newly issued during 2025.

- Tether holds approximately $192.9 billion in reserves, including over $141 billion exposure to U.S. Treasury securities, positioning it among the world’s largest Treasury holders.

Introduction: Stablecoins Move Beyond Crypto Trading

Stablecoins were originally designed to solve a simple problem in cryptocurrency markets: volatility. By pegging their value to fiat currencies such as the U.S. dollar, stablecoins allowed traders to move funds quickly between exchanges without leaving the crypto ecosystem.

Over the past few years, however, the role of stablecoins has expanded dramatically. What began as a trading tool has evolved into something far larger: a global digital payment infrastructure used by hundreds of millions of people.

At the center of this transformation stands USDT (Tether). According to a recent statement by Tether CEO Paolo Ardoino, the stablecoin is now used by over 550 million people in emerging markets, a remarkable milestone that highlights the growing role of blockchain technology in global finance.

While debates continue about regulation and transparency, one fact is becoming increasingly clear: stablecoins—particularly USDT—are rapidly becoming a parallel financial system for people who lack access to traditional banking.

The Decentralized Usage of USDT

One of the most interesting statistics revealed by Ardoino concerns the distribution of USDT transactions.

In the past 12 months, the largest single sender accounted for only 4.97% of total USDT transfer volume. By comparison, other stablecoins show a concentration ratio of 23.34%.

This metric is important because it reflects the degree of decentralization in real-world usage.

When a payment network depends heavily on a few institutional players, it suggests the system is dominated by large exchanges, hedge funds, or trading desks. A lower concentration, on the other hand, implies widespread adoption across many smaller users.

The relatively low concentration in USDT transactions suggests the stablecoin is not only being used by large crypto traders but also by millions of individuals conducting everyday transactions.

This phenomenon can be understood as the grassroots monetization of the digital dollar.

In other words, USDT is not merely an instrument for crypto speculation—it is increasingly functioning as an alternative monetary infrastructure.

Financial Inclusion Through the Digital Dollar

The most striking claim made by Tether’s CEO is that more than 550 million people in emerging markets now use USDT.

If accurate, this figure places USDT among the most widely used financial tools in the developing world.

Why is a digital token gaining such traction among populations historically underserved by traditional finance?

The answer lies in structural weaknesses within the global financial system.

In many countries across Latin America, Africa, and Southeast Asia, citizens face persistent obstacles when attempting to access banking services:

- High inflation eroding local currencies

- Capital controls limiting access to foreign exchange

- Expensive remittance systems

- Limited banking infrastructure in rural regions

For millions of people in these environments, USDT offers a simple alternative: a blockchain-based dollar that can be stored on a smartphone wallet.

Unlike traditional bank accounts, stablecoin wallets do not require:

- credit history

- bank approval

- physical branch visits

As long as users have internet access, they can hold and transfer digital dollars instantly.

This accessibility explains why stablecoins have become particularly popular in countries such as:

- Argentina

- Turkey

- Nigeria

- Venezuela

- Indonesia

- the Philippines

In these markets, USDT is increasingly used for savings, remittances, and everyday commerce.

The Business Model Behind Tether’s Profitability

Tether’s rapid expansion is not only a technological story but also a financial one.

According to company disclosures, Tether generated over $10 billion in net profit in 2025.

This staggering figure places the company among the most profitable entities in the cryptocurrency industry.

The core business model is relatively straightforward.

When users purchase USDT, they exchange fiat currency for digital tokens. Tether then invests the reserves backing these tokens into various financial instruments, primarily U.S. Treasury securities.

Because Treasury bonds generate interest, Tether earns significant income from these reserves.

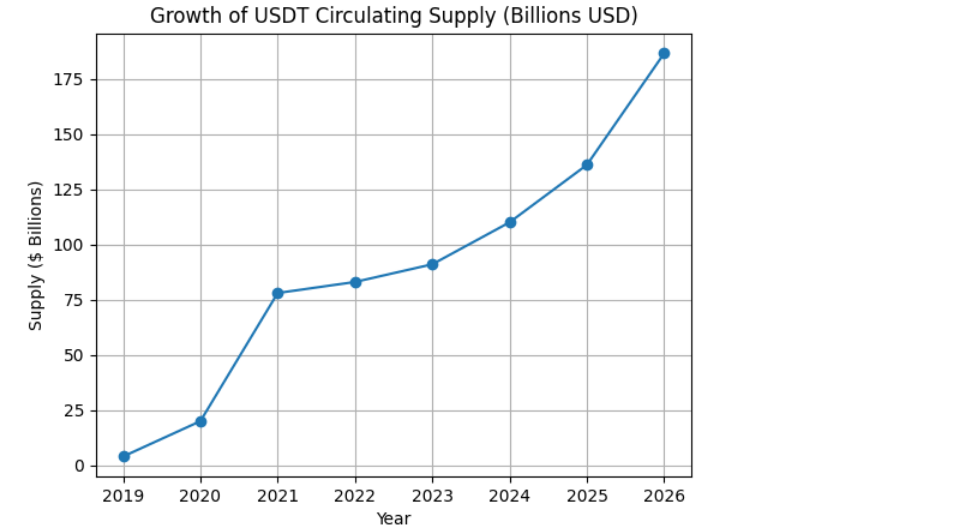

[Growth of USDT Circulating Supply (2019–2026)]

The explosive growth of stablecoins means the reserve pool has become enormous.

As of the latest disclosures:

- Total USDT supply: $186.5 billion

- Total reserves: $192.9 billion

- Excess reserves: $6.3 billion

This reserve structure suggests that Tether holds more assets than the outstanding token supply, a point the company emphasizes in response to criticism regarding transparency.

Tether as a Major Holder of U.S. Treasuries

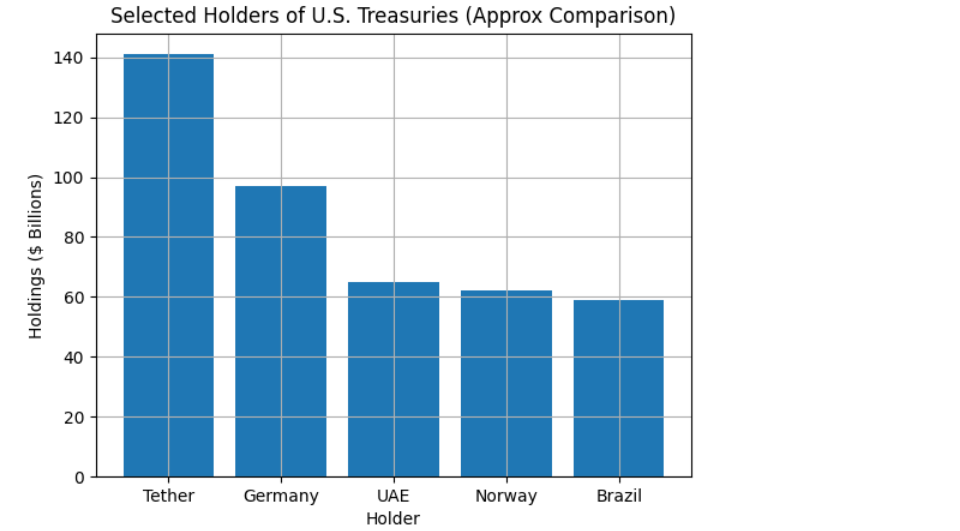

Another remarkable statistic concerns Tether’s exposure to U.S. government debt.

The company reportedly holds more than $141 billion in U.S. Treasury securities, either directly or indirectly.

This amount places Tether among the largest holders of U.S. Treasuries in the world, rivaling some sovereign wealth funds and national governments.

[Tether Treasury Holdings Compared to Countries]

This dynamic creates a fascinating feedback loop between the cryptocurrency economy and traditional finance.

Stablecoins depend on the stability of the U.S. dollar. At the same time, the growth of stablecoins increases demand for U.S. government debt.

In effect, the global expansion of crypto-based dollars may be reinforcing the dominance of the U.S. dollar in international finance.

The Strategic Importance of Emerging Markets

Much of the growth in USDT usage is occurring outside North America and Europe.

Emerging economies represent the primary frontier for stablecoin adoption.

In many developing countries, mobile penetration has outpaced banking infrastructure. This means large populations have smartphones but lack bank accounts.

Stablecoins bridge this gap.

A simple crypto wallet can serve as:

- a savings account

- a remittance tool

- a payment method

For example, migrant workers can send funds home using USDT in minutes instead of paying high remittance fees.

Small businesses can accept digital dollars without dealing with volatile local currencies.

Freelancers can receive international payments without relying on slow banking wires.

These use cases demonstrate that stablecoins are increasingly functioning as practical financial infrastructure, not merely speculative crypto assets.

Competition From Other Stablecoins

Although USDT remains the dominant stablecoin, competition is intensifying.

Major rivals include:

- USDC (Circle)

- DAI (MakerDAO)

- FDUSD

- PayPal USD (PYUSD)

Each project targets slightly different market segments.

USDC focuses on regulatory compliance and institutional adoption. DAI represents the decentralized finance ecosystem. PYUSD seeks integration with global payment networks.

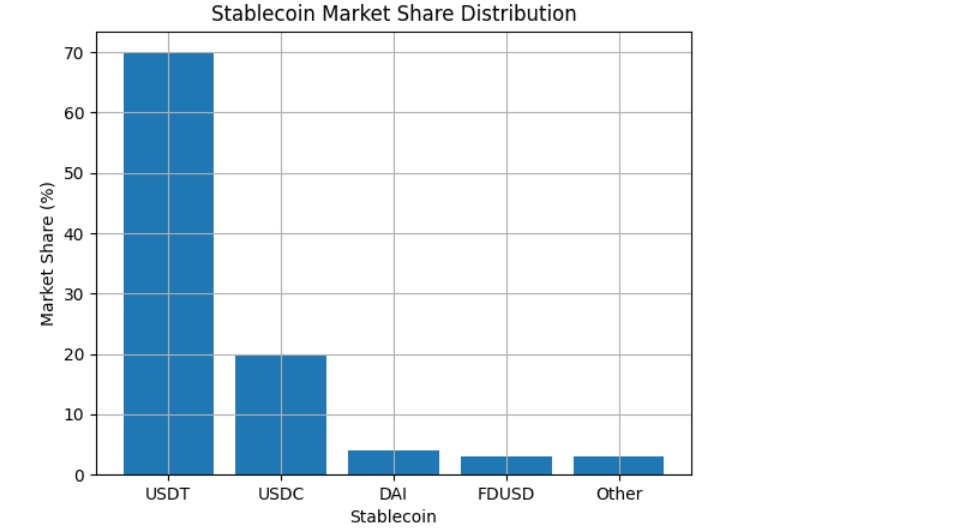

Despite these competitors, USDT continues to maintain the largest market share.

[Stablecoin Market Share Distribution]

The reasons for USDT’s dominance include:

- early entry into crypto markets

- deep liquidity across exchanges

- strong adoption in emerging economies

Regulatory Pressure and Future Outlook

Despite its success, Tether faces increasing scrutiny from regulators.

Governments around the world are developing new frameworks for stablecoins, particularly as the market grows to hundreds of billions of dollars.

In the United States, lawmakers have proposed legislation that could require stablecoin issuers to maintain fully audited reserves and operate under banking-like supervision.

The European Union has already implemented MiCA (Markets in Crypto-Assets) regulations, which impose stricter transparency requirements.

How Tether adapts to these regulatory pressures will shape the future of the stablecoin market.

Nevertheless, demand for digital dollars shows little sign of slowing.

As global inflation persists and cross-border payments remain inefficient, stablecoins may continue expanding as an alternative financial system.

Conclusion: The Emergence of a Parallel Financial Infrastructure

The rise of USDT illustrates a broader transformation taking place in global finance.

What began as a niche crypto trading tool has evolved into a global digital dollar network used by hundreds of millions of people.

With over $186.5 billion in circulation, $10 billion in annual profits, and 550 million users in emerging markets, Tether has become one of the most influential financial institutions in the blockchain era.

For investors and entrepreneurs searching for the next wave of opportunity in the crypto ecosystem, stablecoins represent a critical layer of infrastructure.

They connect blockchain technology with real-world economic activity.

They enable financial inclusion where traditional systems have failed.

And perhaps most importantly, they demonstrate that the future of money may not be controlled solely by governments or banks—but also by open digital networks accessible to anyone with an internet connection.